The search for alpha might be over, at least for a bit, as the buyside has found liquidity and yield in bond backed exchange traded funds (ETFs).

As liquidity wanes in the cash market, the fixed income ETF has emerged as an alternative product that allows investors to navigate an increasingly difficult market environment, a fact reflected in the nine-fold growth in assets under management (AuM) for corporate bond ETFs since 2009, according to a recent report from Tabb Group.

As a matter of fact, credit ETF AUM rose a whopping 15% in Q1 2015 to land at approximately $15 billion, Tabb reported.

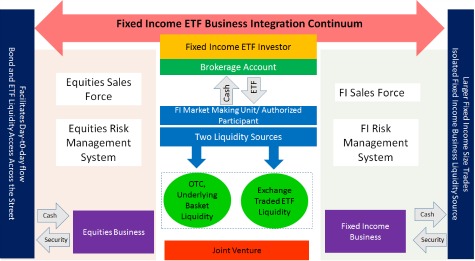

With that much money at stake in commissions, U.S. broker-dealers are building out their fixed income ETF businesses to meet institutional investors’ demands in their search for more viable liquidity options, according to Tabb’s, “Fixed Income ETFs: Bridging the Liquidity Divide.” In the report, co-written by TABB principal, head of fixed income research Anthony Perrotta, and research analyst Colby Jenkins, they examine the meteoric growth in the fixed income ETF market and liquidity dynamics between ETFs and their underlying instruments and the ways in which broker/dealers are meeting customers’ demands.

According to Perrotta, corporate bond ETF AuM grew more than U.S.$110 billion since 2009 as monthly notional volume traded in High Yield credit ETFs have grown from a negligible figure to more than U.S.$21 billion since 2007.

“As institutional investors find fewer viable liquidity options, they’re turning to alternatives such as Fixed Income ETFs, showing a willingness to utilize bond ETFs to manage investment flows, enhance returns and limit transaction costs, exchanging credit risk during times of stress in the underlying market,” Perrotta said.

Despite the bond backed ETF growth, the product does have its critics. Tabb pointed out that corporate bond ETF liquidity could suffer due to the fact that bonds on ETF ‘redemption lists’ trade differently than those that aren’t. However, said Jenkins, a two-tailed t-test measuring the statistical correlation between 41 redemption basket bonds and 358 non-redemption bonds on July 31, 2014 found negligible pricing disparity between the two sets of bonds.

Looking forward, Tabb expects more traditional broker-dealers to enter the asset class and pick up fixed income ETF market-making market share alongside traditional ETF trading firms, utilizing all aspects of the sector’s market-making ecosystem.

“In a world where managers are increasingly scrutinizing execution costs, credit exposure, in terms of inventories, and capital costs,” Perrotta said, “ETFs offer the market maker an efficient way to manage, transfer and hedge risk.”