By Monica Summerville, Head of Capital Markets, Celent

For buy side and sell side firms, alike, enhancing the customer experience (CX) is one of the top priorities driving IT strategies. Meeting—or exceeding—client expectations is central to good business. That’s true in capital markets, where focusing on client-centricity and client enablement is essential for effective implementation of tech initiatives, as I’ve addressed before.

This topic is worth an additional look at the start of 2025, when focusing on client-centric product innovation is one of the key business trends driving technology investments in capital markets, as detailed in Celent’s Capital Markets: Technology Trends Previsory 2025. Additional key business trends driving technology investment in capital markets in 2025 include balancing efficiency and innovation (where too much focus on cost-cutting can lead to missed opportunities); building NextGen ecosystems; establishing credibility and value in data; and navigating tactics, risk, and strategy across regulatory regimes.

Keeping a close eye on the possibilities for improved customer experience—and how investing in technology enables these enhancements—will always be valuable.

Technologies Converge to Support Client-Centricity

Today we’re seeing a convergence around emerging technologies, cloud computing, and data initiatives. Cloud adoption is high, with investment technology ecosystems migrating to the cloud, service providers consolidating data onto cloud infrastructures, and confidence growing as banks build cloud expertise and embrace cloud delivery models. Cloud is also an emerging technology enabler, such as for artificial intelligence (AI), quantum, and blockchain. As these new technologies come together, they can facilitate everything from new business approaches to new product and service proposition, digital interaction channels, and personalization of client relationships.

To ensure effective initiatives while embracing new technologies for the purpose of supporting client-centric product innovation, the imperative for a new approach is also becoming clear: financial institutions must de-silo their tech stacks and their “tech thinking.” Whereas before there may have been separate groups working on separate initiatives, firms are finding that they must bring these areas together to unlock the usefulness from their technologies. Similarly, firms are creating next generation data ecosystems which bring together sourcing, storage, management, analytics, and advanced technologies. to help facilitate initiatives.

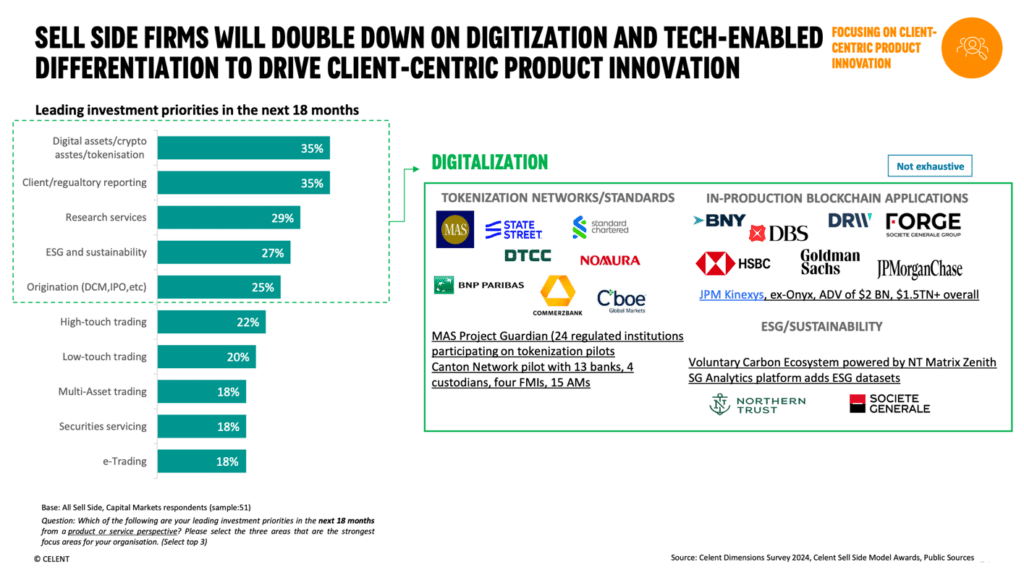

Sell Side Client-Centricity

Source: Celent

The sell side is doubling down on digitization and tech-enabled differentiation to drive client-centric product innovation. Leading investment priorities, as found in Celent’s 2024 Dimensions: IT Pressures & Priorities research include digital assets/crypto assets/tokenization; client/regulatory reporting; research services; environmental, social, and governance (ESG) and sustainability; and origination. Some ways that firms are taking action on these initiatives for digitalization include:

- Tokenization networks/standards: making digital plays across banks, custodians, and financial market infrastructures (FMIs), and asset managers to identify new services which can be offered in this space to meet client needs.

- Sustainability initiatives, driven with proprietary data and data sets, designed with client-centricity front and center. Societe Generale, for example, has added sustainability data sets to its in-house developed, and client accessible, Data & Analytics platform.

- In-production blockchain platforms from firms, such as Kinexys (formerly Onyx) from J.P. Morgan, that realized a need early on to innovate to meet the needs of clients.

Client-centric product innovation provides a range of opportunities. Firms can embrace opportunities to focus on unstructured data to improve communications. With great potential for both back office (where emails and faxes are still prevalent) and front offices. Emerging technologies, especially some of the new AI offerings, support opportunities for new products around data transfer, which leverage automation, to streamline and improve communications, and shorten onboarding cycles.

Firms also have new opportunities to cross-sell by focusing more holistically on the client. Technology now makes it possible for areas within a firm, which were once separated and operated as silos, sometimes for regulatory reasons, to be cross-sold. New technology taps into the potential to leverage adjacencies through cross-selling and up-selling at the group level, between banking units, while remaining compliant with securities, market abuse, and privacy rules. Examples here may include across: asset and liability management (ALM) and treasury and markets, looking at flow; wealth management and capital markets, for structured products, issuance, and product placements; transaction banking and capital markets, looking at foreign exchange (FX) or interest rate derivatives; or asset servicing and capital markets, in areas like collateral management and FX.

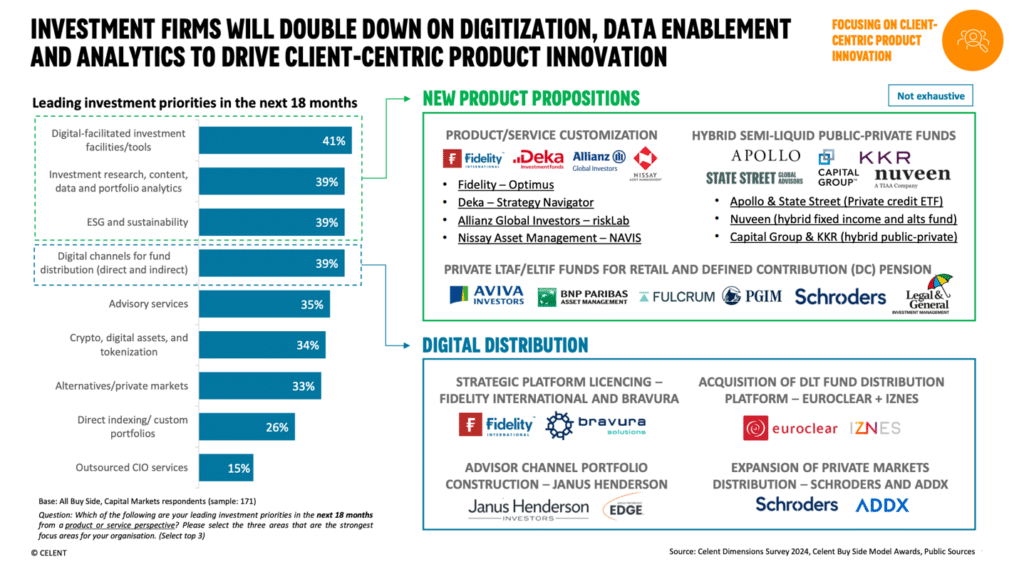

Buy Side Client-Centricity

Source: Celent

Similarly, as our team has found, the buy side is putting new energy into client-centric product innovation. Firms here are evolving from traditional analog distribution models to digitally-enabled strategies to engage advisors, allocators, and other intermediaries using technological capabilities, insights, content, and analytics. Various firms are building out digital channel capabilities and partnerships, such as product/service customization initiatives, new hybrid public/private product launches, and new opportunities for private asset investing in retail and defined contribution (DC) pensions.

What we’re likely to see in the coming year on the buy side will include scaled product innovation and hyper customization, which is becoming a core capability. Firms will look to enhance capabilities for faster product innovation and customization, aiming to counteract the ongoing pressures on margins. By developing tailored investment products and swiftly adapting to market demands, firms can differentiate themselves and attract a broad client base and ultimately improve profitability.

This emphasis on innovation will help mitigate margin compression, also allowing firms to better align offerings with the evolving needs of investors. Traditional and alternative investment managers are taking action around the expansion of private assets into non-institutional segments, such as defined-contribution pensions, private banks, wealth managers, and independent financial advisors that service a more retail-oriented client base. By expanding offerings to include alternative investments (private equity, credit, hedge funds, real estate, and other non-traditional assets), firms can cater to a wider-range of clients while seeking diversification and enhancing returns beyond traditional asset classes.

Private credit crossovers and collaborations, between banks and alternative/private credit managers, are set to grow. These are becoming increasingly prominent. As firms navigate the complexities of these opportunities and some of the involved risks, emphasis on digitization will likely grow as a means to optimize the private credit operations in terms of greater automation, efficiency, and more accurate information exchanges across the multiple participants.

Plan for Uncertainty, While Focusing on Client Needs

Technology needs to support capital markets firms, no matter what is thrown at them in the coming year. For a business to be agile, it must plan for uncertainty, all while embracing the technology that can not only support innovation goals, but meet current and prospective clients’ needs.