CBOE Holdings, buoyed by the phenomenal success of options and futures contracts based on its Volatility Index, is ratcheting up its efforts to broaden their appeal.

“The volatility business is only eight years old, but we see terrific growth,” Ed Tilly, CBOE’s president and chief operating officer, told a gathering of reporters in New York recently. “We see hedge funds, prop trading firms, (commodity trading advisors), insurance companies and other institutional users migrating to the product. It’s very important for us.”

As part of its marketing, CBOE is emphasizing to money managers and traders the growth of liquidity in the instruments and the attractiveness of adding a volatility component to their portfolios.

The exchange operator also plans to provide European institutions with direct access to CBOE matching engines, 24 hours a day, 5 days a week.

The Volatility Index, or VIX, is a measure of the market’s expectation of stock market swings over the next 30 days, as determined by the performance of options on the Standard & Poor’s 500 Index. Trading in both contracts has soared in the past three years, with growth in the futures product especially dramatic.

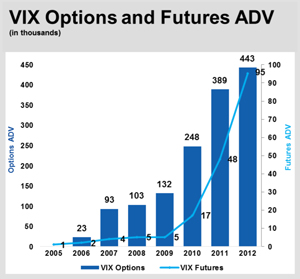

Last year, average daily volume in VIX futures—traded at the CBOE Futures Exchange—reached 95,000 contracts, up from 5,000 in 2009. Average daily volume in VIX options—traded at the Chicago Board Options Exchange— reached 443,000 contracts, up from 132,000 in 2009. All this while overall options volume fell in 2012 and volatility itself was relatively muted.

Behind the surge in interest in both products was the financial crisis of 2008, which propelled the VIX to a high of 79.13 on October 20. It had been trading at under 21 at the end of August.

Barclays Bank set the stage when it released its VXX iPath S&P 500 VIX Short Term Futures exchange-traded note in 2008, giving users a more direct way to gain exposure to volatility. Other financial institutions soon brought out similar exchange traded products. In managing the securities, the firms had to hedge by trading VIX options and futures.

The explosion in volume, however, didn’t occur until 2010 when traders sought out exposure to volatility directly by trading the VIX futures and options contracts themselves. Players such as proprietary traders and hedge funds have jumped into VIX trading, and their volume now surpasses that of the ETP sponsors.

“Whereas before, folks might have traded the VXX ETP as exposure to volatility, now they are direct users of the futures product or even the options product,” explained Jim Lubin, managing director of CBOE Futures Exchange.

The growing liquidity in the product has encouraged the CBOE to step up its marketing of the products. To money managers, it is suggesting they consider volatility as welcome addition to their portfolios, or an asset class in its own right. “Volatility as an asset class really offers a new opportunity for these participants,” Lubin said. “It allows them to diversify away from their traditional holdings.”

To appeal to European traders, CBOE is building a “point-of-presence” telecommunications hub in London with direct connectivity to its U.S.-based matching engines and will soon offer trading 24 hours per day, five days a week.

The VIX finished at 12.88 Friday, near its lowest point since the credit crisis peak.