Frank La Salla, President, CEO, and Director of DTCC

While the macroeconomic and geopolitical environment will remain uncertain in 2025, I’m optimistic about our industry’s future and the opportunity for DTCC to lead on critical initiatives that mitigate risk, enhance resilience and strengthen market structure. In that sense, this year will largely be a continuation of 2024 in that we must continue to execute flawlessly on large-scale industry implementations. On the heels of the smooth T+1 conversion, we will galvanize the industry and provide strong leadership on the transition to the SEC’s U.S. Treasury Clearing rule.

In addition, innovation will be an area of sharp focus for our firm. We’ve already been integrating digitization, cloud and AI into our capabilities, and we’ll continue to advance this important work in the coming years. However, we also recognize that not all innovation will be underpinned by technology, which means that we’ll also focus on opportunities to improve market safety and efficiency through process enhancements, cross-margining agreements and other creative approaches.

Technologies such as blockchain and the cloud will play a crucial role in the build out and interconnectedness of the digital financial ecosystem. DTCC will continue to serve as a strategic partner to the industry by advancing acceptance and adoption of digital assets, focusing on opportunities to tokenize collateral and funds, and leveraging our existing clearing and settlement capabilities to facilitate the listing of digital funds on exchanges as well as secondary trading. We’ll also continue to advance our use of AI where it will be strategically beneficial to the client experience.

We continue to focus on upgrading and modernizing our technology to provide clients and the industry with innovative services and capabilities they need today and in the future. In 2025, one of our top priorities will be readying our IT platforms and client-facing applications to support US Treasury Clearing, which represents one of the most significant changes to market structure in decades. In addition, given the evolving threat landscape, we’re committed to strengthening our resiliency and partnering with our clients and technology providers to ensure financial markets continue to operate seamlessly.

We’re also investing in AI and exploring how it can improve the client experience as well as to enhance our own productivity and efficiency. As AI continues to mature, it becomes essential to upskill employees with a foundational knowledge of AI to drive innovation and pursue practical and responsible use cases.

Nadine Chakar, Managing Director, Global Head of DTCC Digital Assets

2024 was a pivotal year for digital assets, and we’re seeing strong momentum toward adoption. More and more institutional investors – on both the buy- and sell-side – continue to be getting engaged with this technology. We also saw a lot of progress on the regulatory front, with the SEC’s approval of Ethereum and Bitcoin ETFs in the US in 2024, and the first stages of the EU’s MiCA, the first-ever blockchain-related asset regulation, coming into effect.

We still have our work cut out for us in 2025 and beyond. While we’ve clearly proven the merits of this technology, it’s time to put real applications on the ledger using tokenization. As we move beyond pilots and start putting projects into production, we’ll need to make sure we’re collectively driving toward an end goal: building an efficient digital market infrastructure and standards. Collaboration is the core ingredient that will help us capture the promise that digital assets hold.

DTCC is excited to be at the forefront, leading the charge for industry acceptance and greater adoption of tokenization solutions. We are proud to have further advanced this work with the launch of DTCC Digital Launchpad, an industry sandbox that’s bringing together financial market participants and clearing the path to scalable adoption of digital assets. In 2025, we will continue to focus on establishing the digital market infrastructure of the future, showcasing how we can deliver the same efficiencies for digital assets as we do in traditional markets today, while also ensuring smooth market operation, transparency and liquidity.

# # #

Timothy Cuddihy, Managing Director and Group Chief Risk Officer at DTCC

As the threat landscape evolves and the nature of risk takes on new forms in the coming year, DTCC will continue to focus on strong risk management practices and robust operational resilience. Effective risk management is imperative given the heightened geopolitical risks, macro-economic uncertainty, cyber threats, and pace of technology change. Given DTCC’s role in mitigating risk, we are always focused on assessing and protecting against multiple and interconnected risks to the global financial system.

To ensure defense against ever-evolving risks,firms must embrace a holistic approach to risk management, combining real-time threat detection, advanced automation, and collaboration across the financial ecosystem. The key to navigating this environment lies in building and implementing adaptable, forward-looking frameworks that not only address today’s risks but forward-looking risk assessments to prepare for dynamic challenges ahead.

# # #

Brian Steele, Managing Director, President, Clearing & Securities Services at DTCC

The expansion of U.S. Treasury clearing is a huge priority for us in 2025. With deadlines fast approaching, DTCC is fully committed to a successful implementation, and we are working closely with the industry to educate clients on the impacts and preparations needed to ensure a smooth transition and to deliver upon the transparency and risk management benefits of such a move. Driving capital and liquidity efficiencies for the industry is a keen focus area for DTCC, which is why we are doubling down to improve our solutions (i.e. cross margining arrangements, creation of default fund, etc.) and enable our clients to maximize capital while complying with mandates such as Basel III rules, etc.

At the same time, we stand ready to assist the industry as global accelerated settlement efforts progress in EU and UK. We will continue to engage our clients through various forums as we look to expand and develop new products and services such as cleared securities lending, optimizing the use of Collateral, increase the usability and access of our data, and improve our clients’ experience by modernizing platforms and increasing resiliency. We are also actively preparing to support our clients through regulatory change efforts impacting RDS (i.e. Canada, JFSA Phase III and HKMA rewrite) and continue to invest in risk management excellence to protect the industry.

# # #

Michele Hillery, Managing Director, Head of Repository & Derivatives Services

2024 was a significant year in which the derivatives markets were shaped by substantial regulatory reporting updates. Global refits across North America, UK, EU, Singapore, Japan and Australia delivered enhanced transparency and greater efficiency across global capital markets, as firms tackled legacy trades and aligned reporting across jurisdictions, with swift action and robust data strategies proving crucial to implementation success.

The pace of regulatory change shows no sign of slowing in 2025, with global jurisdictions including Canada, Japan and Hong Kong preparing to go live with the UPI reporting as part of the derivatives trade reporting rules.

To ensure preparedness, firms should continue to build on lessons learned from past implementations. Early preparation and collaboration, continuous adaptation, and strong industry partnerships will all be critical to ensuring compliance and strengthening post-trade infrastructure and reporting as the industry continues to evolve.

# # #

Laura Klimpel, Managing Director and Head of DTCC’s Fixed Income and Financing Solutions

2024 has been a pivotal year in industry preparations for the expanded UST clearing as a result of the SEC mandate, resulting in a significant and continued growth in fixed income clearing volumes. Throughout the year, FICC remained focused on providing the most efficient and resilient clearing services for the industry. On September 30, FICC’s Government Securities Division saw record daily volumes of over $10 Trillion and its Sponsored Service alone reached peak daily volumes over USD$1.7 trillion, creating USD$846 billion in balance sheet savings across the industry. FICC is built for scale, and the record-breaking clearing volumes seen over the course of the past year are testament to its ability to meet the growing demand.

To help the industry prepare for the 2025 and 2026 regulatory deadlines, FICC has made significant strides in advancing how we will support done-away clearing in the Treasury market. Both of our indirect access models, the Sponsored Service and the Agent Clearing Service which was recently approved by the SEC, support done-away activity. We are also addressing remaining challenges around accounting implications – with resolution anticipated imminently – and will continue to roll out innovative products and services that create new margin and capital efficiencies for our clients. Looking ahead, we will continue to listen and respond to the needs of the industry to ensure that firms are well prepared for the Treasury clearing mandate and ensure a seamless implementation.

# # #

Tim Lind, Managing Director of DTCC Data Services

2024 was a year of transformation for asset servicing, driven by data-centric approaches that leverage new data sources to enable greater integrity and insight into valuation, risk management and liquidity dynamics. AI and cloud-based data marketplaces will accelerate transformation of the data supply chain by replacing point-to-point connectivity between institutions with collaborative alternatives that focus on sharing, rather than sending data.

As a leading market infrastructure provider and trusted partner to American issuers, we are poised to lead this change. DTCC will harness its data assets and innovative technologies in service to the capital markets industry, and bring issuers, intermediaries and investors closer together than previously imagined.

# # #

Val Wotton, Managing Director and General Manager of DTCC Institutional Trade Processing

2024 marked the successful implementation of T+1 in the US, which delivered substantial risk mitigation and operational and cost efficiency benefits to market participants. Under the new timeline, over 95% of transactions are meeting the affirmation criteria, a notable improvement from the 73% affirmation rate under T+2. Market participants have also benefitted from the significant reduction in margin requirements, allowing them to make better use of their capital and resources, while simultaneously reinforcing financial stability. Global accelerated settlement cycles will continue to be the key theme for market participants in 2025, with attention shifting to implementation in the UK and Europe. DTCC wholly supports the recently published UK’s Accelerated Settlement Taskforce Recommendations which focus on post-trade automation as a T+1 enabler, and ESMA’s recently issued Final Report, which calls for automation and harmonization across the EU region in order to make the move to a T+1 settlement cycle. We recommend that market participants approach T+1 implementation in the UK and Europe as an opportunity to evaluate holistically at their middle and back-office functions and assess how they can increase operational efficiency through automation and standardization through central matching solutions that enable same day confirmation.

Imperative Execution, a financial technology company and the operator of the IntelligentCross alternative trading system, hired Keith Fortier to the newly created position of Managing Director of Operations.

Keith Fortier

Fortier joins Imperative Execution from BMO Commercial Bank, where he was Head of Broker Dealer Client Services and TechOps Global Trading Solutions. Previously he held technology and client service roles at Clearpool Group, Dimension Capital Partners, and SunGard Financial Systems (now FIS).

“I’m excited to join IntelligentCross at this exciting stage of their journey,” Fortier told Traders Magazine. “Since their launch, I’ve had the opportunity to collaborate with this talented team as a routing partner. Today, I am honored to take the next step and be part of their growth, working from the other side of the partnership to support and empower subscribers, just as I once was.”

The hire follows Imperative Execution hiring Greg Ludvik as Global Head of Product & Strategy, also a new role, in November.

2024 was a major year of change for displayed trading on IEX as a result of added functionality and enhancements to core offerings like our Signal. We are very proud of our market share growth in displayed trading, which has increased approximately 3x since June, allowing us to become one of the top exchanges for displayed liquidity as measured by our time and size at the inside in both the S&P 500 and Russell 3000. We also saw growth in non-displayed trading as demonstrated by the fact that we currently have the largest notional midpoint market share in single stocks compared to all other exchanges. Last, but certainly not least, our plan to launch a U.S. Options Exchange is one of our top highlights of 2024.

What are your expectations for 2025?

IEX spent the last decade innovating by building technology designed to protect market participants from adverse selection while maximizing best execution. We expect to continue to leverage our expertise in building equities exchange technology and our obsession with market quality to drive our growth. Conversations over the past year underscored that the successful features of our equities exchange—proprietary solutions to help resting orders and order performance optimization—will be key differentiators in how we protect clients from adverse selection as they navigate the challenges of a rapidly growing U.S. Options landscape.

What trends are getting underway that people may not know about but will be important?

While IEX’s recent growth in displayed trading was a highlight in 2024, we think the growth in non-displayed trading for exchanges is a trend to watch. For example, IEX expanded its exchange midpoint intraday market share in single stocks by 20% from earlier this year. One of our most recent blog posts highlights how IEX continues to deliver high-quality liquidity, combining growth with better execution outcomes.

While some traders may think of ATS and similar dark venues as the primary source of midpoint block trades, conducting these trades on exchanges presents a unique opportunity. ATS trades are not “attributable” to the tape following an execution, meaning traders don’t know which ATS or other off-exchange venue a block trade occurred on unless they were a party to the trade. Conversely trades on exchanges like IEX are attributable to the tape, allowing traders to use “heat maps” to direct flow towards a lit venue. Traders who prefer the insights from this more fulsome public data will gravitate towards venues that provide quality midpoint and block trading.

What are your customer’s pain points and how have they changed from 1 year ago?

We have always believed in our product and the quality of our market. However, our customers gave us great feedback that enhancing our fees and economics for displayed liquidity could create a powerful combination of product, performance, and economics. That led to our introduction of tiers for enhanced rebates, which propelled our growth through the second half of this year. This was led by the success of D-Limit, with $4.8T of notional value traded to date. This growth was achieved without sacrificing the market quality that we are known for.

As for options, the asset class remains one of the fastest growing in the world. Options trading volume (ADV) increased by 145% from 2019 to 2024, and by 8% from 2023 to 2024 alone. While this rapid expansion is encouraging, it is not without its challenges—particularly for market makers dealing with the risk management challenges that come with this proliferation of data. We heard from market participants that adverse selection and “pick off” risk impact market quality and the quotes on screen for investors. This feedback drove IEX’s multi-asset class expansion. We look forward to collaborating with the Options industry to deliver tools and solutions that meet their needs and help with their challenges.

Joseph (Joe) Saluzzi is partner, co-founder and co-head of equity trading of Themis Trading.

Joseph (Joe) Saluzzi

What trends are getting underway that people may not know about but will be important?

There has been a significant shift in US equity market volume this year from on-exchange trading to off-exchange trading. In recent years, trading on-exchanges accounted for approximately 55% of volume. This year, that number has consistently been below 50%. In other words, more volume is now trading off-exchange than on-exchange. We believe this shift has been the result of two factors: 1) increased segmentation of ATS orders primarily due to the use of private rooms and trajectory crosses and 2) increased volume in sub-dollar stocks. Investors need to be aware of this shift in market venues as it increases the amount of inaccessible liquidity and could harm the price discovery process.

What surprised you in 2024?

We were surprised by the number of potential new stock exchanges. This year, the 24X National Exchange had its application approved by the SEC and the Green Impact Exchange filed an exchange application. Additionally, there are two more exchanges which might soon seek approval, the Texas Stock Exchange and the Dream Exchange. If all these exchanges receive approval, then the US would be the home to 20 stock exchanges. The US stock market is already extremely fragmented with liquidity being scattered across dozens of on and off-exchange venues. Before adding any new exchanges, regulators should be thinking about consolidating some of the exchanges with de minimis market share to help aggregate liquidity.

What are your expectations for 2025?

We expect that many of the SEC’s pending proposals will not make it to a vote and end up getting withdrawn. We also expect that the Supreme Court’s decision in the Loper Bright case which ended the “Chevron deference” will open the door to more lawsuits brought by market makers, stock exchanges and trade groups against the SEC. One of their main litigation targets has been the Consolidated Audit Trail and we expect that this critical regulatory surveillance tool will continue to be challenged by the industry and their Washington DC friends.

Jim Kaye is Executive Director at the FIX Trading Community.

Jim Kaye

What was the highlight of 2024?

The T+1 settlement cycle change across the US, Canada, and Mexico was undoubtedly a highlight. Despite some concerns leading up to the transition, it went remarkably smoothly, with no significant ongoing issues reported. At our October conference, we posed the question, “How was this achieved?” Two clear answers emerged: early, coordinated action by industry participants and market infrastructure providers, and a strong, consistent approach from regulators, particularly in fixing the implementation date. While this might sound intuitive, even obvious, it doesn’t always work out this way. This achievement demonstrates what can be accomplished with the right focus and direction.

What trends are emerging that may become significant?

For the past couple of years, we’ve been collaborating with the Organization for the Advancement of Structured Information Standards (OASIS) on messaging standards for trading power and energy. By applying financial trading concepts to this sector, we aim to simplify and open up these markets, which could significantly improve energy usage efficiency.

The next frontier is green energy, including carbon emissions and related products. We’re beginning to work with firms, associations, and standards bodies to develop standards for primary issuance and secondary trading in this area. There’s a growing belief that this market has the potential to become both a major investable asset class and a crucial facilitator of the green transition.

What are your expectations for 2025?

There are two key areas our members continue to emphasize that feel poised for significant developments in 2025. One is the tokenization of securities, which has been in the prototype and pilot stages for some time. Members believe 2025 could mark its transition into the mainstream. The other is artificial intelligence, which, despite the surrounding hype, is steadily being adopted across the industry. Rather than focusing on robo-traders, the real impact lies in addressing process inefficiencies and helping people perform better. Improving data quality and implementing responsible adoption practices – such as controls and training – are critical focus areas, both to prevent accidents and to maximise the benefits of these technologies.

As technology developments create new opportunities finance professionals to push the boundaries of what’s possible in asset management, strategically applying new technologies and processes is critical to success. The insights below highlight key trends shaping the industry, including scalable data capture and analysis, the impact of tokenization, strategic uses and the limitations of AI, as well as optimizing IT landscapes for investors and hedge funds.

Investment Management Industry Consolidation Continues – Oleg Movchan, CEO

The consolidation process of the investment industry will continue and accelerate. Commercial models for both traditional asset managers and wealth managers are notoriously difficult to scale, requiring a tricky balance between comprehensive asset class and product coverage, talent growth challenges and operating costs. In many market segments, as well as more broadly, a “winner takes all” market structure seems to be taking shape. Therefore, we will continue to see industry consolidation, both across businesses and across product lines – recent M&A transactions in the space are too numerous to list. As such, we expect that open and flexible technology architecture – both in terms of functionality and delivery (SaaS vs. on premise) and ownership (buy vs. build) – will remain central to differentiating between successful and failing M&A strategy, for both acquirers and targets.

Unlocking Private Credit: The Scalable Data Demand – Movchan

Private credit markets are on the precipice of a data-driven transformation that will redefine operational efficiency and replace antiquated technology landscapes. By building scalable, intelligent workflows around comprehensive and robust terms and conditions data (the common language of private credit), firms can establish appropriate technology infrastructure upon which they can optimize their operational ecosystem. Such initiatives will be key drivers in dramatically reducing operational risks and overall costs, as well as creating new value streams. The key to success will be developing a robust, flexible security master and meta-data environment that properly captures the ontology of complex credit instruments and turns this information into strategic, risk and valuation insights.

Tokenization: The Next Frontier of Financial Innovation – Movchan

Tokenization will continue to revolutionize how all financial instruments and real-world assets are traded and managed. Deregulation of financial services, increased appetite for non-traditional asset classes and strategies as well as technological advances, will accelerate the democratization of investment opportunities, creating more liquid and efficient markets. Forward-thinking firms will see tokenization not as a disruption, but as a strategic opportunity to drive and enrich portfolio construction, enhancing business economics while delivering better investment outcomes for their clients.

Portfolio Construction: Breaking Down Asset Class Barriers – Movchan

The future of investment management lies in a holistic portfolio construction paradigm that seamlessly integrates liquid and illiquid asset classes. Advanced data capabilities and sophisticated risk modeling and valuation analytics – powered by scalable security masters, modern analytics and AI and machine learning – will enable firms to create more nuanced, transparent and diversified investment strategies that meet increasingly complex client demands. The firms that can effectively combine these traditionally segregated asset classes will gain a significant competitive advantage.

AI Finds Alpha: Reimagining Investment Intelligence – Movchan

Machine learning and AI will continue to transform alpha generation and capture for investment managers. By combining advanced quantitative models with strategic insights, firms can unlock more efficient information sourcing and risk management by combining data-driven frameworks with discretionary overlays. The most successful investment strategies in 2025 will be those that masterfully blend algorithmic precision with human judgment.

The SaaS Transformation: Achieving Agility by Shifting Solution Delivery Strategies – Movchan

In 2025, asset management firms will accelerate their shift from rigid on-premise systems to flexible SaaS solutions that dramatically reduce total cost of ownership. This transition isn’t just about technology—it’s about creating organizational agility that allows firms to rapidly adapt to market changes, enable growth and provide more custom offerings based on client needs. This can only be accomplished through seamless updates without the need to manually configure functionality, upgrade software and IT infrastructure in response to each new development. The most successful firms will view their technology infrastructure as a strategic enabler, not just a back-office utility, and will partner with their vendors to balance buy vs. build decisions.

In 2025, Data Will Be the Differentiator – Neal Pawar, COO

As AI becomes increasingly open-sourced and customizable, your alpha will be the data you train it with. How you generate, curate, store, secure, remove bias & errors, structure, and deliver data will become a priority for companies looking to leverage AI. Data carries your expertise, your values, your know-how. Data is where your best employees share their best practices for the benefit of the whole workforce. Data is also how your clients steer you to build better products and services. It’s your differentiator.

Future-proof Asset Management by Keeping Lift & Shift in The Rearview – Dan Groman, CTO

By 2025, we’ll see a dramatic shift in how asset management firms approach technology modernization, moving well beyond traditional “lift and shift” cloud migration strategies that have dominated the industry. Nearly all asset managers (95%) recognize technology and digital capabilities as key differentiators, yet many firms remain tethered to legacy systems that impede their ability to adapt and scale. Simply relocating existing systems to the cloud without reimagining their investment operating model will put firms at a significant competitive disadvantage as a result of the time, cost and personnel required to maintain this IT infrastructure. The true differentiator will be the adoption of enterprise-level SaaS solutions that eliminates lift and shift as well as the upgrade trap – which leads to operational disruption as a result of downtime during updates – and hidden costs associated with hardware maintenance, version control, and dedicated IT staffing. Beyond selecting the right approach to modernizing legacy systems, there are other emerging technologies that should be part of anyone’s long term vision.

In 2022, the world was inspired by the release of OpenAI’s ChatGPT and the progress that’s been made since then is nothing short of astonishing. While there is no substitute for subject matter expertise, providing employees with the next generation of tools is paramount. Taking advantage of continued advancements in generative-AI and machine learning requires having a strategy with regard to data accessibility, governance and oversight. A sound strategy regarding data hygiene has never been more critical while modernizing a firm’s technology infrastructure. 2025 will mark a critical turning point as mounting fee pressures, evolving investor demands, and regulatory changes force firms to grapple with the total-cost-of-ownership and wanting to do more with their data.

Looking ahead, the winners in 2025 will be asset managers who embrace fully integrated SaaS platforms that can support any asset class and investment strategy from front to back. These solutions will enable firms to rapidly scale new products like direct indexing and ETFs, as well as leverage new innovative solutions like AI, while maintaining the flexibility to adapt to emerging market opportunities. The ability to pivot quickly and scale efficiently as a result of SaaS deployment will become not just a competitive advantage, but a necessity for survival in an increasingly dynamic market landscape.

+++

About Enfusion

Enfusion’s investment management software-as-a-service (SaaS) platform removes traditional information boundaries, uniting front-, middle- and back-office teams on one cloud-native system. Through its software, analytics, and middle/back-office managed services, Enfusion creates enterprise-wide cultures of real-time, data-driven intelligence, boosting agility, and powering growth. Enfusion partners with over 850 investment managers from 9 global offices spanning four continents.

Cboe Global Markets and Metaurus Advisors, LLC Collaborate on New U.S. Equity Index, First of Four in Planned Dispersion Product Suite

January 07, 2025

Cboe U.S. Large-Mid Cap 100 Index (CEQX) launched on December 20, 2024

New equal-dollar-weighted index comprised of 100 large-mid cap US-listed stocks

Two new planned indices tracking top 50 and bottom 50 performing constituents of CEQX Index

CHICAGO, Jan. 7, 2025 /PRNewswire/ — Cboe Global Markets, Inc. (Cboe: CBOE), the world’s leading derivatives and securities exchange network, and Metaurus Advisors, LLC (Metaurus), an asset management company focusing on financial innovation, today announced their collaboration on the Cboe U.S. Large-Mid Cap 100 Index (CEQX). The CEQX Index, which launched on December 20, 2024, is the first of four indices jointly developed by Cboe and Metaurus.

The CEQX Index is designed to be an equal-dollar-weighted index comprised of 100 large-mid cap U.S. stocks, rebalanced quarterly, that replicates the sector capitalization weightings of the largest companies listed on U.S. exchanges. Following the launch of the CEQX Index, Cboe and Metaurus plan for the introduction of three additional indices – the Cboe Lead 50 Index, the Cboe Lag 50 Index and the Cboe U.S. Large-Mid Cap 100 Cumulative Return Index – in the first quarter of 2025.

“The launch of the Cboe U.S. Large-Mid Cap 100 Index marks an exciting step forward in Cboe’s efforts to making dispersion trading more accessible,” said Rob Hocking, Global Head of Product Innovation at Cboe. “We believe CEQX will not only be a reliable gauge of U.S. large- and mid-cap stock performance, but importantly, also serves as the foundation for additional indices we’re developing. Dispersion trading has seen growing interest from market participants seeking to capitalize on differences in implied volatility between index options and individual stock options, and we couldn’t be more excited to continue to deliver the tools that traders need to unlock new opportunities in this market.”

Derived from the CEQX Index, the Cboe Lead 50 and Cboe Lag 50 indices are expected to be equal-dollar-weighted and designed to measure the total returns of the top 50 and bottom 50 performing companies, respectively, within the Cboe U.S. Large-Mid Cap 100 Index on a quarterly basis. Investors who track the varying quarterly returns of the Cboe Lead 50 and the Cboe Lag 50 indices may gain insight into realized dispersion, a measure of independent movement observed in the components of a diversified portfolio.

“CEQX will serve as the foundational index for the Cboe Lead 50 and Lag 50 indices, providing the market a new and innovative way to gauge realized dispersion,” said Richard Sandulli, Co-CEO of Metaurus. “The relationships between these new indices, along with the planned futures on the Lead/Lag 50 indices, are designed to be simple and intuitive, and mark a steppingstone towards the securitization of new groupings of financial assets.”

The CEQX Index is administered by Cboe Global Indices, a leading derivatives-based index provider, and adds to Cboe’s growing list of innovative index offerings including its suite of volatility indices and its new Cboe Bitcoin U.S. ETF Index. The daily value of the CEQX Index and other indices can be found on the Cboe Global Indices Feed.

Cboe Labs, Cboe’s product innovation arm, plans to launch tradable futures products based on the Cboe Lead 50 and the Cboe Lag 50 indices. The futures are planned to be listed on Cboe Futures Exchange, subject to regulatory review.

About Cboe Global Markets Cboe Global Markets (Cboe: CBOE), the world’s leading derivatives and securities exchange network, delivers cutting-edge trading, clearing and investment solutions to people around the world. Cboe provides trading solutions and products in multiple asset classes, including equities, derivatives and FX, across North America, Europe and Asia Pacific. Above all, we are committed to building a trusted, inclusive global marketplace that enables people to pursue a sustainable financial future. To learn more about the Exchange for the World Stage, visit www.cboe.com.

About Metaurus Advisors, LLC Metaurus Advisors is an SEC-registered investment advisor whose partners have decades of experience developing cutting-edge derivative and structured products. Metaurus’ growing IP portfolio is the basis for multiple strategies utilized in both public and private investment formats. Metaurus is committed to helping investors unlock new sources of investment return. Please visit www.Metaurus.com for more information.

Catherine Clay is Global Head of Derivatives at Cboe Global Markets.

Catherine Clay

What was the highlight of 2024?

Amid geopolitical tensions and macro uncertainty including the Fed’s shifting monetary policy, we saw investors globally increasingly turning to options for the risk management and income generating capabilities they offer. In fact, the industry is on pace for its fifth record year in a row. Part of this growth was due to the increased demand for single-stock and index options. Within Cboe’s proprietary index options, S&P 500 Index (SPX) and Cboe Volatility Index (VIX) options are on track to surpass last year’s record volume. Institutional and retail investors from across the globe have found value in the broad exposure, precise hedging ability and cash-settled nature these products provide.

This was my first year leading the Global Derivatives business and a large part of our success followed a strategic reorganization that unified Cboe’s derivatives businesses, educational institute and innovation hub under one umbrella. This allowed us to lay out a strong foundation for the future with one unified, global team working towards a common objective. Going forward, we can continue to leverage our global expertise, new and existing partnerships, and customer relationships to provide access to options, and advocate for the benefits these products can provide.

What were the key theme(s) for your business in 2024?

Expanding access to options for investors across the globe was a key theme for our business this year. Expanding accessibility comes in a multitude of ways but ultimately the objective is to equip traders with the tools and education they need to be successful. We expanded access through making options trading available on new platforms, enhancing educational resources, or launching new products. In October, we announced plans to partner with Robinhood as they launched index options on their platform, further expanding retail access. The launch of index options on Robinhood was a long time in the making and comes with important guardrails and education to ensure new options traders on the platform are well prepared.

This year we expanded our volatility toolkit, with the launch of Options on VIX Futures and Variance Futures, and the addition of cash-settled index options in the crypto space following the launch of options on the newly created Cboe Bitcoin U.S. ETF Index (CBTX). The CBTX Index options launch is a great example of Cboe’s ecosystem at work. Cboe is the listing exchange for many U.S. spot bitcoin ETFs. Cboe Global Indices developed a new index from these ETFs, we then listed options on the index and are now working with issuers through our Listings business to extend access to these strategies through ETPs. No matter the product or underlying asset, we strive to listen to our customers and work to provide exchange-traded solutions.

What surprised you in 2024?

The appetite for the U.S. markets from foreign investors, especially investors in the Asia Pacific region, was particularly surprising. This is an area that we are increasingly focused on considering the level of sophistication and derivatives knowledge many retail investors already have. By collaborating with local retail brokers, we are looking to provide resources and access to our index options to a new set of customers. Each country in APAC brings its own unique challenges and opportunities with a different regulatory landscape and trading culture. Despite these differences, the common theme of strong demand for U.S. exposure connects them all. Many market structure obstacles — like barriers to market data and tradable products— remain, and we continue to work with our Data Vantage business to ensure investors have the data and tools needed to test trading strategies, understand opportunities and begin trading.

What are your expectations for 2025? Any trends to keep an eye out for?

Going forward, Cboe Global Derivatives will build off the momentum we created this year and strive to shape how global investors manage risk and opportunity. The demand for options has expanded beyond the utility they first provided when Cboe introduced listed options over 50 years ago. We’ve seen a shift in trading as investors implement more short-dated trading strategies, options-based ETFs and options on new asset classes into their portfolios. We will continue to facilitate growth and access to U.S. options market by listening to and educating our customers, working with industry partners and leveraging Cboe’s entire ecosystem. Options can play an important role in portfolios, and Cboe is well-positioned to drive this market forward on a global scale.

TECH TUESDAY is a weekly content series covering all aspects of capital markets technology. TECH TUESDAY is produced in collaboration with Nasdaq.

We see that 2024 turned out to be a pretty good year for many economies, especially the U.S.

Recessions were mostly avoided, inflation returned to around 2% and labor markets remained strong but no longer strained. You could say that last year concluded with economies in a bit of a “Goldilocks” state – not too hot, not too cold.

Labor markets have softened but are still generally healthy

One place where that’s evident is in labor markets.

The past four years have seen extremes for labor markets – from big spikes in unemployment during the early part of Covid then to historically tight labor markets as economies reopened, leading to a shortage of workers.

Now, unemployment is generally near historically low levels, but in many countries, it is rising (chart below). That’s a sign that the supply of labor is back in line with demand for labor. In fact, in the U.S., the number of jobs per person looking for work has fallen from 2-to-1 to a much more balanced 1.1-to-1.

That’s good for companies, as it’s getting easier to hire staff. It’s also good news for inflation, as the pace of wages growth is also slowing.

Jobs markets are “not too hot, and not too cold.”

Chart 1: Unemployment rates are low (but mostly increasing)

Inflation is back near 2% targets around the world

We all know that inflation increased dramatically during Covid. That was mostly due to supply chain disruptions caused by Covid, wage pressures from tight labor markets and the Ukraine conflict. The prices of goods, energy and food all rose. Data shows that consumer prices in the U.S. are now around 22% higher and wages are 25% higher than before Covid.

But with supply chains fixed and wage growth cooling, headline inflation around the world has fallen. It is back around 2% in many of the world’s largest economies (chart below).

In short, inflation is very close to being “just right.”

Chart 2: Inflation back near central bank targets

GDP growth just strong enough to avoid recession

The main tool central banks used to get inflation back under control was higher interest rates. Often, that slows the economy too much, leading to a recession, which many were worried about back in 2023.

However, the data shows that, although growth is slow in some places, most countries have avoided recession. Generally, countries seem to have achieved a so-called “soft landing.”

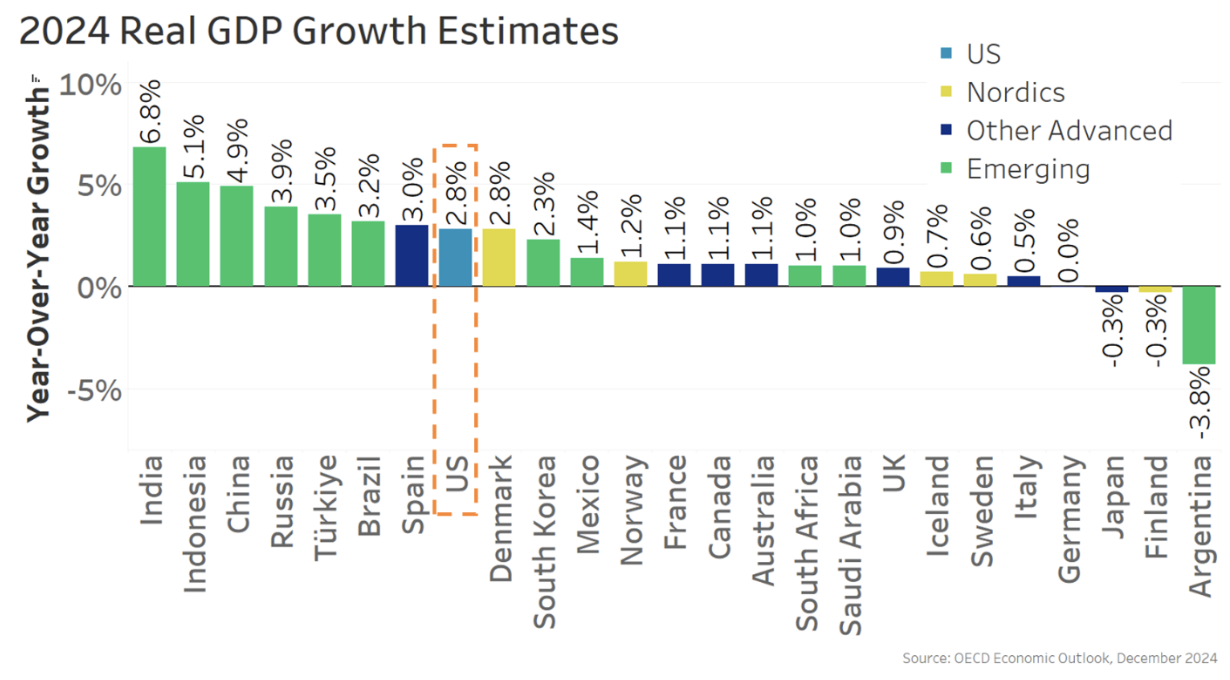

Chart 3: U.S. stands out for its strong growth among advanced economies in 2024

So, as we exit 2024, we have what is pretty close to a “Goldilocks” economy – not too hot, not too cold.

Interestingly, the U.S. has seen one of the strongest economies in 2024, where we have a 4.2% unemployment rate, 2.4% inflation rate, and are on pace for nearly 3% real GDP growth.

Rate cuts underway, with more expected in 2025, should help boost growth

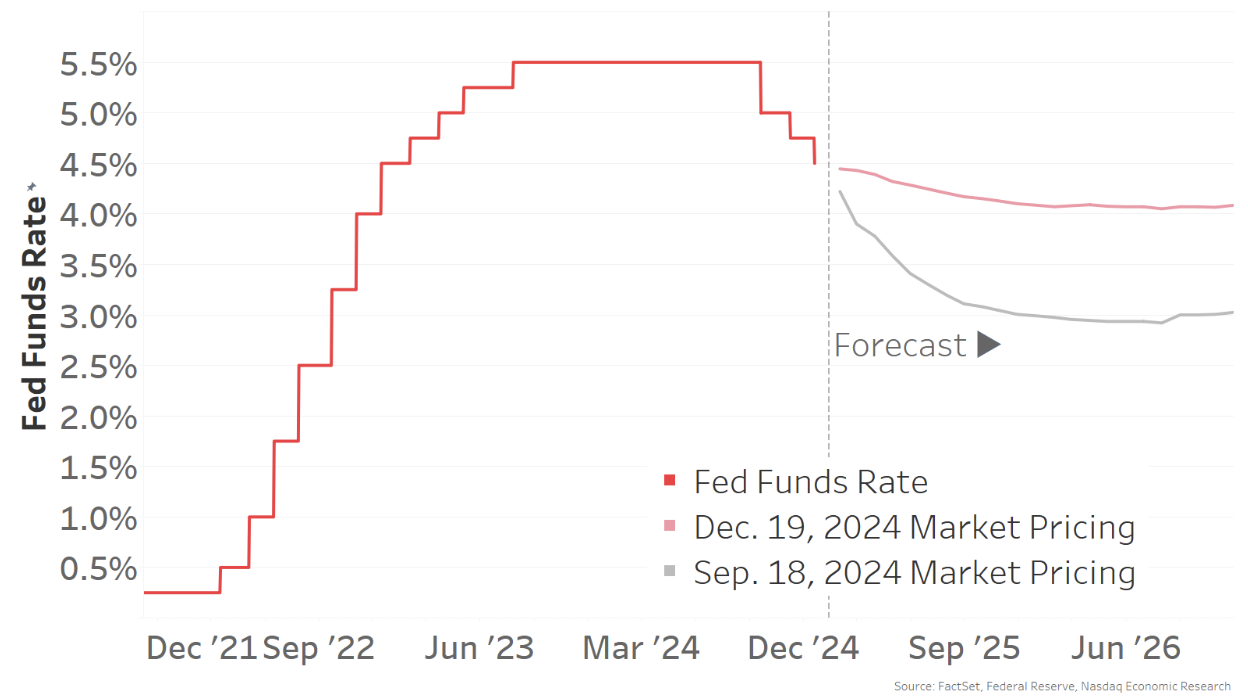

With inflation down and employment markets softer, central banks have already started to reduce rates. Based on the U.S. Fed’s own estimates, current short-term interest rates are still at levels that are “restrictive” – or above the neutral rate. As a result, rates are expected to fall more in 2025. The big question is how much.

Just three months ago, markets were pricing in a Fed funds rate of around 3.0% by the end of 2025 – a fall of around 1.5% from current levels.

By December, a lot had changed. Markets now only expect rates to fall to around 4.0%, and maybe not reach that level until 2026. In short, we are seeing rates staying higher-for-longer again. For interest rate-sensitive segments of the economy, that could affect investment and growth.

Chart 4: Interest rates are falling in most countries, with more cuts expected in 2025

Global stock markets had a mostly good year in 2024

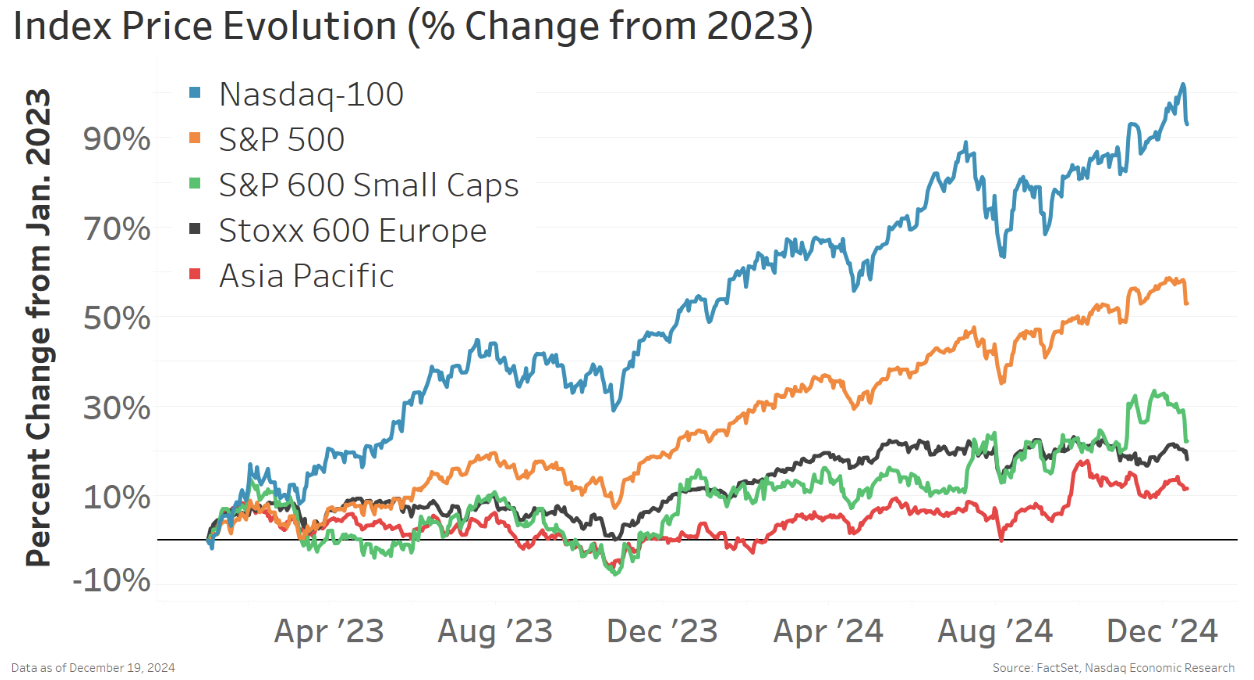

Overall, 2024 was a good year for stock markets. Many countries saw earnings recoveries, which, combined with lower interest rates, helped push stock valuations up.

However, returns in the U.S. large cap stocks – and especially for Nasdaq-100® stocks – were much higher than most other regions or market caps.

Chart 5: Most stock markets are up in 2024, but U.S. mega cap saw stronger returns

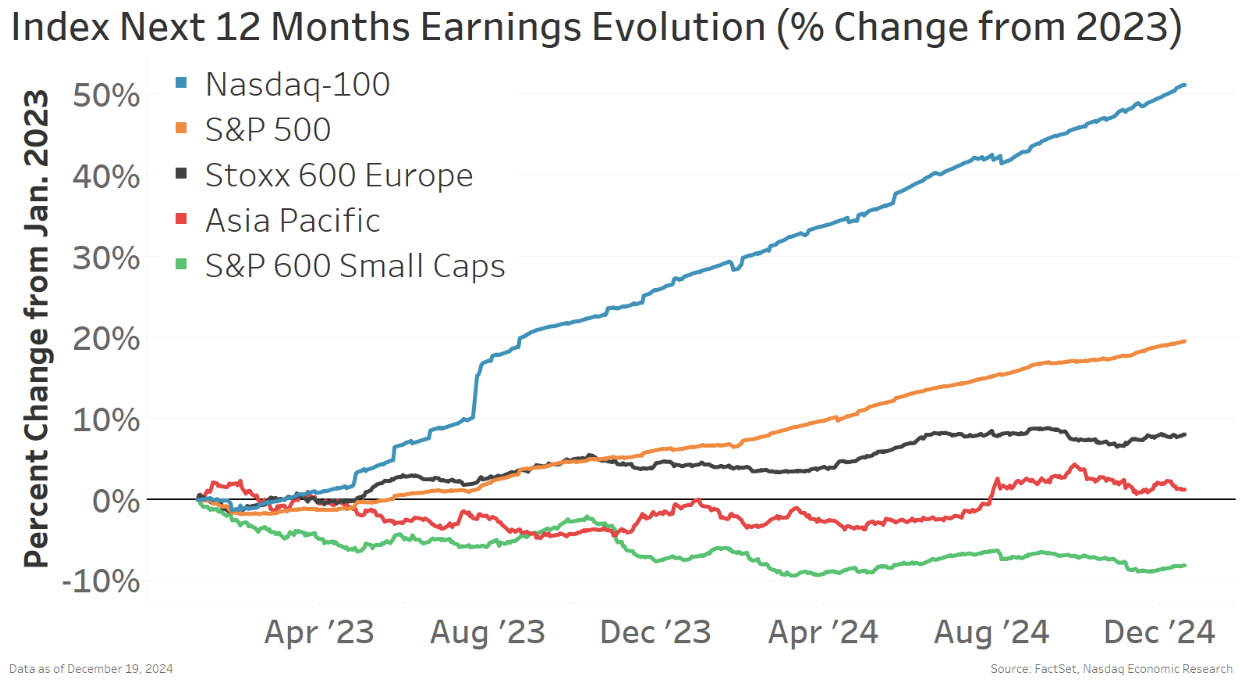

Interestingly, looking at earnings in the same indexes we see the same trends.

The outperformance of the Nasdaq-100® is supported by far stronger earnings growth. While U.S. small caps are mired in an earnings recession.

Chart 6: Earnings trends mirror stock returns

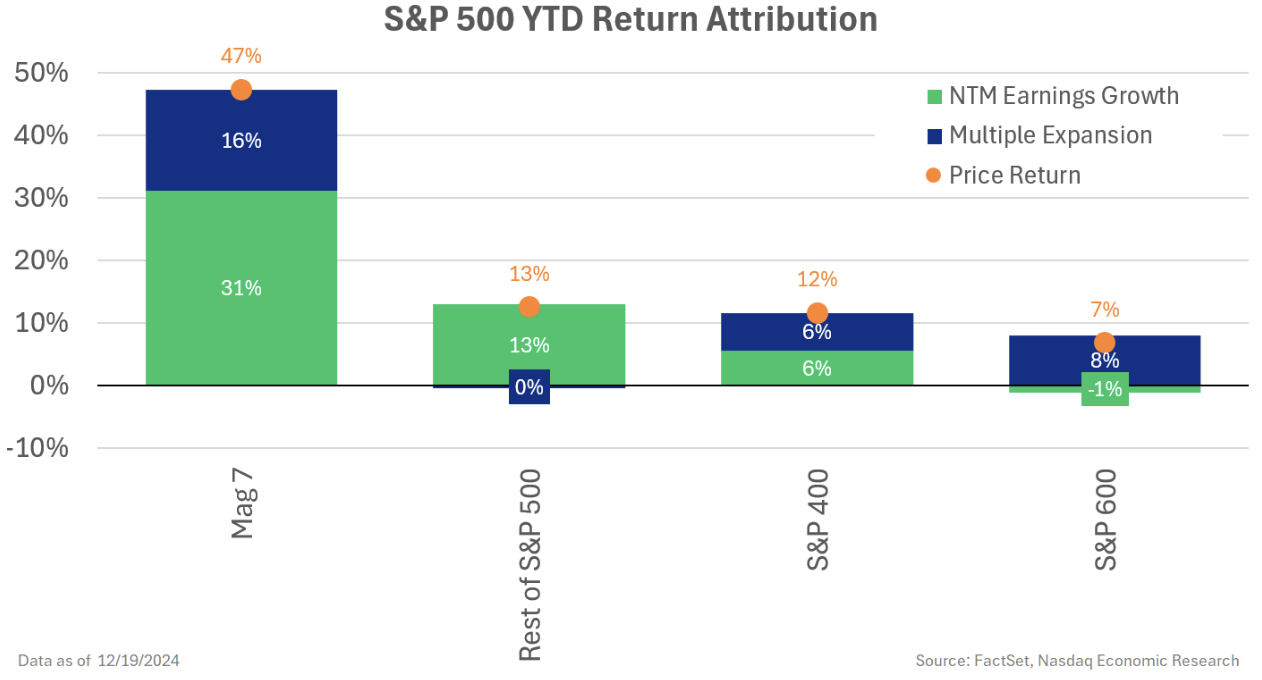

Taking a closer look at earnings in the large cap indexes, we see that earnings growth in the S&P 500 has been driven predominantly by the so called “Mag 7” stocks.

All those stocks are exposed to the spending on artificial intelligence, which some estimate is running well over $200 billion per year. Nvidia makes the GPU chips sought after for calibrating AI models. Amazon, Microsoft and Google all run cloud data centers, which are key to processing all the data, and Apple,Tesla and Meta are among the first movers using AI in their products.

Because all are Nasdaq listings, they make up an even larger proportion of the Nasdaq-100 Index® – helping the Nasdaq-100® outperform the broader S&P 500 index.

Chart 7: Large-cap earnings are driven by the Mag 7 stocks

Importantly though, as we have progressed through 2024, we have seen a broadening of the earnings recovery in the rest of the large cap stocks.

Lower rates would be good for small companies

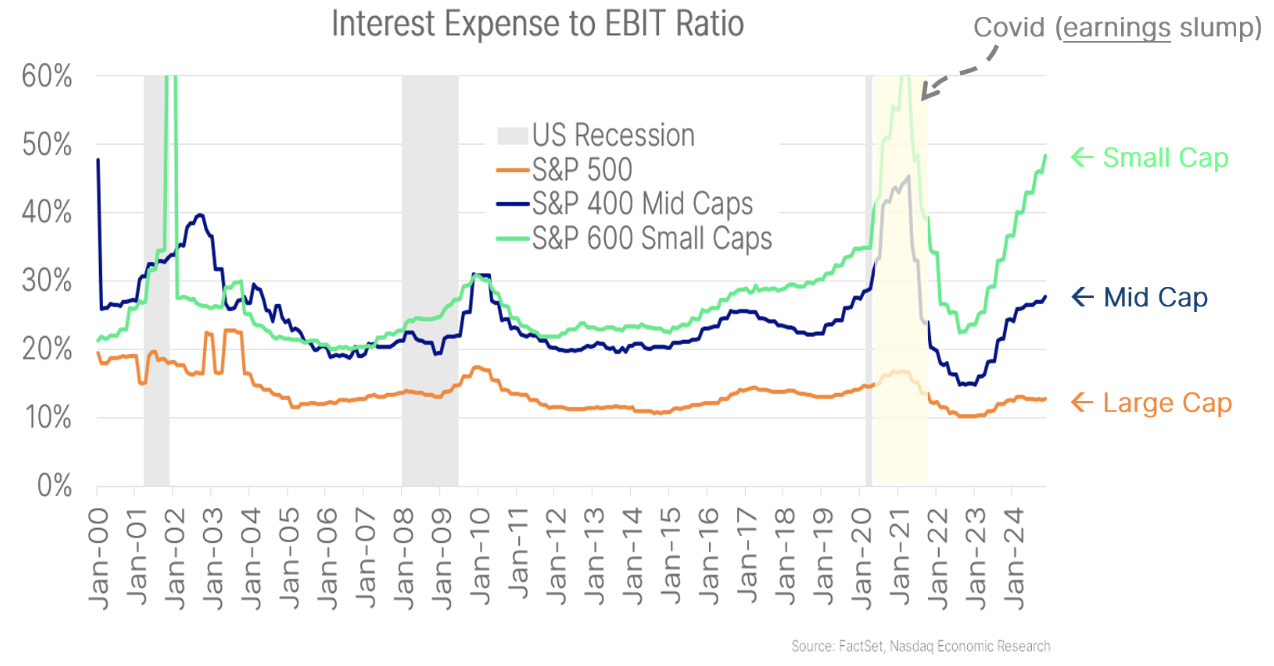

When we look at the difference between large-cap and small-cap stocks, one thing stands out. Interest expenses are reducing profits of small cap companies much more than for large-cap companies.

Some data shows that higher interest rates have especially impacted smaller companies, with interest expense/profit ratios at multidecade high levels. In contrast, the proportion of interest expense for large cap companies is near record low levels – and has hardly increased despite rising interest rates.

Chart 8: Interest rates are affecting small-cap companies much more than larger companies

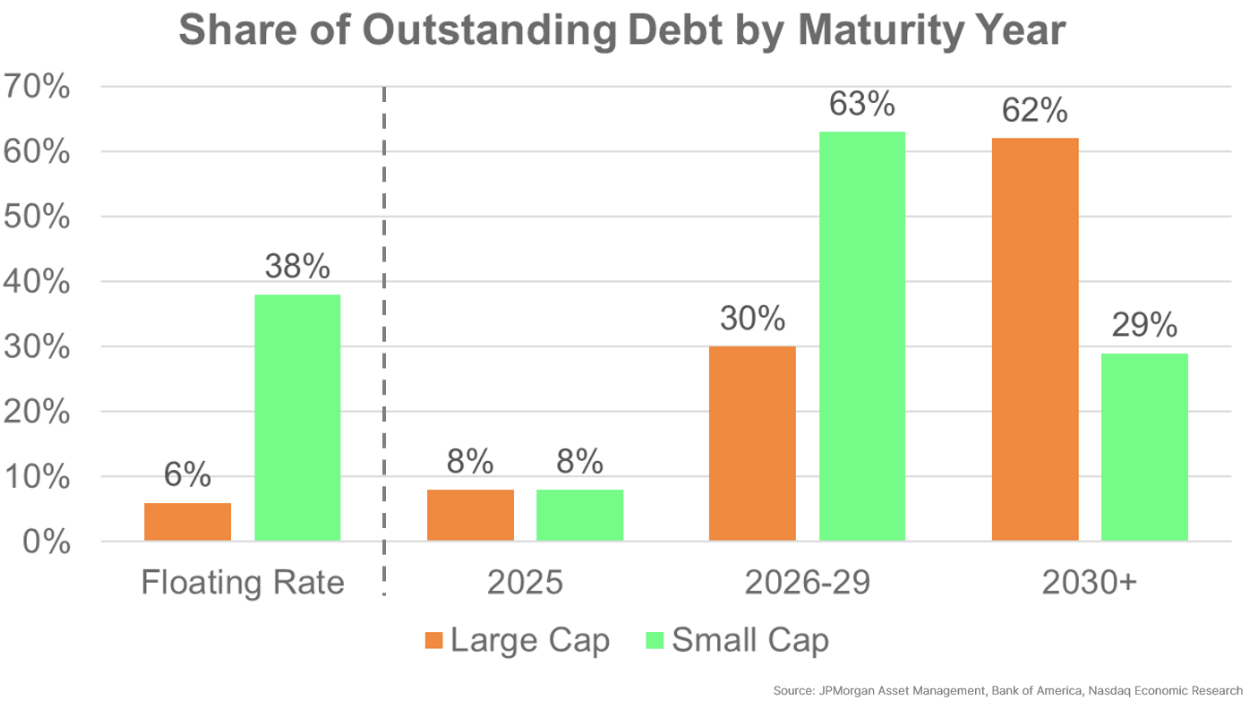

The different sensitivity to interest rates is supported by looking at company debt financing across market cap. We see that large-cap companies have very little floating rate debt, which has insulated them from Fed interest rate increases. In fact, large-cap companies seem to have fixed rates on the majority of their debt, at low rates, out to at least 2030.

In contrast, small-cap companies have around a third of their debt at floating rates, with a large proportion of fixed rate debt scheduled to refinance starting in 2026. Clearly, small-cap companies will be more impacted by rates staying higher-for-longer.

Chart 9: Small-cap companies are much more exposed to higher short-term interest rates

2025: No signs yet of consumer weakness

Overall, the reason the U.S. economy performed so well in 2024 was because the U.S. consumer remained strong. Real spending (adjusted for inflation) is up almost 15% compared to right before Covid. That’s a lot better than Europe, where real spending has barely increased.

Chart 10: U.S. consumer spending stands out among other advanced economies

A number of factors have helped maintain consumer spending growth in the U.S.

Firstly, after experiencing the Credit Crisis back in 2008, most U.S. households have now locked in long-term fixed mortgage rates. Just like large-cap companies, despite the Fed increasing official interest rates and new mortgage rates almost tripling, the average interest rate on outstanding mortgages barely increased – and remains around 4%. That has left more money in people’s pockets – and means monetary policy has had a more muted impact on consumers.

Secondly, with wage gains that started in the “Great Resignation,” and then broadened to include most workers, real wages have also grown. That, combined with strong employment and low risks of layoffs, has given the consumer the confidence to keep spending.

With interest rates higher, even savers are earning more income.

Finally, higher house prices have also left household balance sheets in a strong position. Recent data showing increases in home equity loans (HELOCs) suggest some might finally be tapping into debt markets, allowing spending to persist.

So far, there are few signs of weakness. Credit card debt, although at new highs, is relatively low as a proportion of income and household net assets. In fact, even the increase in unemployment (Chart 1) that the U.S. has seen is mostly due to more workers looking for jobs. Layoffs, which more typically lead into recessions, remain near multidecade low levels.

Chart 11: Low layoffs have helped consumers keep spending

2025: Strong underlying economy with a chance of uncertainty

There are a lot of positive signs for the U.S. economy and the stock market heading into 2025.

The consumer remains strong, thanks to robust household balance sheets and a strong job market.

Company earnings are recovering. Expected tax cuts and looser regulation in 2025 should help boost earnings, too. Although some uncertainty exists for companies that have to deal with higher longer-term interest rates, possible new tariffs and potential new labor shortages.

Looking at the bigger picture, further interest rate cuts, combined with tax cuts and net positive government spending, should keep the U.S. economy growing for at least another year. That should also be good for stocks.

Phil Mackintosh is Chief Economist at Nasdaq. Michael Normyle is U.S. Economist and Senior Director at Nasdaq.

Creating tomorrow’s markets today. Find out more about Nasdaq’s offerings to drive your business forward here.

Brian Steele isManaging Director, President, Clearing & Securities Services, DTCC.

Brian Steele

What were the key theme(s) for your business in 2024?

DTCC has played a unique and critical role in the industry for over 50 years. In 2024, the industry again looked to us to lead some of the most sweeping changes to market structure in history, including the successful implementation of T+1 in North America, preparing the industry for expanded US Treasury clearing and advancing the digitization of financial markets. These initiatives required us to work collaboratively with market participants, industry organizations and key stakeholders, while advancing our efforts to modernize our platforms to improve the client experience and strengthen resiliency.

What was the highlight of 2024?

While there were many achievements in 2024, the U.S. transition to T+1 stands out given its scope and impact. It required market participants to collaborate and execute this historic change. For several years, we worked closely with the industry to identify and resolve issues, educate firms, increase automation, and test readiness to ensure a safe and successful transition. As part of this, we heavily focused on improving industry affirmation rates through automation to solve a long-standing industry challenge. Since implementation, the industry is affirming nearly 95% of transactions by the 9 p.m. DTC cutoff, which represents a significant improvement over pre-T+1 rates. In addition, accelerating settlement delivered significant capital and liquidity benefits enabling us to provide $3 billion dollars in clearing fund savings back to the industry, all without increasing fails. With this success, we are now seeing the United Kingdom, Europe and countries in Asia begin work on aligning their settlement cycles. We look forward to sharing our learnings and expertise to support their journeys.

What are your expectations for 2025?

While the geopolitical and macroeconomic environment remain highly uncertain, we are very focused on delivering on our strategic priorities – most notably, the expansion of U.S. Treasury clearing. With deadlines quickly approaching for customer margin segregation in March 2025, followed by cash clearing in December 2025 and repo clearing in June 2026, we continue to work closely with our clients to address the impacts of the rule and how they need to prepare for the transition. We’re leading industry efforts in a number of areas, including initiatives to support done away transactions via our Sponsored Service and recently SEC-approved Agent Clearing Service access models, as well as identifying ways to solve accounting treatment challenges. At the same time, DTCC is pursuing opportunities to drive additional capital and liquidity efficiencies via cross-margining arrangements, the creation of default funds and other innovative approaches. We’ll continue to partner closely with our clients and the industry to ensure smooth implementations.

DTCC Executive Predictions for 2025

Frank La Salla, President, CEO, and Director of DTCC

While the macroeconomic and geopolitical environment will remain uncertain in 2025, I’m optimistic about our industry’s future and the opportunity for DTCC to lead on critical initiatives that mitigate risk, enhance resilience and strengthen market structure. In that sense, this year will largely be a continuation of 2024 in that we must continue to execute flawlessly on large-scale industry implementations. On the heels of the smooth T+1 conversion, we will galvanize the industry and provide strong leadership on the transition to the SEC’s U.S. Treasury Clearing rule.

In addition, innovation will be an area of sharp focus for our firm. We’ve already been integrating digitization, cloud and AI into our capabilities, and we’ll continue to advance this important work in the coming years. However, we also recognize that not all innovation will be underpinned by technology, which means that we’ll also focus on opportunities to improve market safety and efficiency through process enhancements, cross-margining agreements and other creative approaches.

Technologies such as blockchain and the cloud will play a crucial role in the build out and interconnectedness of the digital financial ecosystem. DTCC will continue to serve as a strategic partner to the industry by advancing acceptance and adoption of digital assets, focusing on opportunities to tokenize collateral and funds, and leveraging our existing clearing and settlement capabilities to facilitate the listing of digital funds on exchanges as well as secondary trading. We’ll also continue to advance our use of AI where it will be strategically beneficial to the client experience.

Videos:

# # #

Lynn Bishop, Chief Information Officer

We continue to focus on upgrading and modernizing our technology to provide clients and the industry with innovative services and capabilities they need today and in the future. In 2025, one of our top priorities will be readying our IT platforms and client-facing applications to support US Treasury Clearing, which represents one of the most significant changes to market structure in decades. In addition, given the evolving threat landscape, we’re committed to strengthening our resiliency and partnering with our clients and technology providers to ensure financial markets continue to operate seamlessly.

We’re also investing in AI and exploring how it can improve the client experience as well as to enhance our own productivity and efficiency. As AI continues to mature, it becomes essential to upskill employees with a foundational knowledge of AI to drive innovation and pursue practical and responsible use cases.

Videos:

# # #

Nadine Chakar, Managing Director, Global Head of DTCC Digital Assets

2024 was a pivotal year for digital assets, and we’re seeing strong momentum toward adoption. More and more institutional investors – on both the buy- and sell-side – continue to be getting engaged with this technology. We also saw a lot of progress on the regulatory front, with the SEC’s approval of Ethereum and Bitcoin ETFs in the US in 2024, and the first stages of the EU’s MiCA, the first-ever blockchain-related asset regulation, coming into effect.

We still have our work cut out for us in 2025 and beyond. While we’ve clearly proven the merits of this technology, it’s time to put real applications on the ledger using tokenization. As we move beyond pilots and start putting projects into production, we’ll need to make sure we’re collectively driving toward an end goal: building an efficient digital market infrastructure and standards. Collaboration is the core ingredient that will help us capture the promise that digital assets hold.

DTCC is excited to be at the forefront, leading the charge for industry acceptance and greater adoption of tokenization solutions. We are proud to have further advanced this work with the launch of DTCC Digital Launchpad, an industry sandbox that’s bringing together financial market participants and clearing the path to scalable adoption of digital assets. In 2025, we will continue to focus on establishing the digital market infrastructure of the future, showcasing how we can deliver the same efficiencies for digital assets as we do in traditional markets today, while also ensuring smooth market operation, transparency and liquidity.

# # #

Timothy Cuddihy, Managing Director and Group Chief Risk Officer at DTCC

As the threat landscape evolves and the nature of risk takes on new forms in the coming year, DTCC will continue to focus on strong risk management practices and robust operational resilience. Effective risk management is imperative given the heightened geopolitical risks, macro-economic uncertainty, cyber threats, and pace of technology change. Given DTCC’s role in mitigating risk, we are always focused on assessing and protecting against multiple and interconnected risks to the global financial system.

To ensure defense against ever-evolving risks,firms must embrace a holistic approach to risk management, combining real-time threat detection, advanced automation, and collaboration across the financial ecosystem. The key to navigating this environment lies in building and implementing adaptable, forward-looking frameworks that not only address today’s risks but forward-looking risk assessments to prepare for dynamic challenges ahead.

# # #

Brian Steele, Managing Director, President, Clearing & Securities Services at DTCC

The expansion of U.S. Treasury clearing is a huge priority for us in 2025. With deadlines fast approaching, DTCC is fully committed to a successful implementation, and we are working closely with the industry to educate clients on the impacts and preparations needed to ensure a smooth transition and to deliver upon the transparency and risk management benefits of such a move. Driving capital and liquidity efficiencies for the industry is a keen focus area for DTCC, which is why we are doubling down to improve our solutions (i.e. cross margining arrangements, creation of default fund, etc.) and enable our clients to maximize capital while complying with mandates such as Basel III rules, etc.

At the same time, we stand ready to assist the industry as global accelerated settlement efforts progress in EU and UK. We will continue to engage our clients through various forums as we look to expand and develop new products and services such as cleared securities lending, optimizing the use of Collateral, increase the usability and access of our data, and improve our clients’ experience by modernizing platforms and increasing resiliency. We are also actively preparing to support our clients through regulatory change efforts impacting RDS (i.e. Canada, JFSA Phase III and HKMA rewrite) and continue to invest in risk management excellence to protect the industry.

# # #

Michele Hillery, Managing Director, Head of Repository & Derivatives Services

2024 was a significant year in which the derivatives markets were shaped by substantial regulatory reporting updates. Global refits across North America, UK, EU, Singapore, Japan and Australia delivered enhanced transparency and greater efficiency across global capital markets, as firms tackled legacy trades and aligned reporting across jurisdictions, with swift action and robust data strategies proving crucial to implementation success.

The pace of regulatory change shows no sign of slowing in 2025, with global jurisdictions including Canada, Japan and Hong Kong preparing to go live with the UPI reporting as part of the derivatives trade reporting rules.

To ensure preparedness, firms should continue to build on lessons learned from past implementations. Early preparation and collaboration, continuous adaptation, and strong industry partnerships will all be critical to ensuring compliance and strengthening post-trade infrastructure and reporting as the industry continues to evolve.

# # #

Laura Klimpel, Managing Director and Head of DTCC’s Fixed Income and Financing Solutions

2024 has been a pivotal year in industry preparations for the expanded UST clearing as a result of the SEC mandate, resulting in a significant and continued growth in fixed income clearing volumes. Throughout the year, FICC remained focused on providing the most efficient and resilient clearing services for the industry. On September 30, FICC’s Government Securities Division saw record daily volumes of over $10 Trillion and its Sponsored Service alone reached peak daily volumes over USD$1.7 trillion, creating USD$846 billion in balance sheet savings across the industry. FICC is built for scale, and the record-breaking clearing volumes seen over the course of the past year are testament to its ability to meet the growing demand.

To help the industry prepare for the 2025 and 2026 regulatory deadlines, FICC has made significant strides in advancing how we will support done-away clearing in the Treasury market. Both of our indirect access models, the Sponsored Service and the Agent Clearing Service which was recently approved by the SEC, support done-away activity. We are also addressing remaining challenges around accounting implications – with resolution anticipated imminently – and will continue to roll out innovative products and services that create new margin and capital efficiencies for our clients. Looking ahead, we will continue to listen and respond to the needs of the industry to ensure that firms are well prepared for the Treasury clearing mandate and ensure a seamless implementation.

# # #

Tim Lind, Managing Director of DTCC Data Services

2024 was a year of transformation for asset servicing, driven by data-centric approaches that leverage new data sources to enable greater integrity and insight into valuation, risk management and liquidity dynamics. AI and cloud-based data marketplaces will accelerate transformation of the data supply chain by replacing point-to-point connectivity between institutions with collaborative alternatives that focus on sharing, rather than sending data.

As a leading market infrastructure provider and trusted partner to American issuers, we are poised to lead this change. DTCC will harness its data assets and innovative technologies in service to the capital markets industry, and bring issuers, intermediaries and investors closer together than previously imagined.

# # #

Val Wotton, Managing Director and General Manager of DTCC Institutional Trade Processing

2024 marked the successful implementation of T+1 in the US, which delivered substantial risk mitigation and operational and cost efficiency benefits to market participants. Under the new timeline, over 95% of transactions are meeting the affirmation criteria, a notable improvement from the 73% affirmation rate under T+2. Market participants have also benefitted from the significant reduction in margin requirements, allowing them to make better use of their capital and resources, while simultaneously reinforcing financial stability. Global accelerated settlement cycles will continue to be the key theme for market participants in 2025, with attention shifting to implementation in the UK and Europe. DTCC wholly supports the recently published UK’s Accelerated Settlement Taskforce Recommendations which focus on post-trade automation as a T+1 enabler, and ESMA’s recently issued Final Report, which calls for automation and harmonization across the EU region in order to make the move to a T+1 settlement cycle. We recommend that market participants approach T+1 implementation in the UK and Europe as an opportunity to evaluate holistically at their middle and back-office functions and assess how they can increase operational efficiency through automation and standardization through central matching solutions that enable same day confirmation.