Credit Suisse has stopped reporting trading volume data to industry record-keepers for Crossfinder, the largest dark pool of orders for trading of U.S. equities.

The international financial services group is no longer reporting equities trading activity of Crossfinder to Tabb Group or Rosenblatt Securities, each of which keeps track of market shares of dark pools. The two industry consultancies get their data from broker-dealers and other dark venue operators.

“While we are disappointed that Credit Suisse has decided to stop reporting, it is hard to argue that continued self-reporting would do them much good,” said Adam Sussman, analyst at Tabb Group in a statement. “We still feel it is important for the industry to continue to try to measure these numbers so we have no plans to cancel LiquidityMatrix. At least until regulators feel the same and put in place a better way for the industry to measure the volume and impact of different trading mechanisms.”

Justin Schack, managing director at Rosenblatt Securities confirmed to Traders Magazine that Credit Suisse “is no longer reporting data to us for Crossfinder in the U.S.”

“We’re disappointed with Credit Suisse’s decision, but respect that the firm must ultimately do what it believes is best for its business,’’ Schack said.

Credit Suisse spokeswoman Katherine Herring declined to comment.

Merrill Lynch Bank of America, JPMorgan and Fidelity Capital Markets also do not report their dark pool volumes.

According to the latest report from Rosenblatt Securities, dark pool market share in February executed 14.26 percent of consolidated U.S. equity volume in February, down from January’s 14.33 percent level. Crossfinder reported trading of 123.1 million shares or 13 percent of volume reported by dark pools in the Rosenblatt survey. Crossfinder also accounted for 1.9% of total consolidated trading in equities, lit and dark.

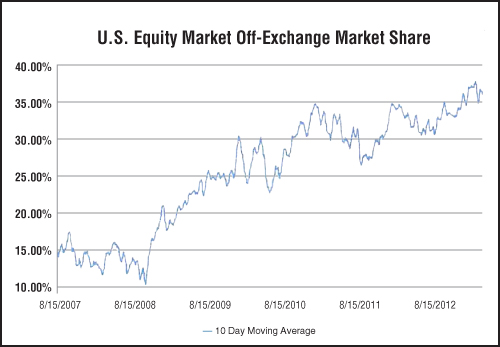

The move could affect market debate on whether dark pools help or hurt the equities market. Public exchanges, such the New York Stock Exchange and the Nasdaq Stock Market, have seen their trading volumes shrink over the last several years as volume in private dark pools has increased. Over the last five days, off-exchange trading has accounted for 33.26 percent of total trading in equities, according to BATS Global Markets data based on transactions reported to the Financial Industry Regulatory Authority’s Trade Reporting Facility. The percentage was less than half that five years ago, according to a U.S. Market Structure Update prepared this month by exchange operators.

That update was prepared for an April 9 meeting by the chief executives of NYSE Euronext, Nasdaq OMX Group and BATS Global Markets with Securities and Exchange Commission member Dan Gallagher on April 9 to discuss the topic of on- versus off-exchange trading. The exchanges argue that trading in the dark pools hurts open price discovery, harms liquidity and benefits the broker-dealers who run these pools.

The dark pools, a majority of which are run by the bulge bracket brokers, counter that they help maintain liquidity, provide price discovery and improvement and offer users more anonymity than the public venues.

Credit Suisse has said that the exchanges are distorting the argument by leading Washington and regulators to believe the exchanges only trade in the light. Exchanges use, the brokers counter, “hidden orders” or orders that only display a portion of an order and keep the rest hidden from view. Credit Suisse said these hidden orders and other similar order types are essentially no different than trading in a dark pool.

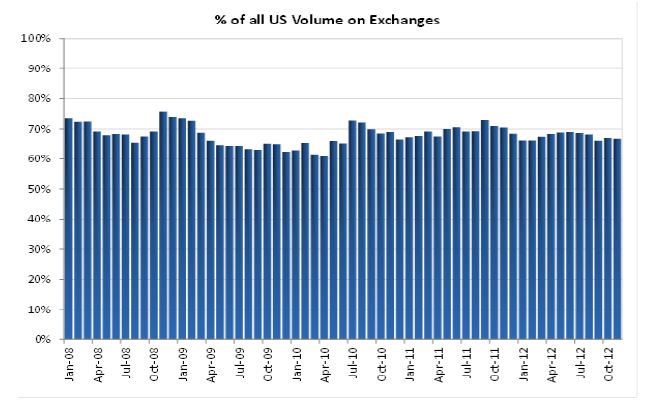

In December, Dan Mathisson, the head of U.S. Equity Trading for Credit Suisse, testified before the Senate Banking Committee on Securities, Insurance and Investment that volume has not shifted to off-exchange venues over the period from January 2008 through November 2012. “The percentage of volume executed off-exchange has been remarkably constant over the past five years,’’ he said.