By Kelvin To, Founder And President Of Data Boiler Technologies

Kelvin To

Market data reform was originally a raised concern for fairness of access and cost burden for market participants. The Financial Conduct Authority (FCA) said the Consolidated Tape (CT) for UK equities would not happen until 2028 is in effect a diplomatic move without saying the obvious. The European Securities and Markets Authority (ESMA) MiFIR Review Final Report contains FATAL FLAWS that will lead the European equities markets to a death spiral. Switzerland is NOT a part of the EU. It may sit on the fence and observe if other National Competent Authorities (NCAs) REJECT this faulted ‘Regulatory Technical Standards’ (RTS) at the European Commission (EC) level. Meanwhile, the US Market Data Infrastructure Rule (MDIR) is set to be implemented in November 2025 with odd-lot information to be included by May 2026. The following pinpoints the key flaws and how to turn it around positively for the best interest of investment firms and the overall markets.

Flaw #1: Timing Mismatch of European Best Bid & Offer (EBBO) and the Most Relevant Market in terms of Liquidity (MRMTL)

ESMA opted for anonymity of trading venue with the best price, yet they ask the CT provider to show the MRMTL that is calculated annually per Article 4 of Commission Delegated Regulation 2017/587, alongside the real-time EBBO. The public will be misled! It is a deliberate act to direct order flow to the larger exchanges, when the smaller / remote exchanges or multilateral trading facilities may have the best price and sufficient quantities to fill orders. Not only is it counter-productive to the CMU or the new ‘Savings and Investment Union’ (SIU) objective, with its intent to “attract institutional investor participation, better connect savers and borrowers irrespective of their geographical location, and ensure that ordinary savers can benefit from the wealth creation of the corporate sector”, Europe is digging its own grave – money would flee when markets can no longer be trusted!

Flaw #2: One single currency to represent both the best bid and the best offer in Europe

Following Flaw #1, where larger exchanges have dominated turnover volume, especially during close and/or open. It is likely that smaller or remote trading venues will rarely be reported on the MRMTL because of the bias. The next distortion is which currency to show for EBBO. Securities in Europe can be denominated in various currencies other than Euro. The best bid could be in Swedish Krona, while the best offer in Sterling Pound, or vice versa or a mix of different currencies. Pairing the best bid and the best offer is indeed concentrating volume at the larger exchanges. It reduces the serendipity of cross-market trading opportunities. Rail ticketing in Europe accepts different currencies. It is one of its conveniences, how can the EU equities CT not to have real-time multi-currencies capabilities?!

Flaw #3: Tolerating latency timeliness standards and leaving loopholes for ecosystem degradations

It is totally practical for CT to mimic how High Frequency Trading firms (HFTs) aggregate ultra-low latency data across venues. Yet, ESMA relaxes the “as close to real time as technically possible” clause to allow Exchanges and Approved Publication Arrangements (APAs) transmit data to the CT Providers within 50 milliseconds with a 95% confidence interval from the timestamp of the order submission for pre-trade data. The Europe CT’s benchmark should be at least better than the US SIP realized latency in tens of microseconds, amid those that subscribe to PPs are receiving more detailed data in nanoseconds or microseconds at most. One of the US Consolidated Audit Trail fatal flaws is its 50± milliseconds tolerance. Hundreds-of-thousands trade messages at any given point in time is not suitable for analytics. Although ESMA preserved the timestamp granularity for trading venues with a gateway-to-gateway latency below 1 millisecond to be set at 0.1 microseconds, the amendment to Regulation (EU) No 648/2012, and Article 22c grants a Maximum Divergence from UTC of 100 microseconds is a loophole. There is no obligation for Exchanges or APAs to report “clock drift averages and peaks and number of instances of clock drift greater than 100 microseconds”.

The ESMA’s expectation of “data contributors send the data to the CT Provider as soon as possible and without artificial delays compared to sending of data for other purposes, including proprietary feeds, to meet such requirements” is substantially weaker than the US Securities and Exchange Commission (SEC) Rule 603(a) that “prohibits an SRO from making NMS information available to any person on a more timely basis.” The SEC recognizes the Securities Information Processors (SIPs) were not modernized alongside markets evolution and technologies development; therefore, it requires the “same manner same methods” provision (see page 186 or footnotes 608 and 609 of MDIR). Yet, we argue that the US SEC MDIR does not go far enough because Co-location ≠ Latency equalization ≠ Market data available Securely in Synchronized Time.

Shared versus dedicated switch, temperature, network time rather than precision time protocol, etc. can affect performance and influence the EBBO spread. What you see may not be what you get. One will need to upgrade to higher bandwidths and add depth-of-book data, or else face being disadvantaged to proprietary feed subscribers. Trading venues’ products differences are often determining success or failure in a few nanoseconds and/or altering bandwidth for blocks. Losing a few basis points per trade could accumulate to hundreds of millions if not a billion.

Flaw #4: Crappy clauses such as ‘authentication, authorization, and non-repudiation’ is within the RTS requirement

Did ESMA forget that they once acknowledged these concerns raised by market participants – “(i) onerous administrative obligations on data users, for example through frequent and detailed requests on the use of data; (ii) ambiguous language in the agreement; (iii) frequent unilateral amendments to the agreement; (iv) general lack of transparency on terms and conditions; (iv) excessive fees; (v) increase of fees through penalties; and (iv) overly burdensome audits”?! Investment firms want to have Enterprise license with free redistribution on ‘fair use’ basis, rather than all the onerous and burdensome charges per device, professional/ non-professional users fees, and restricted redistribution of data contents that were originally belongs to the broker-dealers themselves. The Facebook case affirmed that contents (quotes and trades contributions) belong to the content creators (broker-dealers with passthrough back to retail), NOT the streaming platforms (stock exchanges). Empirical evidence proves Exchanges optimally restricting access to price information is undeniable. It exacerbated the latency gap between Proprietary Products (PPs) and CT that caused data fragmentation. If NCAs are not rejecting the faulted RTS at the EC level, the public would feel betrayal. Elites in alleged cahoots with politicians rather than upholding justice leads to social unrest and possible change in regimes as seen all around the world.

Flaw #5: Denial of innovations and lack understanding of how encryption can level playing field and lower costs

ESMA’s statement of “innovation-related aspects are not of direct relevance to the specific nature of the proposed RTS on the input/output data RTS” reflected their naivety. Not sure if this poorly written EC equities DEG report (that I refused to have my name affiliated with) has swayed the RTS. I urge policy makers around the world and the broader industry to distinguish truths versus myths.

EuroCTP partners with Amazon Cloud, may use AWS “time sync service” over Network Time Protocol (NTP) has an observed accuracy around 400 microseconds that is insufficient for some applications that require even higher precision. We at Data Boiler advocate for Precision Time Protocol (PTP) which is widely used by HFTs and is substantiated to improve performance and reduce the observed error to under a microsecond (see this). The unmerited or non-substantiated “stab” at PTP by the EC equities DEG report was ‘a clumsy denial resulting in self-exposure’ of their incapabilities.

Field program gate array (FPGA) enables execution of a trade at as little as 13.9 nanoseconds which is documented in the STAC-T0 benchmark report. FPGA hardware acceleration can reduce server resource consumption by as much as 10-20 times. FPGA has been adopted in processing market data with tremendous successes, blowing the competition away.

Time-lock encryption (TLE) was first invented in 1976, the widely used RSA algorithm was used since 1999. Even the online gaming industry is using it to promote fairness, yet the electronic trading equities market is behind. Those who can afford proprietary feeds or data center co-located trading venues have an unfair advantage to access market data ahead of the general public and the remote venues. The phenomenon is like Animal Farm.

The purpose of requiring Encryption is NOT ONLY about confidentiality of data. Given the geographic disperse of trading venues, the way for CT to overcome ‘latency hop’ is by having a SECURE and SYNCHRONIZED start line and going fast by traveling light (i.e. streaming only the essential core data for pre-trade equities tape with data compression). TLE eliminates the problem of where the CT data center is located. Thus, the financial industry no longer needs to be subservient to telecom vendors and move away from overcrowded data centers to other remote locations that offer cheaper prices, hence saving money for the public in the long-term.

Indeed, one of the root causes of rising market data and connectivity costs is related to trading venues passing on fee increases by data centers and telecom infrastructure vendors to market participants. The latency arms race bids up the infrastructure costs and waste energy. If TLE can be implemented throughout the US, Texas Stock Exchange and other trading venues’ data centers would not need to be concentrated in or near Secaucus, Mahwah, Carteret, but could move back to their home states to benefit the local economy and lower costs. Same goes with Europe.

As trading volume may be maturing in London, Paris, and Frankfurt (amid “participants on Euronext Paris and London Stock Exchange set a new EBBO price substantially more frequently than CBOE, Aquis, and Turquoise… In Germany, Xetra improves the EBBO less often than both Aquis and CBOE” per research by Plato Partnership), Eastern Europe presents itself at a driver of fast growth for the EU. Eastern Europe may replicate the success of Nordic markets in equities trading despite their currencies not being denominated in Euro. TLE would provide seamless trading experience across Europe and infuse trust by providing a level playing field to draw institutional and retail investors to increase participation. Nevertheless, CMU / SIU emphasized “irrespective of their geographical location”. Instead of skewing policies toward Euro based trading centers in central Europe, let’s give smaller and remote trading venues a fighting chance to flourish by adopting TLE.

The seldomly talk secret ingredients of how the US equities markets have structurally advantages over Europe and others:

Canada spent approximate 60% of their retail trading platforms’ total cost on subscription and redistribution of market data. Europe and other regions would not be far off from this number if they purchase depth-of-book feeds from respective trading venues or non-display vendors. Whereas in the US, non-display direct access is indeed subsidizing display indirect / internet access, hence US retail platforms are able to offer zero trading commission and other investor education programs that other markets cannot.

Investment firms in the US, including Self-Aggregators (SAs) and Alternative Trading Systems (ATSs), the equivalent of Multilateral Trading Facilities (MTFs) in Europe, connect to 30+% less trading venues in average instead of all the 11 most active PPs to save costs. This SIFMA / BCG analysis provides valuable insights into different categories of firms and their respective spending on a mix of the US SIP / CT with selected PPs. One does not need to know how many people are in queues of all markets across European markets if he/she may be shopping within neighborhood distance.

From the NASDAQ SIP Accounting 101, tech / running cost is approximately 6% of SIP total revenue, the remaining US$424 million per annum in quote and trade revenue are indeed being split between trading venues to divide the cake. This source of income from ‘Revenue Distribution Scheme’ (RDS) in turn is used by Exchanges to pay for ‘access fee rebates’, similar to market-makers’ payment for order flow (PFOF). Park aside the alleged potential conflict of interest, to some extent the rebates serve in effect as an incentive or a royalty payment to reward the order flows bring-in by the elites (see this). The US$400+ million can be used towards a lot of good, the only trouble is – the payout is not standardized, i.e. some got 32 mils in super tier rebates, some got nothing. The SEC’s access fee cap update is a wrong dose of medication, the ‘Haves’ never worry about insufficient incentives to go around in markets because they can exploit or squeeze the ‘Have-Not’ (see this).

Amid the EU goes with ‘Reasonable Commercial Basis’ (RCB) for regulatory price control, and the elements of RDS consisted of ‘small trading venue’, ‘young instruments’, and ‘pre-trade transparent trading venue’ that carry the highest to lowest respective weight in computing how the cake would be divided. It omitted a key component of an equitable incentive to reward broker-dealers and trading platforms on new natural liquidity in improving the overall trading volume of European markets. Do not get us wrong, we are NOT against stock exchanges. Just that RDS should cover data, connectivity, and API testing costs, while any upside of revenue sharing to trading venues and APAs should be based on growing the overall pie in increasing the Europe markets total trading volume, rather than compensate for potential lost in PP revenue.

We at Data Boiler, computed 5 scenarios:

Scenario 1 (S1) is a Display indirect / internet access CT that is priced with onerous fee categories similar to the existing PPs or the US SIPs. Without the non-display direct access subsidization, trading venues’ lead CT contender(s) would not mind the CT acting as a “SECOND LINE PRODUCT”, fund and pay for by the public to generate additional profits for them, so long as CT does not compete with PPs. S1 would push “total spend” on equities market data and connectivity across PPs, vendors’ solutions, and CT to be up at least 5% on top of a year-on-year increase of 7.1%.

S2 is a scenario modeled after the US SIP’s subscription mix, where approximately one-third of CT subscribers would choose non-display direct access. Our results show that, not only S2 can proportionally lower price to both direct and indirect access fees by at least 15% than S1, the onerous of per device, prof. vs non-prof. users, redistribution fees can also be waived to grant investment firms the enterprise license in ‘fair use’ of data per their request. We envisage S2 would avert the 7.1% year-on-year increase and lower the “total spend” by 1.5%.

S3 is a scenario where direct access subscription reached critical mass. S3’s price can proportionally lower by up to 20% than S2, while the subsidization effect would lower the indirect / internet access fee to as little as €100 per month, assuming an annual cost of living adjustment of 3% compares to today’s inflation rate. We believe if more market participants adopt electronic trading and encourages cross-trade over 2 or more platforms (especially for trading venues in remote locations) would improve the 4Vs – ‘variety’ and ‘veracity’ in price discovery, ‘velocity’ in EBBO refresh rate, and total trading ‘volume’ for healthy development of European markets. Under S3, we envisage the industry would yield over 5%, or over US$100 million, in overall savings on their “total spend”.

While S3 is the optimal point, where CT Provider should be rewarded in delivering a truly usable CT in benefiting the investing community, we simulate a S4 scenario to assume further price drop of CT in an intense rivalry with the PPs. We foresee the “total spend” would achieve 10+% savings, which is good for the markets but hurting trading venues and a diminishing return for the CT Provider. Our pricing mechanism ensures a smooth transition to new equilibrium rather than overly disruptive to shaking the bread-and-butter of Exchanges’ PPs’ revenue stream.

S5 is a full-fledged price war scenario, where the frienemies equilibrium between CT Provider and vendors’ value-added services would be broken for a 20+% reduction in “total spend” compares to today’s market size. Under S5 the diminishing return for CT Provider would exacerbate (back to S1 or S2), while some smaller vendors may not survive or be merged with larger players. The evolution from S1 to S5 could be a roadmap for a healthy market data reform over a 10-years racecourse with flexibility to respond to changes in PP, vendors, and CT dynamics. The mechanism sets the CT as a reasonable compromise, but not a close substitute product to PPs, while encouraging modernization of CT alongside markets evolution and technologies development. It is the ONLY effective way to achieve the regulatory goal in applying the right amount of “competitive pressures for existing sellers of market data, resulting in cheaper, higher quality and more accessible data for its users.”

Amid the initial cost and energy consumption would likely be higher for the CT Provider in the beginning years, the year-on-year multi-millions in savings and the benefits of a constant refreshing tight spread EBBO to the industry will out weight its costs. This CT business model is viable because different needs in the markets will be fulfilled and enhances the competitiveness of European markets. Rather than letting trading venues split the cake of about US$200 million a year under RDS and creating more data fragmentation to convolute the ecosystem, our proposed mechanism would craft out certain percentages of revenue as Rebates* to investment firms (IFs) on top of the pricing discount as described in S1-S5.

IFs may use the rebates* towards investment in the CT Provider for dividends/ profit sharing, as well as obtaining board seats to improve governance. Rebates may also be used towards purchase of value-added services with affiliated vendors, or cash out at a discount (given this substantial amount nevertheless is an incentive to drive increased trading volume to Europe).

CT Provider oversees data suppliers to address the 3 main causes of Data Quality problems + Value-added Services:

Trading venues’ PPs exacerbate the data fragmentation issue and is unfair to latency disadvantaged market participants. There are 3 main causes of Data Quality problems:

Man made issues for self-interest and favoritism: e.g., crappy data (i.e., 100,000 messages at any given point in time that mussed everything up) and/or hold off the advancement of CT for ecosystem degradation to exacerbate gap between PPs and CT. CT with a wide bid-ask spread and delay refreshing of the US National / European best bid offer (NBBO/ EBBO), i.e., to make the tape unsuitable for Best Execution (BestEx) analysis, in turn, majority of market participants are not aware that they have been receiving inferior price.

Inadvertent or honest mistakes during trade reporting, such as duplicated positions and/or misuse of taxonomy flag(s) by IFs during trade reporting to APAs. CT Provider in its consolidated trade system is required to pass along a ‘duplicated positions’ flag, or such, to data subscribers, while awaiting regulator to investigate potentially erroneous information, typically reviewing event lifecycle details in clearing and settlement system. CT Provider must NOT add, amend, or remove any data, except at the direction and discretion of the regulator. APAs as a Trade Reporting Facility (TRF) may allow a, e.g. 5%, tolerance level before taking action against an IF.

This empirical research uncovered a “preferencing” phenomena. The finding shows that “86% of all reported off-exchange trading volume, trades reported in the NASDAQ TRF experience significantly poorer execution quality.” Be mindful if trading venues lead contenders / APAs may influence off-exchange fragmentation and reporting across APAs if they become the CT Provider to benefit from the RDS using daily trading volume to divide the cake. We will curb any inequitable access, degradation, or exploitation issues, and prevent any attempts (be it intentional or unintentional caused by trading venues/ APAs’ competition) that impair the interests of IFs.

Do NOT believe those who claim some taxonomy “flags” would magically help you profile liquidity. By no means we are critical to FIX MMT that serves regulatory transparency purpose. The truth is liquidity in equities electronic trading or best execution involves comprehensive analysis. Fill rate, execution speed, effective versus realized spread, order-to-execution ratio, VWAP, slippage, etc. are some of the common metrics. Yet, metrics are rarely effective to deal with rapidly evolving issues proliferated by hidden problems and silos.

Be in the know of techniques such as tracking and responding to the level of toxic (or likely toxic) orders, deciphering dynamics of HFT activities and adverse selection, assessing market makers’ risk profile and market timing, and recognizing that hidden orders could be placed deep down away from the best quotes. Including five price levels in CT / SIP is no safe bet that markets would not come up with a workaround. Optimization between speed and richness of contents would be an ongoing exercise to response to competition with both PPs and other jurisdictions. If Europe regulators and investment firms have concerns with “order duplication and liquidity measurement in EU equity markets”, data vendors may provide “values-added services” to offer such intelligence on HFTs’ propensity of cancellation or sponsor academic studies on related implications to toxic versus natural liquidity. Yet, these are outside CT Provider’s scope of responsibilities of aggregate and disseminate market data.

NOTE: HFTs are indeed taking risks in their multiple positions. They are obligated to take the exposures if unmatched orders are not cancelled in time. Under no circumstances can the CT Providers curb HFTs legally permissible activities in cancelling orders. The capabilities difference between lit exchanges, MTFs, and Systematic Internalizers may be a worthwhile but are a separate topic to market data reform that policy makers around the world should consider.

Other Remarks and Conclusions:

Do not underestimate the negative consequences where a faulted RTS can hurt the overall Europe markets. If NCAs lets the EC approve it “as-is”, market participants would lose faith in the integrity of European markets. The public is no fool, divest money away or social unrest to protest an unfair system are their options. The only interested parties to seek trading opportunities in Europe would be those who can exploit and segment order flow away from the EU. We will wait and see how the Switzerland and the UK would play out when the EU markets go down the drain. However, a death spiral in one market is likely contagious to others. Inadvertently, the negative sentiment or mistrust towards the EU capital markets may also spread globally to affect the US.

Act now to REJECT the faulted RTS in the EU and the disastrous report by ‘Europe Economics’ in the UK. Remember: CT / EBBO is an advertised price. Low intensity competition among CT, PPs, and vendors’ solutions per the 5 scenarios we looked at, indeed maximize and optimize the promotion of European markets. By infusing trust through TLE and facilitate increase cross-platforms trading (give smaller/ remote trading venues a fighting chance), that is the ONLY way to achieve the desire outcomes of CMU / SIU – “attract institutional investor participation, better connect savers and borrowers irrespective of their geographical location, and ensure that ordinary savers can benefit from the wealth creation of the corporate sector.”

There are plenty of low-latency infrastructure data vendors out there. Think about why none have emerged to become the equities CT contender thus far. Think about why Europe failed to attract expatriates. How sad that even HSBC, a prominent global bank with their headquarters in UK, is retreating from the equities market. It is now or never to encourage investments to turnaround the Europe markets’ weaknesses. Like laying new high speed rail network for the next century, why should FinTech go about investing in Europe instead of other jurisdictions? We pour our heart out to provide our open and honest comments. At Data Boiler, we already located an expansion team in Europe and will bring the world best talents to support the sustainable development of the Europe markets. Moving on, we may consider the competing consolidator and other opportunities in the US and around the world. Contact us if you are interested to learn more.

Cboe Global Markets (Cboe) is the latest exchange to announce plans to implement 24-hour equities trading, and it won’t be the last, according to Sylvain Thieullent, CEO at Horizon Trading Solutions.

“Traditionally limited to asset classes like FX and digital assets, exchanges are now looking to facilitate extended trading hours to adapt to an increasingly global market landscape,” he told Traders Magazine.

Sylvain Thieullent

“However, trading in the middle of night requires technology systems that have the unwavering level of speed and precision needed to navigate potentially volatile markets,” he added.

Thieullent said that liquidity is also likely to be thinner outside of regular trading hours, which can make it difficult for high-speed traders to execute trades at desired prices.

“Realistically, it is sophisticated algorithms that are able to analyse extensive volumes of data, detecting patterns, and executing trades with split-second precision that will determine who is able to capitalise most from this trend among global exchanges,” he said.

On Monday, February 3, Cboe Global Markets announced plans to offer 24-hour, five-days-a-week (24×5) trading for U.S. equities on its Cboe EDGX Equities Exchange (EDGX), subject to regulatory review and industry developments.

The proposed expansion aims to meet growing global customer demand for expanded access to U.S. equities markets.

“We continue to hear from market participants globally – particularly those in Asia Pacific markets like Hong Kong, Japan, Korea, Singapore and Australia – that they want greater access to U.S. equities trading and need trusted venues that can offer transparency, robust liquidity and efficient price discovery,” said Oliver Sung, Head of North American Equities at Cboe Global Markets.

“As the world’s largest global exchange operator, Cboe is uniquely positioned to meet that demand. By leveraging our global infrastructure, leading-edge technology, and proven experience facilitating around-the-clock trading in global markets, we believe we can seamlessly support a 24×5 trading model for U.S. equities.”

Cboe operates 27 markets across five asset classes in the U.S., Asia Pacific and Europe. Currently, it already supports extended trading hours for U.S. equities on EDGX, with early order acceptance beginning at 2:30am ET and trading available from 4:00am ET to 8:00pm ET, Monday through Friday. During its Early Hours Trading session (4:00am – 7:00am ET), average daily volumes on EDGX increased by 135% between 2022 and 2024.

Cboe also offers near 24×5 trading in its proprietary S&P 500 Index (SPX) options, and Cboe Volatility Index (VIX) options and futures markets, in addition to 24×5 trading in its global FX markets.

The proposed 24×5 trading model for U.S. equities is expected to further expand trading opportunities for investors worldwide, enabling them to react to global macroeconomic events as they are happening, manage risk more effectively, and adjust positions around the clock.

To complement the planned expansion, Cboe continues to significantly increase distribution of its U.S. equities market data for APAC and European customers, recognizing real-time pricing as an essential component of the investing and trading process.

Its Cboe One U.S. Equities Feed, available to customers globally, offers consolidated, real-time market data from Cboe’s four U.S. equities exchanges – which collectively account for 21.6% of U.S. equities on-exchange trading.

Cboe plans to make all listed NMS stocks available for trading on EDGX for 24 hours every business day (excluding U.S. holidays), subject to regulatory review, with all trades expected to be cleared through the Depository Trust and Clearing Corporation (DTCC).

The company plans to seek approval from the Securities and Exchange Commission (SEC) and will collaborate with other industry participants to ensure operational readiness for this initiative.

NEW YORK, Feb. 4, 2025 – To streamline communication between asset managers and their executing brokers, Broadridge Financial Solutions Inc. (NYSE: BR), a global Fintech leader, today announced a partnership with Symphony, the communication and markets technology company, to integrate messaging technology into the NYFIX Matching platform.

This latest innovation empowers asset managers to communicate directly with brokers via Symphony’s secure messaging platform, enabling compliance, transparency and streamlined resolution of post-trade discrepancies.

Georger Rosenberger

“By integrating Symphony’s messaging functionality, we are enabling clients to resolve post-trade inaccuracies faster and with greater ease, ultimately enhancing operational efficiency,” said Georger Rosenberger, Head of NYFIX, Broadridge Trading and Connectivity Solutions.

“This is the latest example of simplifying the client experience with innovative solutions to meet their evolving needs and help them better operate, innovate and grow.”

As the first post-trade matching tool in the industry to offer integrated messaging capabilities, NYFIX Matching addresses a critical gap in the market.

The introduction of messaging functionality responds directly to client feedback, who expressed a desire for faster and more direct communication with brokers. This functionality is now available for NYFIX customers.

“As the financial industry advances towards workflow digitization, it has become increasingly reliant on modern, secure, and interoperable collaboration tools to mitigate risks and increase efficiencies,” said Brad Levy, CEO of Symphony. “Through this collaboration, we are able to accelerate trade flows and improve real-time transactional accuracy for Broadridge’s clients.”

The financial technology (fintech) sector has experienced remarkable growth over the past two decades, with advancements in areas such as digital banking, blockchain, and, notably, trading. Trading platforms and strategies have been revolutionized by the rise of algorithmic trading, robo-advisors, and AI-driven insights, making it a rapidly evolving space. One of the most transformative elements of fintech, however, has been the increasing involvement of women in leadership roles, particularly in the trading innovation space.

Historically, the financial services industry has been male-dominated, with few women in positions of power. However, over the last few years, women have increasingly played pivotal roles in driving fintech innovation, including in areas such as high-frequency trading (HFT), asset management, and algorithmic trading. Their leadership has not only contributed to the democratization of financial markets but also introduced new ways of thinking, diversity in problem-solving, and fresh perspectives that are redefining the future of fintech and trading.

Women Pioneers in Fintech Trading Innovation

Maggie Wilderotter

Maggie Wilderotter is a trailblazer in tech and finance, with a long history of leadership roles in both sectors. As a former CEO of Frontier Communications and current board member at Citigroup, Wilderotter has influenced fintech innovation in equities trading by providing strategic oversight on how financial institutions can leverage technology to improve market access and trading efficiency. Wilderotter has been instrumental in pushing digital transformation in financial services, including equities trading. Her work at Citigroup has contributed to the firm’s efforts to create AI-driven platforms for equities trading that use machine learning to enhance decision-making, reduce costs, and improve trade execution times.

Another prominent figure is Christine Moy is the head of J.P. Morgan’s Digital Assets team, where she focuses on integrating blockchain technology into traditional financial services, including equities trading. Moy is working on creating digital infrastructure that would allow for tokenized equities and smart contracts to transform how stocks and other securities are traded. Her work with tokenized equities aims to address the long-standing inefficiencies of the equities trading process, including the settlement and clearing cycles, making equity transactions faster, cheaper, and more secure. By leveraging blockchain’s transparency and security, Moy is at the forefront of a potential paradigm shift in how equities are traded and settled on a global scale.

In addition, longtime Bank of America executive Cathy Bessant, has driven the development of AI-driven trading systems that allow for better market analysis and faster trade execution in the equities markets. By making use of big data, machine learning, and cloud computing, Bessant’s leadership has enabled Bank of America to increase trading efficiency and offer advanced equity trading solutions to institutional clients.

Mona Ataya

Women leaders in fintech are also making significant strides in the integration of artificial intelligence (AI) and data analytics into trading strategies. The application of AI in trading can analyze vast amounts of data at a speed and efficiency far beyond human capability. For example, Mona Ataya, the founder of Mumzworld and an influential figure in fintech, has made strides in integrating technology with finance, focusing on personalized experiences that tailor financial and trading tools to the needs of individual traders. Her focus on data and the personalized approach resonates in fintech’s shift toward a more client-centric model, which has been particularly beneficial for retail investors and everyday traders looking to leverage trading platforms more effectively.

Challenges and Opportunities

The involvement of women in trading and fintech innovation is not just beneficial for the growth of the industry, but also for the evolution of trading practices themselves. Research suggests that diverse teams often outperform homogeneous ones, particularly when it comes to problem-solving and creativity. Women bring unique perspectives to the fintech space that are often overlooked in traditionally male-dominated environments.

Despite the undeniable progress, women in fintech and trading still face challenges, such as navigating an industry where gender disparity remains significant. The number of women in senior positions within fintech companies is still low compared to men, and societal expectations can sometimes make it difficult for women to break through. However, the increasing visibility of successful female leaders is helping to create new opportunities for the next generation of women innovators.

The fintech sector itself has a unique opportunity to reshape the future of finance by continuing to support female leadership and fostering a more inclusive ecosystem. Many fintech firms are beginning to recognize the value of gender diversity, which can help expand the pool of talent and ideas needed to tackle complex trading problems. This shift is opening doors for women to contribute in more meaningful ways, particularly in areas like trading algorithms, risk management, and financial data analytics.

The Future of Women in Trading

Looking ahead, the future of women in fintech and trading innovation is bright. The growing focus on blockchain technology, cryptocurrency trading, and DeFi (Decentralized Finance) presents exciting opportunities for women to continue influencing and shaping the future of trading. The next frontier in fintech is likely to be one where women play a central role, guiding the industry toward new heights of efficiency, inclusivity, and innovation.

As more women take on leadership roles in fintech, we can expect to see a continued evolution in how trading is conducted, moving toward more agile, data-driven, and accessible platforms that are designed for diverse user groups. The work being done by women today is laying the foundation for a new era of financial technology where the barriers that once existed are continuously broken down, making way for more equal opportunities and outcomes.

In conclusion, the influence of women in fintech and trading innovation is undeniable, with female leaders contributing to major advancements in AI, data analytics, and inclusive trading platforms. As their role continues to grow, so too will the scope of innovation and transformation within the trading industry, promising a future where diversity and creativity are central to its success.

In 2024, the ETF industry experienced unprecedented growth, attracting over $1 trillion in inflows with a historic 746 launches. This surge propelled the total assets held in ETFs to an impressive $10+ trillion. Nasdaq listed 203 ETFs in the U.S. in 2024 and set a record with 67% growth in new listings on the exchange year-over-year, compared to a 37% increase over the same time period for total market launches.

The total number of U.S. ETFs on Nasdaq rose 28% to 768, with assets under management of $1.87T (as of December 31, 2024). There were 42 first-time ETF issuers on the Nasdaq Stock Market.

Leading off 2024 was the debut of spot crypto ETFs including Blackrock iShares Bitcoin Trust, IBIT, which listed in January 2024 and reached $50B in assets under management by the end of the year, making IBIT a record-breaking ETF launch. The ETF space is heating up in 2025, given the optimism for crypto regulatory clarity.

Out of Nasdaq’s U.S. ETF launches, 4% were focused on cryptocurrency, 9.5% applied an options or defined outcome strategy, and over three quarters were active transparent in terms of their management style. Danielle Rutsky, Lead Product Manager at Nasdaq, said in a blog: “As we see the continued growth of unique and advanced strategies utilizing the ETF wrapper, we look to mirror that innovation in issuer support.”

In 2024, the Nasdaq Stock Market continued to be the largest U.S. equity market by trading volume and the ETF business benefited from this deep equities trading liquidity pool and the world’s most robust electronic auction, the Nasdaq Closing Cross. Nasdaq’s market share of total ETF listings grew to 20% in 2024, an almost 10% increase over the previous year and the third consecutive year of market share increases for the exchange.

Rutsky said Nasdaq is always looking to better advance ETF industry support and data transparency. Nasdaq launched ETF Intel in 2023, a first-of-its-kind, customizable ETF data portal that combines individual market quality data with overall industry trends to allow for more powerful peer comparison and trading analysis. This year, Nasdaq is evaluating adding more data and visualizations to ETF Intel for premier clients and enhancing its Designated Liquidity Provider (DLP) program to continue to expand support for various types of ETFs and help increase liquidity with ETFs that have lower trading volumes.

Rutsky also remarked that approximately 50 asset managers have filed with the SEC already this year to offer share classes of ETFs and mutual funds within the same investment vehicle, and there were a record 55 mutual funds to ETF conversions in 2024. “2025 could be a pivotal year for the funds industry,” added Rutsky.

Reductions Reflected Across 168 Vanguard Mutual Fund and ETF Share Classes

Changes Represent More Than $350 Million1 in Savings for Investors

VALLEY FORGE, PA (February 3, 2025)—Vanguard today announced historic expense ratio reductions to one hundred sixty-eight mutual fund and exchange-traded share classes across eighty-seven funds. The reductions will save Vanguard’s investors more than $350 million in 2025 alone, the largest annual expense ratio reduction in Vanguard’s nearly 50-year history.

“Jack Bogle founded Vanguard in 1975 with a simple purpose—to design an investor-owned company that would serve a single constituency, our clients,” said Salim Ramji, Vanguard’s Chief Executive Officer. “At Vanguard, we’re focused on creating value for our investors, not extracting value from them. We’re proud to build on Vanguard’s legacy of lowering the costs of investing—which we have done more than 2,000 times since our founding—by announcing our largest ever set of expense ratio reductions. Lower costs enable investors to keep more of their returns, and those savings compound over time.”

In investing, you get what you don’t pay for. Costs matter.

Vanguard’s index and active products have low costs across all asset classes—equity, bond, money market, and multi-asset solutions. That track record of lower costs is directly correlated to the long-term performance of the firm’s mutual funds and ETFs–84% of Vanguard funds have outperformed their peer group averages over the past decade.2 This latest expense ratio reduction will allow clients to retain an even greater share of their long-term returns.

“Vanguard’s strength as an industry-leading active manager and index pioneer has only grown over the years, in part due to our low costs,” said Greg Davis, Vanguard President and Chief Investment Officer. “When thinking about our actively managed funds, our portfolio managers can take investment risk strategically as they don’t have to overcome the hurdle of high fees to add value.”

Crucial role for fixed income—active management at index fund fees

Vanguard Fixed Income Group is the largest manager of bond mutual funds and ETFs,3 and for more than 40 years has distinguished itself with deep investment capabilities, disciplined security selection processes, and rigorous risk management techniques, which has resulted in consistent long-term performance.

Vanguard investors have access to world-class active fixed income management—91% of Vanguard’s active bond funds and ETFs outperformed their peer group average over the past decade.4 Vanguard’s actively managed fixed income funds and ETFs have a weighted-average expense ratio of 0.10% versus the industry average of 0.53% for active funds and ETFs from other firms.5 Vanguard’s bond index funds have a weighted-average expense ratio of 0.05%, less than half the average of 0.11% from our competitors.6

“Bonds are poised to play a crucial role in investors’ portfolios going forward,” said Mr. Davis. “We expect yields to settle at levels higher than those seen over the past 15 years. This will not only provide attractive inflation-adjusted income, but also reinforce the traditional role of bonds as the ballast in investors’ portfolios.”

Expense ratio reductions across Vanguard’s fund lineup

In addition to Vanguard’s world-class lineup of bond mutual funds and ETFs, these historic expense ratio reductions will lower costs across Vanguard’s U.S. equity, international equity, and money market funds as well.

A full list of expense ratio reductions can be found here. The changes in expense ratios are effective immediately.

###

About Vanguard

Founded in 1975, Vanguard is one of the world’s leading investment management companies. The firm offers investments, advice, and retirement services to tens of millions of individual investors around the globe – directly, through workplace plans, and through financial intermediaries. Vanguard operates under a unique, investor-owned structure where Vanguard fund shareholders own the funds, which in turn own Vanguard. As such, Vanguard adheres to a simple purpose: To take a stand for all investors, to treat them fairly, and to give them the best chance for investment success. For more information, visit vanguard.com.

1 Comparison uses AUM as of 11/2024. There is no guarantee that any individual investor will save money due to the reductions in expense ratios. Figures are estimates and should not be relied on. For illustrative purposes only. See www.corporate.vanguard.com/feecuts for details.

2 Source: LSEG Lipper. Number of Vanguard funds that outperformed their Lipper peer-group averages for periods ended December 31, 2024: For the ten-year period, 265 of 317 Vanguard funds. Results will vary for other time periods. Only funds with a minimum ten-year history were included in the comparison. Note that the competitive performance data shown represent past performance, which is not a guarantee of future results, and that all investments are subject to risks. For the most recent performance, visit our website at vanguard.com/performance.

3 Source: Morningstar, assets under management for bond mutual funds and ETFs, November 30, 2024.

4 Source: LSEG Lipper. Number of Vanguard funds that outperformed their Lipper peer-group averages for periods ended December 31, 2024: For the ten-year period, 40 of 44 actively managed bond funds. Results will vary for other time periods. Only funds with a minimum ten-year history were included in the comparison. Note that the competitive performance data shown represent past performance, which is not a guarantee of future results, and that all investments are subject to risks. For the most recent performance, visit our website at vanguard.com/performance.

5 Source: Vanguard calculations using Morningstar data. Expense ratios weighted by assets as of November 30, 2024.

6 Source: Vanguard calculations using Morningstar data. Expense ratios weighted by assets as of November 30, 2024.

For more information about Vanguard funds, visit vanguard.com to obtain a prospectus or, if available, a summary prospectus. Investment objectives, risks, charges, expenses, and other important information are contained in the prospectus; read and consider it carefully before investing.

Vanguard ETF Shares are not redeemable with the issuing Fund other than in very large aggregations worth millions of dollars. Instead, investors must buy and sell Vanguard ETF Shares in the secondary market and hold those shares in a brokerage account. In doing so, the investor may incur brokerage commissions and may pay more than net asset value when buying and receive less than net asset value when selling.

All investing is subject to risk, including the possible loss of the money you invest.

Vanguard is reducing expense ratios for certain share classes of some funds. There is no guarantee that any individual investor will save money due to the reductions in fund expense ratios. Not all fund share classes will have a reduced expense ratio and therefore not all investors will experience the estimated savings. Investors that purchase the relevant funds after the expense ratios have been reduced will not experience savings. Savings means future money not spent on expense ratios, and does not entail a rebate or deposit of any sort. Savings figures are estimates and should not be relied upon. Savings is based on data as of November 30, 2024; if other data is used, savings may differ. Estimated savings accrue to existing investors holding relevant share classes for 2024 and 2025. For illustrative purposes only. Past performance is not indicative of future results.

Be aware that fluctuations in the financial markets and other factors may cause declines in the value of your account. There is no guarantee that any particular asset allocation or mix of funds will meet your investment objectives or provide you with a given level of income.

Diversification does not ensure a profit or protect against a loss.

Investments in bonds are subject to interest rate, credit, and inflation risk.

Investments in stocks or bonds issued by non-U.S. companies are subject to risks including country/regional risk and currency risk. These risks are especially high in emerging markets.

Vanguard Marketing Corporation, Distributor of the Vanguard Funds.

Trading Technologies is porting its integrated surveillance offering to asset classes beyond futures.

As regulation in the US, UK and Europe has increased in recent years, securities firms have invested more in operations, compliance and trade surveillance. And rather than just checking a regulatory box, technological advances are enabling firms to realize a return on their investment and even a competitive advantage.

Investment in operations and compliance technology is a 2025 market structure trend to watch, according to Crisil Coalition Greenwich. In a January report, the consultancy noted that firms are spending money to shore up the back office, a historically under-resourced area compared with the revenue-generating front office.

“Making money can’t happen if the foundation is weak,” the report stated. “Those that look closely at operations and compliance infrastructures understand the goal is not just cost reduction, but scale, risk reduction and enabling strategic goals. That’s why mainframes are giving way to the cloud, exception alerts to AI monitoring and margin management spreadsheets to portfolio management systems that help optimize collateral.”

Compliance and trade surveillance is a focus area for Trading Technologies, a SaaS provider to the global capital markets industry. Traders Magazine spoke with Nick Garrow, EVP Chief Revenue Officer & Head of EMEA, and Jay Biondo, Head of Surveillance, to learn more about the state of the business and the technology.

What is the background of Trading Technologies’ trade surveillance, and how does it translate to the present day?

Nick Garrow:

Nick Garrow: TT bought Neurensic in 2017. Neurensic was a pioneer in using machine learning solutions for trade surveillance. We then acquired Abel Noser in 2023, and they had a compliance offering as well. We now have a business that services more than 100 customers who use our trade surveillance tools on a day-to-day basis. We have a good customer base, spread all over the world, spanning buy side and sell side. We have a range of different customers and a proven product.

What we’re doing now is bringing together our two unique offerings in trade surveillance. We’re leveraging the machine learning capabilities of the Neurensic product with our configurable models. We’re bringing the best of both worlds in trade surveillance. We can have machine learning to identify false positives, and configurable models to build sets of models around this.

We’re one of the few providers in the marketplace who offer this combination. Our fundamental value proposition is that we will cut down the number of false positives that a compliance officer has to deal with daily. We score, highlight and show, in a clear and

intuitive way, where the biggest risk of trade abuse is for the client. What we are trying to do is greatly reduce the amount of time trade surveillance staff has to spend sorting through hundreds of false positives.

Are there commonalities between compliance / trade surveillance, and other TT businesses?

Nick: This business is similar to TT’s business in data and analytics, and also our business in quantitative solutions and algorithms, in that in each business it’s about ingesting data, running it through a machine, and generating an output. The data and analytics output is transaction cost analysis; the output in quant solutions and algos is great optimization; the output in this area is a trade surveillance solution.

So there’s a theme that runs across these three lines of business. They’re all really built on data, data aggregation, and data smarts.

What are themes for 2025?

Nick: We have a roadmap laid out for this year. We’re promoting one single product to the marketplace, TT Trade Surveillance, which is basically a one-stop shop for multi-asset trade surveillance. We’re bringing that to market now – we’ve had a lot of good feedback and good engagement with some big tech customers, which we’ve been onboarding.

A major market theme out there today is cross-product, cross-market risk proofing and abuse detection. Of course regulators look at what you do on one exchange or with one product, but they’re also looking at what you do as you trade multiple products across multiple trading venues. Another theme is regulators looking at what you do on regulated markets in conjunction with your activity in OTC markets.

Tied in with those is the theme around voice communications, or v-comms and e-comms trade surveillance. It’s great for a firm to surveil and ingest trades, but regulators also want to see a control framework that shows you have all your voice communications and e-communications, your Slack, your email, everything else – all coming into the same data center. And then you have to be able to stitch all this data together and make sure that you understand and explain your trading operations, globally. It’s a lot.

What’s the competitive landscape in trade surveillance?

Nick: Right now in the marketplace there are a few big global players – NICE Actimize, Nasdaq Smarts, and FIS. And then you have the mid-range providers which we compete with, like Scila. After that you have a pile of new entrants, regtech and fintech startups who offer what looks like good technology at a very low price. But we’ve heard from many customers that these offerings are more like tick-the-box trade surveillance, and if you go beneath the surface, they don’t stand up to scrutiny.

Jay, what is your professional background?

Jay Biondo

Jay Biondo: I joined TT with Neurensic. Prior to that, I was a chief compliance officer at some proprietary trading firms here in Chicago, including Alston Trading; before that, I was a regulator for a few years at NYSE Arca and FINRA.

I joined Neurensic because of the very innovative concept of applying machine learning to trade surveillance. Fast forward to today, and I think the critical piece is that we have fully integrated what we had designed at that startup company, onto the TT platform.

How is TT expanding its surveillance offering?

Jay: We have focused primarily on futures, taking what we built at a startup like these machine learning models which looked for patterns and spoofing in futures data. We have had a lot of success with that.

But what we have found is that people don’t want to just monitor spoofing in futures. They want to look at all types of manipulation, like for example marking the close, or influencing the open, or front running, and they want to look beyond futures – they want to see equities, equity options, fixed income, and FX. So what we’ve done over the past seven years is build out our model suite where we have out-of-the-box and configurable models that we can also apply to other asset classes.

Last June we announced that we were expanding our trade surveillance into equities, equity options, fixed income and FX. A lot of people in the industry still associate us with futures, which is understandable as futures has been our core business for a long time. But right now we’re making a big push outside futures and into other asset classes, and it’s been very well received by the industry.

Janney Montgomery Scott, a full-service wealth management and investment banking firm, has appointed Tony Miller as Chief Executive Officer. Miller will also continue in his current role as President, a position he has held since 2023. Miller joined Janney in 2002 and has held progressive leadership roles, including Director of Internal Audit, Treasurer, Chief Financial Officer, and Chief Administrative Officer, where he led the operations, technology, finance, and corporate services divisions. In addition, the firm has also announced that Tim Scheve has joined Janney’s Board of Managers as an Independent Board Director. Scheve, who served as Janney’s President & CEO from 2007 to 2023, brings decades of leadership experience and a deep understanding of the firm and the financial services industry. Scheve is a seasoned independent board director and Senior Advisor at Accenture.

Quentin Limouzi

Broadridge Financial Solutions has added to its global leadership through the appointment of Quentin Limouzi in a new role as Global Head of Post-Trade at Broadridge. With over two decades of leadership experience in the front office space and across enterprise transformation programs, Limouzi will be instrumental in supporting Broadridge’s clients to navigate global regulatory mandates and extract the greatest value from new technologies to optimize their operations. Prior to joining Broadridge, he held leadership and senior executive roles with LSEG (London Stock Exchange Group), TS Imagine (formerly TradingScreen), HSBC and BNP Paribas. In addition, the firm has announced that Stephen Wilkes has joined as Senior Vice President, Head of International Buy-Side Sales. Wilkes brings a wealth of experience and deep domain knowledge to Broadridge, with a proven track record of success in the financial services industry with previous senior roles at Deutsche Bank, J.P. Morgan and Goldman Sachs.

Jon Weiss

Jon Weiss, Co-CEO of Corporate & Investment Banking (CIB), has informed Wells Fargo & Company of his intention to retire. Weiss, who has been with Wells Fargo for nearly 20 years, will step down as Co-CEO effective immediately and will formally retire on June 1, 2025. Weiss started his career with Wells Fargo in 2005 in Investment Banking. In 2008, he became Co-Head of the Investment Banking & Capital Markets division and in 2014 he became President and Head of Wells Fargo Securities. In 2017, he was named Head of Wealth & Investment Management, a position he held until February 2020 when he was named CEO of Corporate & Investment Banking. Fernando Rivas, who joined Wells Fargo in May 2024 as Co-CEO of CIB, will become CIB’s sole CEO.

The Bank of New York Mellon Corporation has appointed Carolyn Weinberg as its Chief Solutions Innovation Officer. She will also be a member of the BNY Executive Committee. Weinberg joins BNY from BlackRock, where she most recently served as Chief Product Innovation Officer and led product innovation, development and commercialization globally for the firm. Earlier in her career, she led Markets businesses at Citibank and Deutsche Bank, where she developed client solutions across risk management, structured financing and fixed income derivatives.

Chris Contrino has joined Sterling Trading Tech, a global provider of technology in order management, risk & margin, and trading platforms, as sales director. Contrino brings a breadth and depth of client service and business development capability to the role shaped by key positions at leading financial technology firms. Most recently he served as Customer Service Manager at Trading Technologies and previously contributed to client and business solutions at Eventus and Fidessa, specializing in derivatives.

Temenos has appointed Sairam Rangachari as Chief Product Officer. With over 20 years of experience, Rangachari’s leadership in developing transformative products has helped organizations elevate customer experience, improve operational efficiency and accelerate growth. As Managing Director at JPMorgan, he led the bank’s digital channels platform and open banking strategy.

Apex Group has appointed Don Yeisley as Global Head of Transformation. He will lead the delivery and improvement team – focusing on client-driven technology and business process initiatives and improvements. Before joining Apex Group, Don Yeisley spent 30 plus years in the financial services industry, having the privilege of assisting leading firms, such as UBS, HSBC and Bank Leumi, design and execute transformational roadmaps.

The Bank of America Corporation Board of Directors has appointed Maria Martinez as a director. She was a senior executive at Cisco Systems, a global leader in networking and cybersecurity solutions, from 2018 to 2024. She most recently served as the Chief Operating Officer with oversight of Cisco’s Worldwide Operations, Customer Experience, Security & Trust, Supply Chain, and other functions.

If you have a new job or promotion to report, let me know at alyudvig@marketsmedia.com

Adena Friedman, chair and chief executive of Nasdaq, said the group’s Index business had an”exceptional” year in 2024, which helped the Capital Access division reach record full-year revenues.

Nasdaq reported that total net revenues for 2024 were $4.6bn, an increase of 19% over 2023, or 9% on an adjusted basis. Friedman said on the full-year results call on 29 January that 2024 was a “transformative” year for Nasdaq. Capital Access platforms generated 10% revenue growth in 2024, driven by the performance of the Index segment.

Adena Friedman, Nasdaq

Friedman said: “2024 was also an exceptional year for our Index franchise, which delivered 31% revenue growth, ending the year with record assets under management.”

The Index business had $80bn of net inflows in 2024, including $28bn in the fourth quarter. As a result, the business reached its fifth consecutive record quarter for assets under management of exchange-traded products that track Nasdaq indices at $647bn at the end of 2024, which was almost $200bn higher year-over-year.

In 2024 the Index business also launched a record 116 new products. More than half of the new launches were international, 27 were in the institutional insurance annuity segment and 30 were launched in partnership with new index clients.

Friedman said there are potential growth areas in digital assets, options, products and proprietary index options benchmarked to cryptocurrency indexes.

“We expect additional opportunities to arise as new regulatory frameworks provide clearer guidance, and Nasdaq will continue to strategically assess and pursue them in this dynamic space,” she added.

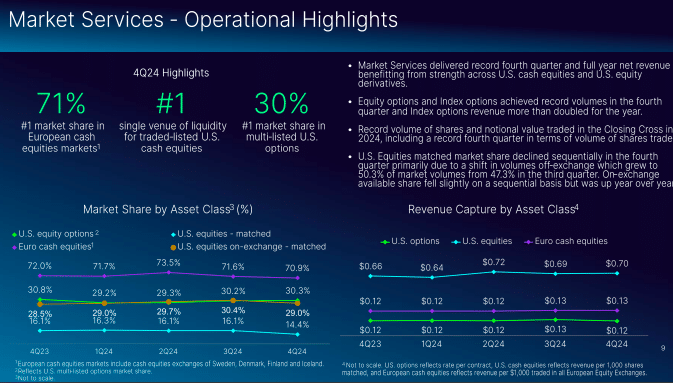

Market Services

The growth in the Index business helped boost adoption of index options and multi-listed options products, as index options revenue more than doubled year over year. Market Services achieved record fourth quarter and full-year net revenue which Friedman said was driven by higher volumes across US equity derivatives, as well as US and European cash equities.

Friedman said Nasdaq is “very focused” on growing the index options franchise by understanding new ways to build new products, bring more capabilities to clients and grow the ecosystem with both institutional and retail investors. Nasdaq’s proprietary index products are available on retail investing platforms, such as RobinHood. Institutional adoption has increased as products are integrated into different data tools

“As our index business goes more into the institutional audience, such as insurance, this drives demand for options trading and hedging capabilities,” she added. “A virtuous cycle is developing.”

Source: Nasdaq

Friedman said Market Services also benefited from momentum in US cash equities, including the Closing Cross setting full year records in both share volume and notional value traded.

In September last year Nasdaq migrated its International Securities Exchange (ISE) to Fusion, its next-generation derivatives platform, which now hosts four out of six of its US options markets and one European equity derivatives market. This year Nasdaq agreed to sell its Nordic power futures business to Euronext, the pan-European capital market infrastructure.

“This transaction will sharpen our focus on our strategic growth areas,” said Friedman. “Moving forward, our European business is an integral part of our strategy as the combination of our US and European footprint is critical to our ability to serve clients globally.”

Financial Technology

The fourth quarter of 2024 marked the one-year anniversary of the completion of acquisitions of Axiom SL and Calypso.

“With the integration of AxiomSL and Calypso largely complete, we’ve made substantial progress as a scalable platform company,” Friedman added.

In November 2023, Nasdaq acquired Adenza from private equity firm Thoma Bravo for $10.5 bn. Adenza consisted of Calypso, which provides capital markets participants with end-to-end treasury, risk, and collateral management workflows, and AxiomSL, which provides regulatory and compliance software.

Friedman said the Financial Technology division emerged as a “vital force” of innovation as more than 3,800 clients see Nasdaq as a partner in helping to solve their most critical challenges across risk, regulation and trade infrastructure,

“The financial system is at a point where transformation is technologically and culturally possible, with greater confidence in the banking and capital markets industry to implement cloud-based solutions,” she added.

The level of comfort among global banks to deploy cloud-based solutions has increased from 57% five years ago to 93% today, according to a recent report from Nasdaq and BCG. In addition, only 22% of banks prefer building in-house solutions for their regulatory and compliance programs.

Cloud bookings as a percent of AxiomSL and Calypso’s combined new annual contract value was 52% for 2024 and 60% in the fourth quarter, increasing the combined business’ cloud mix of ARR to 27% at year end. ARR is the current annualized value of subscription contracts.

“The large majority of banks understand that external solutions provide superior capabilities to solve common industry problems, and they are seeking strategic technology partners who provide solutions across multiple disciplines,” said Friedman.

Source: Nasdaq

In 2024 Financial Technology signed 263 new clients, achieved 424 upsells and has already completed 11 cross sells in 2025. Friedman said these represent Nasdaq’s continued penetration across global financial institutions and the cross highlight success in Tier 1 and Tier 2 banks.

Financial Technology also continued its international expansion with several strategic enterprise deals. For example, AxiomSL secured an upsell with Société Générale to manage the French bank’s domestic regulatory reporting needs. Capital markets technology expanded in markets including Latin America, and Friedman said notable wins included Brazil, Mexico and Colombia.

The technology business also signed three new crypto clients in the fourth quarter.

“As we look ahead, our digital asset strategy continues to focus on helping the industry mature through infrastructure that enhances market liquidity, transparency and integrity through the integration of the asset class within financial institutions,” said Friedman. “This is evident from the industry’s adoption of our market technology, surveillance and Calypso solutions.”

The Trump administration may loosen regulations for the US banking sector but Friedman highlighted that 69% of the revenues of Calypso and AxiomSL combined comes from non-US banks. She argued that if banks have more capital that they can deploy in global markets, that also drives demand for our Nasdaq technology.

“If banks are in growth mode, they will be going into new asset classes and geographies, and that drives demand for our solutions,” she said. “We have a lot of opportunities for growth across the franchise in different regulatory environments.”

Artificial intelligence

Nasdaq is incorporating new AI-powered solutions and product offerings across each of its departments. Friedman said Nasdaq shifted in 2024 from exploration and experimentation with AI to driving impact.

“Entering 2025 our team is engaged in scaling our use of AI to deliver efficiencies and productivity enhancements across the organization, which is also reflected in the expanded efficiency program,” Friedman added.

Friedman was asked about the impact of DeepSeek, a Chinese open source AI platform, that was recently released and led to a $1 trillion fall in the share prices of US technology companies.

She replied that Nasdaq uses multiple cloud providers so that the firm can use both proprietary and open source models. When Nasdaq thinks about a new capability or product, it will test different models to see which one provides the best solutions, and then which has the most efficient cost structure.

“The cost of generative AI has already come down a lot and has been quite dramatic,” she added. “We are really embedding gen AI capabilities into our product roadmaps.”

For example, Nasdaq’s Verafin business has deployed a gen AI co- pilot the anti-financial crime business, and Friedman said that will be implemented in the surveillance business.

The Canadian Investment Regulatory Organization (CIRO) has published its Annual Compliance Report, providing insight for dealers into emerging compliance challenges and what’s needed to address them.

CIRO’s Annual Compliance Report helps dealers focus their supervision and risk-management efforts to comply with CIRO’s regulatory requirements effectively.

Andrew Kriegler

“The Compliance Report serves to communicate emerging issues to all dealers for awareness, preparedness, and to take the best approach to adjusting policies and procedures,” said Andrew Kriegler, CEO, CIRO.

“By alerting dealers to potential issues faced by their industry peers, CIRO advises all members about risks and emerging compliance matters, to strengthen investor protection while responding to changes in the industry.”

A key theme of the report is the relationship between technologies used in the investment ecosystem and managing their risks to protect investors. Highlights include:

Cybersecurity remains a key business risk irrespective of the size and complexity of the dealer member. Dealers are required to report cybersecurity incidents that meet certain criteria and to implement necessary controls to protect their clients. The report warns of an increase in incident reports involving third-party service providers that have impacted their clients. The report encourages dealers to review whether they have the necessary controls in place to protect clients, client information and assets, as well as their own critical operating systems, and in training personnel to fortify their cybersecurity.

Crypto Asset Trading Platforms (CTPs) continue to be onboarded into CIRO membership. Compliance takes a top-down, risk-based approach to recognizing the higher inherent risk associated with CTPs. As CIRO and the CSA continue to evolve and adapt to the changing crypto ecosystem, members planning to offer crypto-assets to clients should stay informed about regulatory developments.

Algorithmic Trading is a significant tool in today’s capital markets. Implementing robust controls to validate data inputs and operations is essential to ensuring the accuracy and reliability of trading decisions—and maintaining the integrity of the capital markets. The report recommends regular reviews of algorithms to ensure their ongoing effectiveness.

Social media is increasingly used as a marketing and educational tool in the finance industry. Dealers are required to establish and maintain policies and procedures on the use of social media for business purposes by their Approved Persons. The report encourages dealers to establish clear guidelines for interacting with clients and to maintain proper books and records of communications in compliance with regulatory obligations.

Integration is a key pillar of the first year of CIRO’s inaugural Strategic Plan and annual public priorities for 2025—delivering efficiencies for the organization, members and the industry as a whole. The internal structure of CIRO’s compliance teams is now integrated and the compliance programs have been harmonized to support the organizational goal of delivering regulation effectively and efficiently.

“This report will help dealers with their own compliance policies and procedures so that collectively, as an industry, we can improve investor confidence and strengthen Canadian markets,” said Kriegler.

{kind=link}

{kind=link}

Low Intensity Competition for Prosperity of Overall Markets

By Kelvin To, Founder And President Of Data Boiler Technologies

Market data reform was originally a raised concern for fairness of access and cost burden for market participants. The Financial Conduct Authority (FCA) said the Consolidated Tape (CT) for UK equities would not happen until 2028 is in effect a diplomatic move without saying the obvious. The European Securities and Markets Authority (ESMA) MiFIR Review Final Report contains FATAL FLAWS that will lead the European equities markets to a death spiral. Switzerland is NOT a part of the EU. It may sit on the fence and observe if other National Competent Authorities (NCAs) REJECT this faulted ‘Regulatory Technical Standards’ (RTS) at the European Commission (EC) level. Meanwhile, the US Market Data Infrastructure Rule (MDIR) is set to be implemented in November 2025 with odd-lot information to be included by May 2026. The following pinpoints the key flaws and how to turn it around positively for the best interest of investment firms and the overall markets.

Flaw #1: Timing Mismatch of European Best Bid & Offer (EBBO) and the Most Relevant Market in terms of Liquidity (MRMTL)

ESMA opted for anonymity of trading venue with the best price, yet they ask the CT provider to show the MRMTL that is calculated annually per Article 4 of Commission Delegated Regulation 2017/587, alongside the real-time EBBO. The public will be misled! It is a deliberate act to direct order flow to the larger exchanges, when the smaller / remote exchanges or multilateral trading facilities may have the best price and sufficient quantities to fill orders. Not only is it counter-productive to the CMU or the new ‘Savings and Investment Union’ (SIU) objective, with its intent to “attract institutional investor participation, better connect savers and borrowers irrespective of their geographical location, and ensure that ordinary savers can benefit from the wealth creation of the corporate sector”, Europe is digging its own grave – money would flee when markets can no longer be trusted!

Flaw #2: One single currency to represent both the best bid and the best offer in Europe

Following Flaw #1, where larger exchanges have dominated turnover volume, especially during close and/or open. It is likely that smaller or remote trading venues will rarely be reported on the MRMTL because of the bias. The next distortion is which currency to show for EBBO. Securities in Europe can be denominated in various currencies other than Euro. The best bid could be in Swedish Krona, while the best offer in Sterling Pound, or vice versa or a mix of different currencies. Pairing the best bid and the best offer is indeed concentrating volume at the larger exchanges. It reduces the serendipity of cross-market trading opportunities. Rail ticketing in Europe accepts different currencies. It is one of its conveniences, how can the EU equities CT not to have real-time multi-currencies capabilities?!

Flaw #3: Tolerating latency timeliness standards and leaving loopholes for ecosystem degradations

It is totally practical for CT to mimic how High Frequency Trading firms (HFTs) aggregate ultra-low latency data across venues. Yet, ESMA relaxes the “as close to real time as technically possible” clause to allow Exchanges and Approved Publication Arrangements (APAs) transmit data to the CT Providers within 50 milliseconds with a 95% confidence interval from the timestamp of the order submission for pre-trade data. The Europe CT’s benchmark should be at least better than the US SIP realized latency in tens of microseconds, amid those that subscribe to PPs are receiving more detailed data in nanoseconds or microseconds at most. One of the US Consolidated Audit Trail fatal flaws is its 50± milliseconds tolerance. Hundreds-of-thousands trade messages at any given point in time is not suitable for analytics. Although ESMA preserved the timestamp granularity for trading venues with a gateway-to-gateway latency below 1 millisecond to be set at 0.1 microseconds, the amendment to Regulation (EU) No 648/2012, and Article 22c grants a Maximum Divergence from UTC of 100 microseconds is a loophole. There is no obligation for Exchanges or APAs to report “clock drift averages and peaks and number of instances of clock drift greater than 100 microseconds”.

The ESMA’s expectation of “data contributors send the data to the CT Provider as soon as possible and without artificial delays compared to sending of data for other purposes, including proprietary feeds, to meet such requirements” is substantially weaker than the US Securities and Exchange Commission (SEC) Rule 603(a) that “prohibits an SRO from making NMS information available to any person on a more timely basis.” The SEC recognizes the Securities Information Processors (SIPs) were not modernized alongside markets evolution and technologies development; therefore, it requires the “same manner same methods” provision (see page 186 or footnotes 608 and 609 of MDIR). Yet, we argue that the US SEC MDIR does not go far enough because Co-location ≠ Latency equalization ≠ Market data available Securely in Synchronized Time.

Shared versus dedicated switch, temperature, network time rather than precision time protocol, etc. can affect performance and influence the EBBO spread. What you see may not be what you get. One will need to upgrade to higher bandwidths and add depth-of-book data, or else face being disadvantaged to proprietary feed subscribers. Trading venues’ products differences are often determining success or failure in a few nanoseconds and/or altering bandwidth for blocks. Losing a few basis points per trade could accumulate to hundreds of millions if not a billion.

Flaw #4: Crappy clauses such as ‘authentication, authorization, and non-repudiation’ is within the RTS requirement