After 30+ years of Wall St experience, I took the plunge into crypto last year to start CoinRoutes with my son (his idea & code) to automate crypto trading across exchanges and help investors navigate a fragmented market. As we have progressed, I have been struck by the different perspectives of the crypto community vis a vis traditional financial professionals. The title of this article represents my opinion that crypto is here to stay, both as an asset class and as a technology that will improve other asset classes, but that the market and its denizens need to mature.

The confusion in the title refers to certain crypto community views that reflect a lack of understanding of financial market principles. Notably the beliefs that decentralization is a goal, in and of itself, and that regulation has little real purpose, but rather is a tool of entrenched interests to create barriers to potential competitors. These confused views are troubling, since price discovery requires some method for orders to interact and the crypto markets are immature, lacking basic mechanisms to facilitate pan-market transparency, fair access and investor protection. The delusion, however, refers to the view of many financial traditionalists that crypto assets are a bubble destined to go to zero and are only useful as a haven for drug dealers and scammers. The reality, in my opinion, is that crypto-assets will ultimately herald a major step forward in financial markets, with lower transfer costs, democratized access to platforms and an ability to program rules into transparent systems.

This gap in understanding between these perspectives is a problem. The misconceptions of the crypto community coupled with a lack of understanding on the part of traditional financial executives, play a large role in explaining why the crypto-markets are immature. Ignoring the luddite views of some in the financial community, there are sufficient opinion leaders, both at banks and at regulators such as the SEC, FINRA, and the CFTC that do appreciate the potential of crypto assets and technology, to help guide the maturation process. For that to occur, however, the crypto-community is going to have to gain a better understanding of how modern market structure evolved and the role of regulation in that evolution.

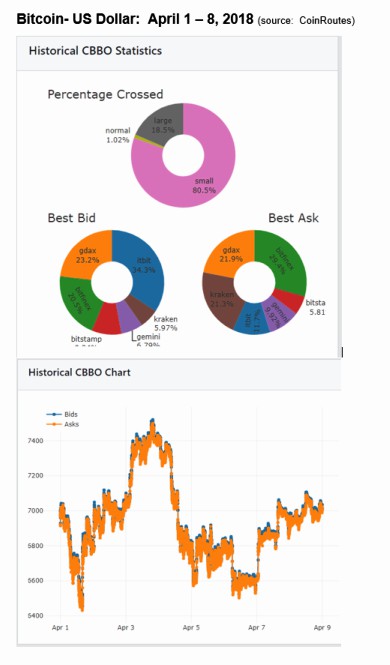

To begin with, lets analyze the common perception in the crypto sphere that decentralization is always better. To be sure, decentralized networks provide benefits of redundancy and robustness, are much harder to subvert, and are more democratic. In the case of price discovery, however, there is a need for orders from widely different sources to compete with one another. When orders compete to be the best price, whether on a central limit order book or via competing books it builds liquidity and lowers trading costs. In todays crypto markets however, the order books, including those operated by the largest crypto exchanges, dont compete. Most of the time, the best bid on one of the largest books is higher than the best offer on one of the others, meaning that the market is crossed. In addition, it is not easy to predict which of the exchanges, at any point in time, will be the best bid or the best offer. What is lacking are networks to provide clients a consolidated view of all such books, which is why we built CoinRoutes. Without software like ours, it is extremely hard to determine the price of a crypto asset at any point in time, making both valuation and achieving best execution very challenging. To put this in perspective, CoinRoutes data shows in the following charts, for the first week of April, Bitcoin traded in US dollars was crossed 98.98% of the time and there were at least 5 exchanges whose prices one would need to consider when deciding what the actual price of Bitcoin (in dollars) is, at any individual point in time.

Resolving this pricing uncertainty would be extremely beneficial to the community, however, asthe SEC has used the uncertainty over the price of bitcoin to reject ETF proposalsin the past. More broadly, institutional investors have concerns about both the accuracy of pricing and the market structure used to trade crypto assets.

To be clear, I amnotdefending a fully centralized market model, but rather arguing for the importance of displayed order books and the aggregation of such books. They could be run on DEXs (facilitated by 0x or other protocols) or be implemented as centralized models. The important point is that displayed order books allow many different types of market participants to interact, and that interaction is critical for a mature market. Different participant types include:

- Retail investors – trade small size, without sophistication, tend to buy and hold

- Large Funds (Institutions) – trade large size, holding periods of weeks, months, or longer

- Professionals (day traders) – trade medium size, holding periods of hours or days

- Medium to small funds (Institutions) – trade medium size, holding periods of weeks, months, or longer

- Arbitrageurs – trade opportunistically either based on visible mispricing or statistical anomalies

- Market makers – trade on both sides at a high velocity and hedge a book of many assets

- Quant traders- trade opportunistically, either based on short term patterns or imbalances in the order book or on longer term signals

- Speculators – trade for any number of reasons, but one sided and timescale can vary substantially

- Miners or crypto insiders – natural sellers of assets, either from holdings or activities

A mature, well-functioning market will facilitate the interaction of all these participant types and more. This leads to a more liquid market, with low transaction costs, particularly compared to markets that are focused on a small subset of the above. Perhaps more important, such a development would likely help attract institutional investors into the crypto market. This is because there are 3 keys for an institution to consider trading an asset class: Liquidity, Fairness, and Reliable Pricing. Lets analyze each:

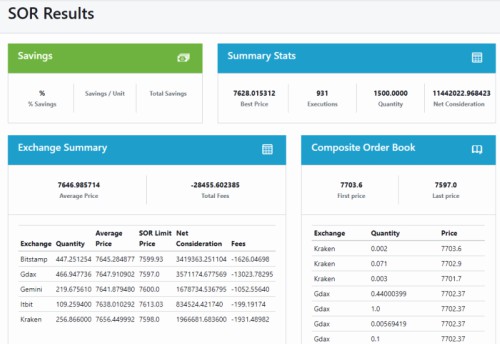

Liquidity: While liquidity is already pretty good in the market, the problem faced by many current funds is that they require Smart Order Routing software, such as we offer at CoinRoutes to find it. To illustrate, using our Cost Calculator, we show that orders over $10 million USD in Bitcoin can be traded, inclusive of exchange fees, for not much more than 1%. To do so, however, it is necessary to trade on multiple exchanges simultaneously. In the following example, which depicts an aggressive sell of 1500 Bitcoin (worth over $11.4 million at the time of the example), CoinRoutes cost calculator shows that the entire position could be liquidated immediately at a price of $7628.02 (net of fees), while the highest bid across exchanges was 7703.6. That corresponds to a total cost of roughly 1%, including roughly 0.25% of fees. That cost is lower, and the available liquidity is higher than most participants I talk to believe is available on the displayed markets. To accomplish this, however, a client would need a smart router to send orders to five different exchanges simultaneously, as depicted in the following screenshot:

Thus, it is fair to say that the market already has a critical mass of liquidity, but that participants need better tools for finding and interacting with it. This bodes well for the future, as such tools will eventually grow in popularity and become widely used.

Fairness: This relates directly to the second area of confusion namely an underappreciation for financial market regulation. Proper regulation can help assure institutional investors in many ways. For example, in the crypto markets, claims of spoofing, wash trading and other activities have been alleged repeatedly. While troubling, the lack of consistent regulatory oversight means that institutions evaluating the market have no way to know if those allegations are true. In addition, there are rumors of special deals for individual clients with respect to both data and market access. Proper regulation could address those concerns if true or disprove them if they are false. Lastly, proper regulation could address conflicts of interest in the business models of some participants. One example is a firm that operates a retail brokerage, a trading venue, an institutional desk, and is building an index fund management business as well. All of these are reportedly being set up in a vertically integrated manner which could create conflicts of interest. In the securities world, such a firm would likely need to divest some of these businesses, or, at a minimum, would need properly documented procedures and information barriers to be able to operate. With proper regulatory oversight, however, clients could have more confidence that such conflicts are being addressed. As a result, it is likely that regulation of the firms trading crypto assets as brokers and the exchanges as ATSs would improve the confidence of institutional investors.

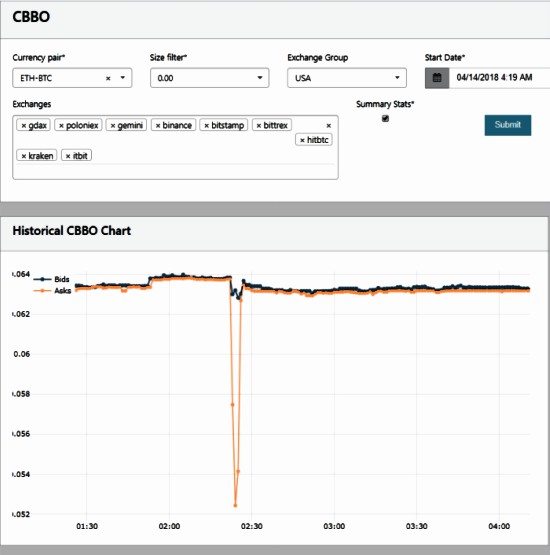

Pricing: The main issue with price formation in the crypto sphere is a lack of consolidated information for best execution or valuation. Examples of best execution problems at exchanges happen all too frequently. For example, this morning, on Poloniex, there was a flash event where in the Ethereum – Bitcoin pair, a large seller on Poloniex triggered a double-digit percentage collapse in the price, while ignoring the other exchanges as shown here by the CoinRoutes software.

As discussed above, this is a primary reason that the SEC has, so far, not approved Bitcoin ETFs and is also an issue for institutional participation in the crypto markets. If, however, exchanges utilized consolidated pricing as guardrails to ensure that they did not execute wildly out of line from other exchanges, it would be welcomed by institutional investors. For their part, institutions would also need quality consolidated pricing for both valuation and to meet their best execution obligations.

In conclusion, we believe that bridging the gap in beliefs between crypto world and traditional finance will be very positive. If that leads to constructive regulation that improves investor confidence, it could well bring more institutional participation into the market. That is probably why recent articles suggestedthat registering the exchanges that trade crypto-assets will assist bitcoin ETF issuers with gaining approval fromthe SEC. That process, however, is going to require changes in approach to best execution, price data dissemination, and the resolution of conflicts of interest. It will be interesting to watch the progress as the market matures.

David Weisberger is CEO and Founder of CoinRoutes