The old adage on Wall Street “If you want size, you have to reach” still applies when Michael Thom, head trader at Genus Capital Management, is looking to execute a large order. That is, he is willing to pay a premium to get the largest fill he can.

And that is important when your firm is in Vancouver, British Columbia, and trades less-liquid stocks in Canada. The Canadian market is only one-tenth the size of the U.S. equity market, and the majority of the stocks there are just not as liquid. But finding blocks can be difficult.

“Good liquidity always demands a premium,” Thom said. “And we’re happy to pay for liquidity. Our trading style tends to be more liquidity taking than providing, and we understand that there are costs associated with this style.”

He’ll also tap his brokers for capital for trading in names that are less liquid and difficult to find-if a natural contra doesn’t come his way. Roughly 20 percent of his trades involve capital.

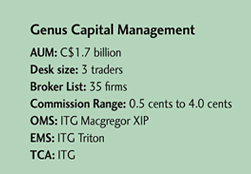

Genus’ three-person trading desk sends its orders not just to the Toronto Stock Exchange, but also to the growing number of alternative trading venues like Chi-X, Omega and Alpha. Thom also uses the growing number of dark pools in the country, which have grown from just two at the beginning of the year-Liquidnet and ITG-to seven. His desk allows Liquidnet to scrape its blotter.

“Liquidnet is our preferred dark venue, as we often find the size and blocks we want there,” said Thom, who began trading three years ago, when he joined Genus. “There is a lack of information leakage and the counterparties there tend to provide good contra liquidity in size that is relevant to us.”

Because Canada is shifting toward a more electronic marketplace, he believes the relevance of the buyside trader is growing. “I think given the much wider set of execution tools available that the trading desk is more important than ever,” he said. “Our knowledge of execution strategies, our relationships and our market intelligence have a very large impact on execution quality and ultimately the return on our investment strategy.”

And Thom has been adapting to and using the market’s newest tools, including algorithms. He has about 13 algo in his quiver but regularly uses two or three from a select group of providers. The desk generally uses arrival-price type, liquidity seeking and implementation shortfall algos for the 40 percent of its flow done via algos. The balance are either done high-touch or sent directly to dark pools.

“It is challenging to build an extremely high level of comfort with a specific algorithm from a specific provider,” Thom said, given the demands on his time. “We hope to do this with more providers and algorithms in the future, but it’s an onerous process.”