Cboe Global Markets and Metaurus Advisors, LLC Collaborate on New U.S. Equity Index, First of Four in Planned Dispersion Product Suite

January 07, 2025

Cboe U.S. Large-Mid Cap 100 Index (CEQX) launched on December 20, 2024

New equal-dollar-weighted index comprised of 100 large-mid cap US-listed stocks

Two new planned indices tracking top 50 and bottom 50 performing constituents of CEQX Index

CHICAGO, Jan. 7, 2025 /PRNewswire/ — Cboe Global Markets, Inc. (Cboe: CBOE), the world’s leading derivatives and securities exchange network, and Metaurus Advisors, LLC (Metaurus), an asset management company focusing on financial innovation, today announced their collaboration on the Cboe U.S. Large-Mid Cap 100 Index (CEQX). The CEQX Index, which launched on December 20, 2024, is the first of four indices jointly developed by Cboe and Metaurus.

The CEQX Index is designed to be an equal-dollar-weighted index comprised of 100 large-mid cap U.S. stocks, rebalanced quarterly, that replicates the sector capitalization weightings of the largest companies listed on U.S. exchanges. Following the launch of the CEQX Index, Cboe and Metaurus plan for the introduction of three additional indices – the Cboe Lead 50 Index, the Cboe Lag 50 Index and the Cboe U.S. Large-Mid Cap 100 Cumulative Return Index – in the first quarter of 2025.

“The launch of the Cboe U.S. Large-Mid Cap 100 Index marks an exciting step forward in Cboe’s efforts to making dispersion trading more accessible,” said Rob Hocking, Global Head of Product Innovation at Cboe. “We believe CEQX will not only be a reliable gauge of U.S. large- and mid-cap stock performance, but importantly, also serves as the foundation for additional indices we’re developing. Dispersion trading has seen growing interest from market participants seeking to capitalize on differences in implied volatility between index options and individual stock options, and we couldn’t be more excited to continue to deliver the tools that traders need to unlock new opportunities in this market.”

Derived from the CEQX Index, the Cboe Lead 50 and Cboe Lag 50 indices are expected to be equal-dollar-weighted and designed to measure the total returns of the top 50 and bottom 50 performing companies, respectively, within the Cboe U.S. Large-Mid Cap 100 Index on a quarterly basis. Investors who track the varying quarterly returns of the Cboe Lead 50 and the Cboe Lag 50 indices may gain insight into realized dispersion, a measure of independent movement observed in the components of a diversified portfolio.

“CEQX will serve as the foundational index for the Cboe Lead 50 and Lag 50 indices, providing the market a new and innovative way to gauge realized dispersion,” said Richard Sandulli, Co-CEO of Metaurus. “The relationships between these new indices, along with the planned futures on the Lead/Lag 50 indices, are designed to be simple and intuitive, and mark a steppingstone towards the securitization of new groupings of financial assets.”

The CEQX Index is administered by Cboe Global Indices, a leading derivatives-based index provider, and adds to Cboe’s growing list of innovative index offerings including its suite of volatility indices and its new Cboe Bitcoin U.S. ETF Index. The daily value of the CEQX Index and other indices can be found on the Cboe Global Indices Feed.

Cboe Labs, Cboe’s product innovation arm, plans to launch tradable futures products based on the Cboe Lead 50 and the Cboe Lag 50 indices. The futures are planned to be listed on Cboe Futures Exchange, subject to regulatory review.

About Cboe Global Markets Cboe Global Markets (Cboe: CBOE), the world’s leading derivatives and securities exchange network, delivers cutting-edge trading, clearing and investment solutions to people around the world. Cboe provides trading solutions and products in multiple asset classes, including equities, derivatives and FX, across North America, Europe and Asia Pacific. Above all, we are committed to building a trusted, inclusive global marketplace that enables people to pursue a sustainable financial future. To learn more about the Exchange for the World Stage, visit www.cboe.com.

About Metaurus Advisors, LLC Metaurus Advisors is an SEC-registered investment advisor whose partners have decades of experience developing cutting-edge derivative and structured products. Metaurus’ growing IP portfolio is the basis for multiple strategies utilized in both public and private investment formats. Metaurus is committed to helping investors unlock new sources of investment return. Please visit www.Metaurus.com for more information.

Catherine Clay is Global Head of Derivatives at Cboe Global Markets.

Catherine Clay

What was the highlight of 2024?

Amid geopolitical tensions and macro uncertainty including the Fed’s shifting monetary policy, we saw investors globally increasingly turning to options for the risk management and income generating capabilities they offer. In fact, the industry is on pace for its fifth record year in a row. Part of this growth was due to the increased demand for single-stock and index options. Within Cboe’s proprietary index options, S&P 500 Index (SPX) and Cboe Volatility Index (VIX) options are on track to surpass last year’s record volume. Institutional and retail investors from across the globe have found value in the broad exposure, precise hedging ability and cash-settled nature these products provide.

This was my first year leading the Global Derivatives business and a large part of our success followed a strategic reorganization that unified Cboe’s derivatives businesses, educational institute and innovation hub under one umbrella. This allowed us to lay out a strong foundation for the future with one unified, global team working towards a common objective. Going forward, we can continue to leverage our global expertise, new and existing partnerships, and customer relationships to provide access to options, and advocate for the benefits these products can provide.

What were the key theme(s) for your business in 2024?

Expanding access to options for investors across the globe was a key theme for our business this year. Expanding accessibility comes in a multitude of ways but ultimately the objective is to equip traders with the tools and education they need to be successful. We expanded access through making options trading available on new platforms, enhancing educational resources, or launching new products. In October, we announced plans to partner with Robinhood as they launched index options on their platform, further expanding retail access. The launch of index options on Robinhood was a long time in the making and comes with important guardrails and education to ensure new options traders on the platform are well prepared.

This year we expanded our volatility toolkit, with the launch of Options on VIX Futures and Variance Futures, and the addition of cash-settled index options in the crypto space following the launch of options on the newly created Cboe Bitcoin U.S. ETF Index (CBTX). The CBTX Index options launch is a great example of Cboe’s ecosystem at work. Cboe is the listing exchange for many U.S. spot bitcoin ETFs. Cboe Global Indices developed a new index from these ETFs, we then listed options on the index and are now working with issuers through our Listings business to extend access to these strategies through ETPs. No matter the product or underlying asset, we strive to listen to our customers and work to provide exchange-traded solutions.

What surprised you in 2024?

The appetite for the U.S. markets from foreign investors, especially investors in the Asia Pacific region, was particularly surprising. This is an area that we are increasingly focused on considering the level of sophistication and derivatives knowledge many retail investors already have. By collaborating with local retail brokers, we are looking to provide resources and access to our index options to a new set of customers. Each country in APAC brings its own unique challenges and opportunities with a different regulatory landscape and trading culture. Despite these differences, the common theme of strong demand for U.S. exposure connects them all. Many market structure obstacles — like barriers to market data and tradable products— remain, and we continue to work with our Data Vantage business to ensure investors have the data and tools needed to test trading strategies, understand opportunities and begin trading.

What are your expectations for 2025? Any trends to keep an eye out for?

Going forward, Cboe Global Derivatives will build off the momentum we created this year and strive to shape how global investors manage risk and opportunity. The demand for options has expanded beyond the utility they first provided when Cboe introduced listed options over 50 years ago. We’ve seen a shift in trading as investors implement more short-dated trading strategies, options-based ETFs and options on new asset classes into their portfolios. We will continue to facilitate growth and access to U.S. options market by listening to and educating our customers, working with industry partners and leveraging Cboe’s entire ecosystem. Options can play an important role in portfolios, and Cboe is well-positioned to drive this market forward on a global scale.

Brian Steele isManaging Director, President, Clearing & Securities Services, DTCC.

Brian Steele

What were the key theme(s) for your business in 2024?

DTCC has played a unique and critical role in the industry for over 50 years. In 2024, the industry again looked to us to lead some of the most sweeping changes to market structure in history, including the successful implementation of T+1 in North America, preparing the industry for expanded US Treasury clearing and advancing the digitization of financial markets. These initiatives required us to work collaboratively with market participants, industry organizations and key stakeholders, while advancing our efforts to modernize our platforms to improve the client experience and strengthen resiliency.

What was the highlight of 2024?

While there were many achievements in 2024, the U.S. transition to T+1 stands out given its scope and impact. It required market participants to collaborate and execute this historic change. For several years, we worked closely with the industry to identify and resolve issues, educate firms, increase automation, and test readiness to ensure a safe and successful transition. As part of this, we heavily focused on improving industry affirmation rates through automation to solve a long-standing industry challenge. Since implementation, the industry is affirming nearly 95% of transactions by the 9 p.m. DTC cutoff, which represents a significant improvement over pre-T+1 rates. In addition, accelerating settlement delivered significant capital and liquidity benefits enabling us to provide $3 billion dollars in clearing fund savings back to the industry, all without increasing fails. With this success, we are now seeing the United Kingdom, Europe and countries in Asia begin work on aligning their settlement cycles. We look forward to sharing our learnings and expertise to support their journeys.

What are your expectations for 2025?

While the geopolitical and macroeconomic environment remain highly uncertain, we are very focused on delivering on our strategic priorities – most notably, the expansion of U.S. Treasury clearing. With deadlines quickly approaching for customer margin segregation in March 2025, followed by cash clearing in December 2025 and repo clearing in June 2026, we continue to work closely with our clients to address the impacts of the rule and how they need to prepare for the transition. We’re leading industry efforts in a number of areas, including initiatives to support done away transactions via our Sponsored Service and recently SEC-approved Agent Clearing Service access models, as well as identifying ways to solve accounting treatment challenges. At the same time, DTCC is pursuing opportunities to drive additional capital and liquidity efficiencies via cross-margining arrangements, the creation of default funds and other innovative approaches. We’ll continue to partner closely with our clients and the industry to ensure smooth implementations.

TECH TUESDAY is a weekly content series covering all aspects of capital markets technology. TECH TUESDAY is produced in collaboration with Nasdaq.

We see that 2024 turned out to be a pretty good year for many economies, especially the U.S.

Recessions were mostly avoided, inflation returned to around 2% and labor markets remained strong but no longer strained. You could say that last year concluded with economies in a bit of a “Goldilocks” state – not too hot, not too cold.

Labor markets have softened but are still generally healthy

One place where that’s evident is in labor markets.

The past four years have seen extremes for labor markets – from big spikes in unemployment during the early part of Covid then to historically tight labor markets as economies reopened, leading to a shortage of workers.

Now, unemployment is generally near historically low levels, but in many countries, it is rising (chart below). That’s a sign that the supply of labor is back in line with demand for labor. In fact, in the U.S., the number of jobs per person looking for work has fallen from 2-to-1 to a much more balanced 1.1-to-1.

That’s good for companies, as it’s getting easier to hire staff. It’s also good news for inflation, as the pace of wages growth is also slowing.

Jobs markets are “not too hot, and not too cold.”

Chart 1: Unemployment rates are low (but mostly increasing)

Inflation is back near 2% targets around the world

We all know that inflation increased dramatically during Covid. That was mostly due to supply chain disruptions caused by Covid, wage pressures from tight labor markets and the Ukraine conflict. The prices of goods, energy and food all rose. Data shows that consumer prices in the U.S. are now around 22% higher and wages are 25% higher than before Covid.

But with supply chains fixed and wage growth cooling, headline inflation around the world has fallen. It is back around 2% in many of the world’s largest economies (chart below).

In short, inflation is very close to being “just right.”

Chart 2: Inflation back near central bank targets

GDP growth just strong enough to avoid recession

The main tool central banks used to get inflation back under control was higher interest rates. Often, that slows the economy too much, leading to a recession, which many were worried about back in 2023.

However, the data shows that, although growth is slow in some places, most countries have avoided recession. Generally, countries seem to have achieved a so-called “soft landing.”

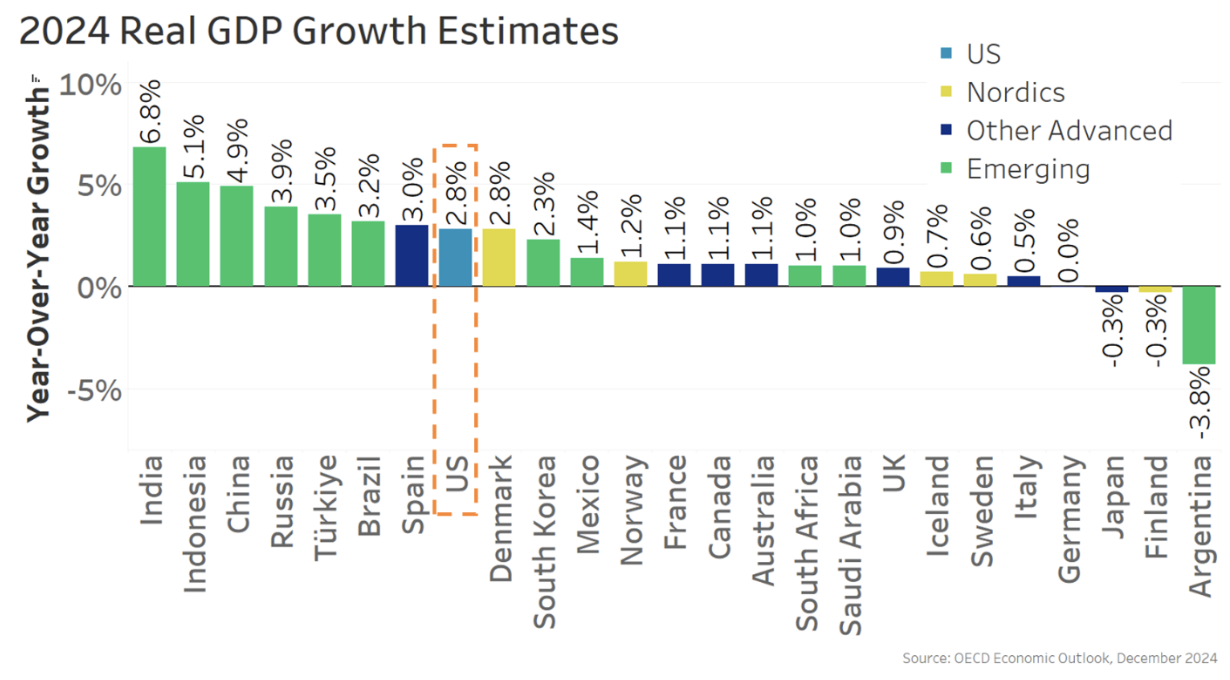

Chart 3: U.S. stands out for its strong growth among advanced economies in 2024

So, as we exit 2024, we have what is pretty close to a “Goldilocks” economy – not too hot, not too cold.

Interestingly, the U.S. has seen one of the strongest economies in 2024, where we have a 4.2% unemployment rate, 2.4% inflation rate, and are on pace for nearly 3% real GDP growth.

Rate cuts underway, with more expected in 2025, should help boost growth

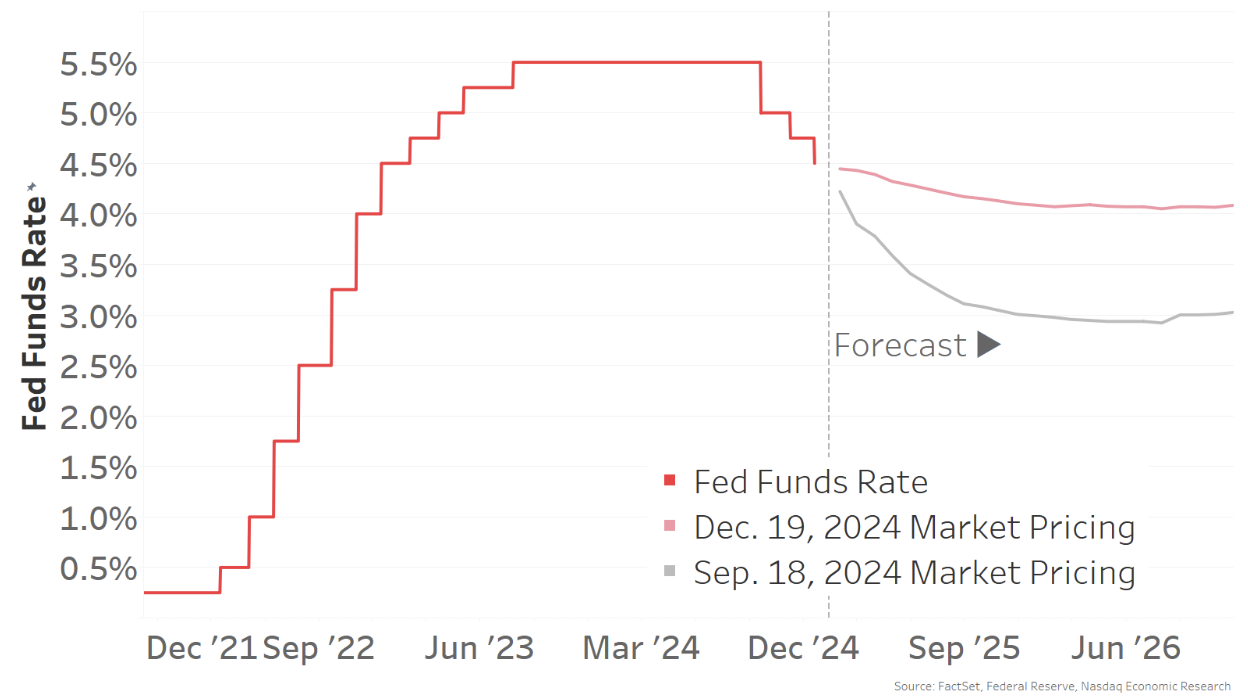

With inflation down and employment markets softer, central banks have already started to reduce rates. Based on the U.S. Fed’s own estimates, current short-term interest rates are still at levels that are “restrictive” – or above the neutral rate. As a result, rates are expected to fall more in 2025. The big question is how much.

Just three months ago, markets were pricing in a Fed funds rate of around 3.0% by the end of 2025 – a fall of around 1.5% from current levels.

By December, a lot had changed. Markets now only expect rates to fall to around 4.0%, and maybe not reach that level until 2026. In short, we are seeing rates staying higher-for-longer again. For interest rate-sensitive segments of the economy, that could affect investment and growth.

Chart 4: Interest rates are falling in most countries, with more cuts expected in 2025

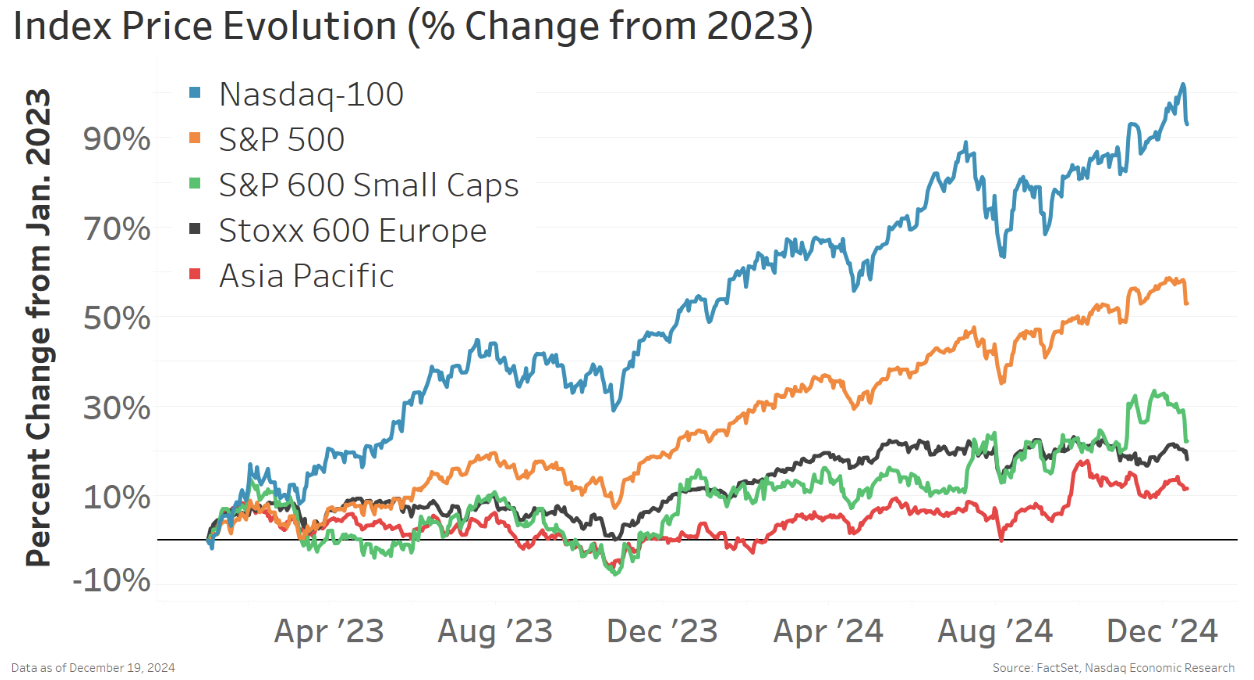

Global stock markets had a mostly good year in 2024

Overall, 2024 was a good year for stock markets. Many countries saw earnings recoveries, which, combined with lower interest rates, helped push stock valuations up.

However, returns in the U.S. large cap stocks – and especially for Nasdaq-100® stocks – were much higher than most other regions or market caps.

Chart 5: Most stock markets are up in 2024, but U.S. mega cap saw stronger returns

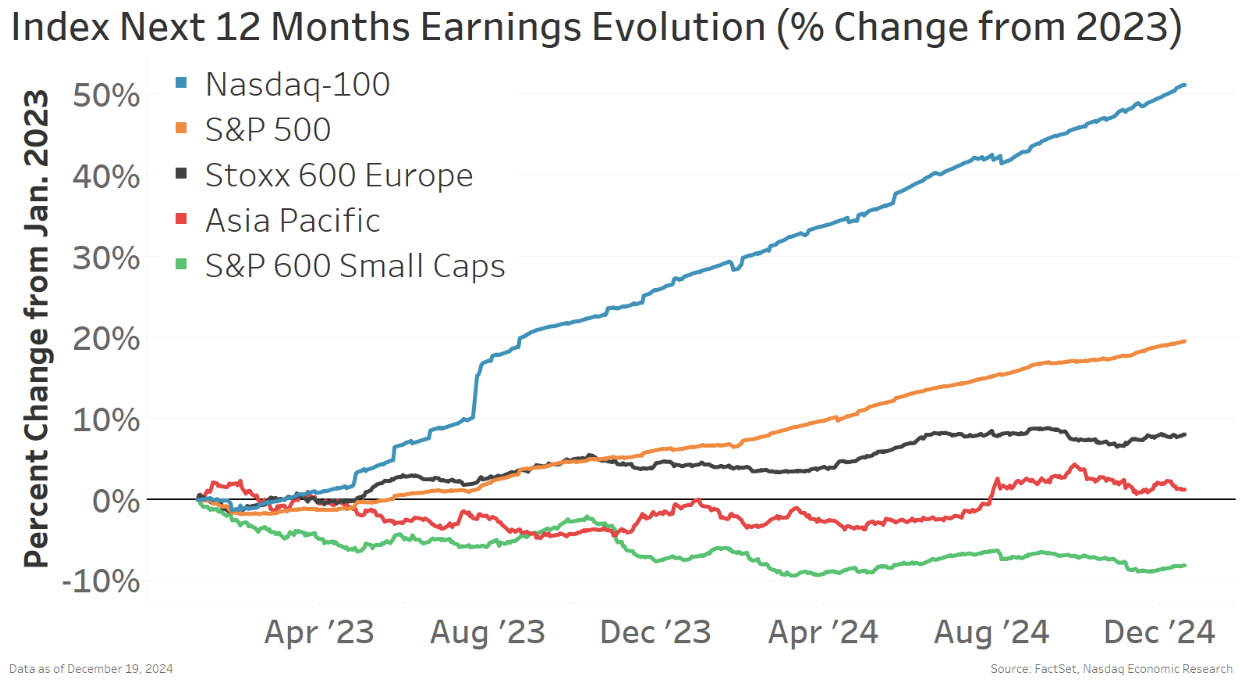

Interestingly, looking at earnings in the same indexes we see the same trends.

The outperformance of the Nasdaq-100® is supported by far stronger earnings growth. While U.S. small caps are mired in an earnings recession.

Chart 6: Earnings trends mirror stock returns

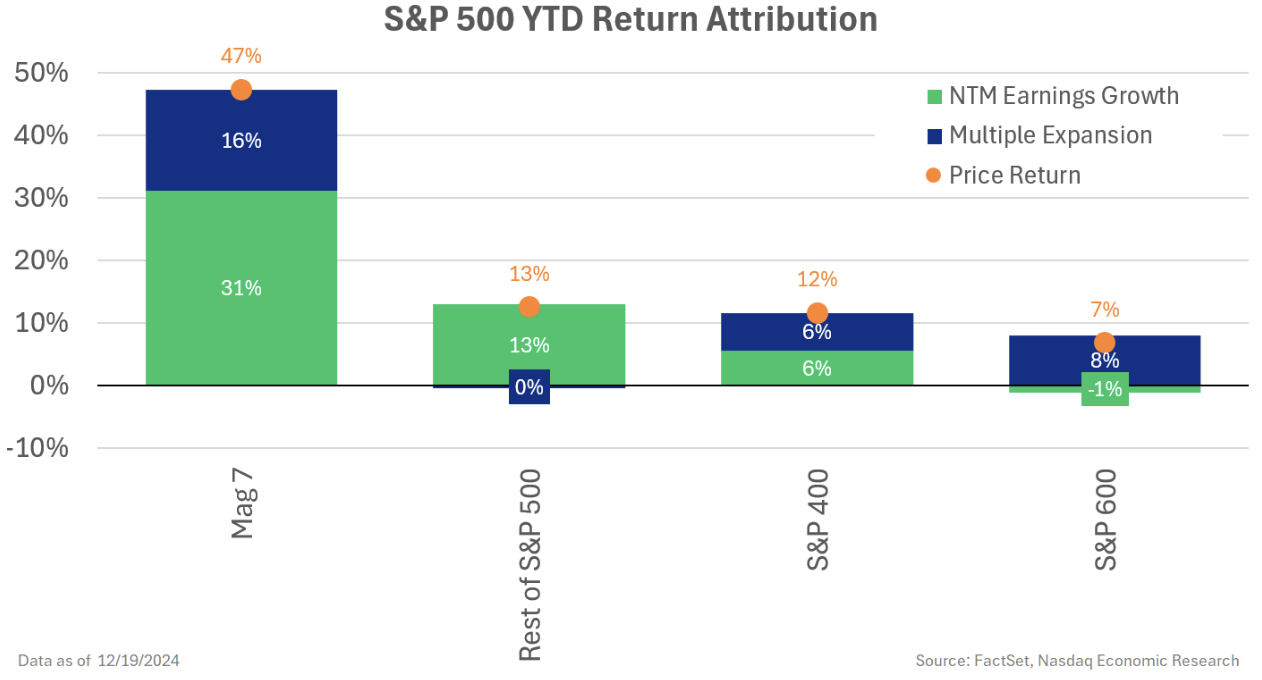

Taking a closer look at earnings in the large cap indexes, we see that earnings growth in the S&P 500 has been driven predominantly by the so called “Mag 7” stocks.

All those stocks are exposed to the spending on artificial intelligence, which some estimate is running well over $200 billion per year. Nvidia makes the GPU chips sought after for calibrating AI models. Amazon, Microsoft and Google all run cloud data centers, which are key to processing all the data, and Apple,Tesla and Meta are among the first movers using AI in their products.

Because all are Nasdaq listings, they make up an even larger proportion of the Nasdaq-100 Index® – helping the Nasdaq-100® outperform the broader S&P 500 index.

Chart 7: Large-cap earnings are driven by the Mag 7 stocks

Importantly though, as we have progressed through 2024, we have seen a broadening of the earnings recovery in the rest of the large cap stocks.

Lower rates would be good for small companies

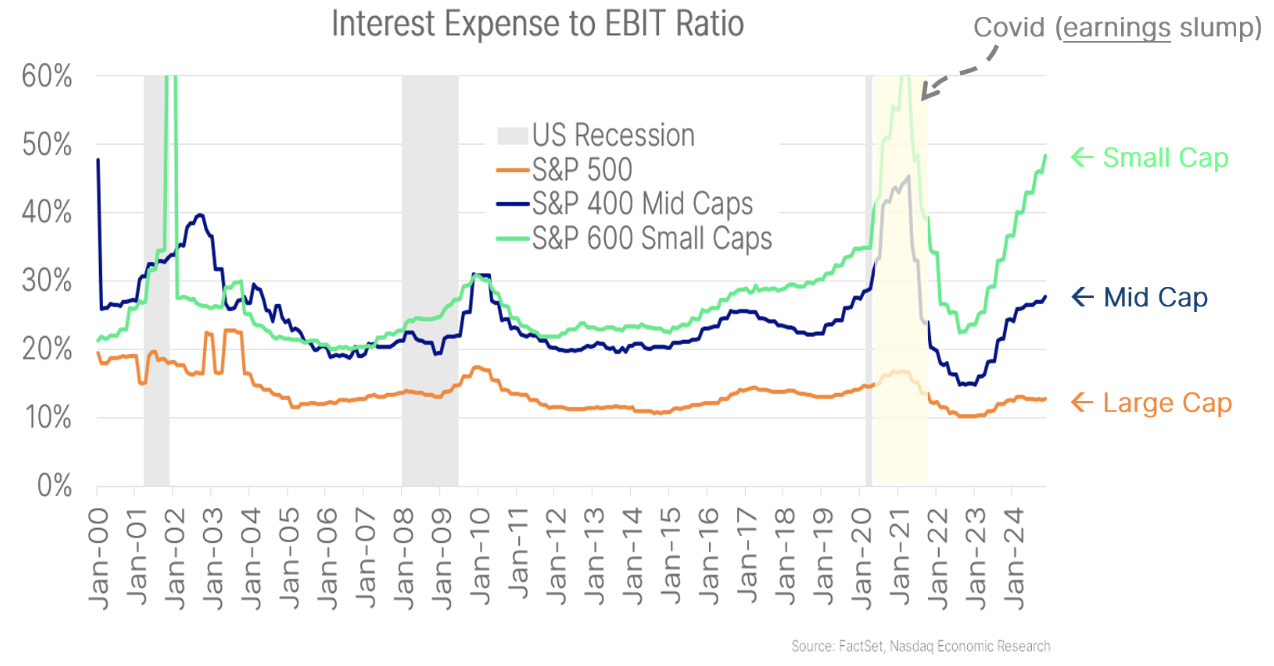

When we look at the difference between large-cap and small-cap stocks, one thing stands out. Interest expenses are reducing profits of small cap companies much more than for large-cap companies.

Some data shows that higher interest rates have especially impacted smaller companies, with interest expense/profit ratios at multidecade high levels. In contrast, the proportion of interest expense for large cap companies is near record low levels – and has hardly increased despite rising interest rates.

Chart 8: Interest rates are affecting small-cap companies much more than larger companies

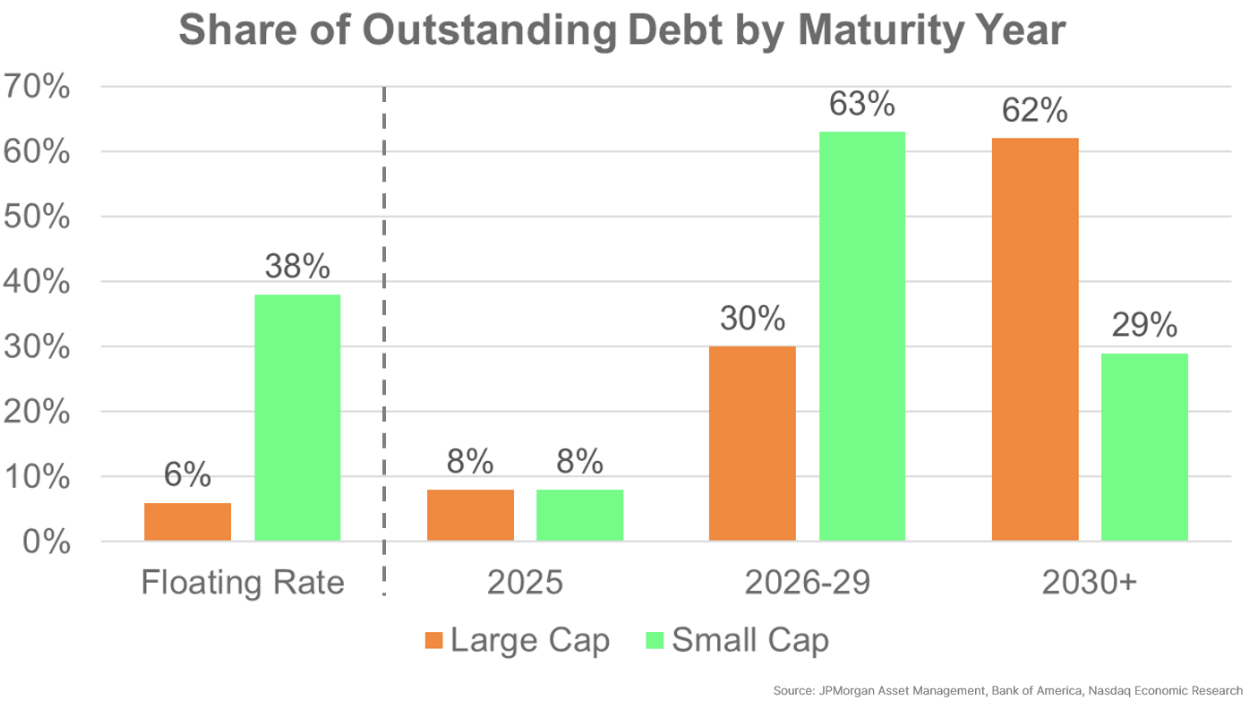

The different sensitivity to interest rates is supported by looking at company debt financing across market cap. We see that large-cap companies have very little floating rate debt, which has insulated them from Fed interest rate increases. In fact, large-cap companies seem to have fixed rates on the majority of their debt, at low rates, out to at least 2030.

In contrast, small-cap companies have around a third of their debt at floating rates, with a large proportion of fixed rate debt scheduled to refinance starting in 2026. Clearly, small-cap companies will be more impacted by rates staying higher-for-longer.

Chart 9: Small-cap companies are much more exposed to higher short-term interest rates

2025: No signs yet of consumer weakness

Overall, the reason the U.S. economy performed so well in 2024 was because the U.S. consumer remained strong. Real spending (adjusted for inflation) is up almost 15% compared to right before Covid. That’s a lot better than Europe, where real spending has barely increased.

Chart 10: U.S. consumer spending stands out among other advanced economies

A number of factors have helped maintain consumer spending growth in the U.S.

Firstly, after experiencing the Credit Crisis back in 2008, most U.S. households have now locked in long-term fixed mortgage rates. Just like large-cap companies, despite the Fed increasing official interest rates and new mortgage rates almost tripling, the average interest rate on outstanding mortgages barely increased – and remains around 4%. That has left more money in people’s pockets – and means monetary policy has had a more muted impact on consumers.

Secondly, with wage gains that started in the “Great Resignation,” and then broadened to include most workers, real wages have also grown. That, combined with strong employment and low risks of layoffs, has given the consumer the confidence to keep spending.

With interest rates higher, even savers are earning more income.

Finally, higher house prices have also left household balance sheets in a strong position. Recent data showing increases in home equity loans (HELOCs) suggest some might finally be tapping into debt markets, allowing spending to persist.

So far, there are few signs of weakness. Credit card debt, although at new highs, is relatively low as a proportion of income and household net assets. In fact, even the increase in unemployment (Chart 1) that the U.S. has seen is mostly due to more workers looking for jobs. Layoffs, which more typically lead into recessions, remain near multidecade low levels.

Chart 11: Low layoffs have helped consumers keep spending

2025: Strong underlying economy with a chance of uncertainty

There are a lot of positive signs for the U.S. economy and the stock market heading into 2025.

The consumer remains strong, thanks to robust household balance sheets and a strong job market.

Company earnings are recovering. Expected tax cuts and looser regulation in 2025 should help boost earnings, too. Although some uncertainty exists for companies that have to deal with higher longer-term interest rates, possible new tariffs and potential new labor shortages.

Looking at the bigger picture, further interest rate cuts, combined with tax cuts and net positive government spending, should keep the U.S. economy growing for at least another year. That should also be good for stocks.

Phil Mackintosh is Chief Economist at Nasdaq. Michael Normyle is U.S. Economist and Senior Director at Nasdaq.

Creating tomorrow’s markets today. Find out more about Nasdaq’s offerings to drive your business forward here.

Jim Toesis President and CEO of the Security Traders Association (STA).

Jim Toes

What was the highlight of 2024?

STA experienced several notable highlights in 2024. Of course, the most significant outcome of the year was the election results — after months of uncertainty, the stage is set for a new regulatory landscape and a new set of legislative priorities, which is a crucial development for our members regardless of their political views. For our part, STA saw a strong rebound in terms of our affiliate events, with approximately 75 in-person gatherings taking place throughout the year. These events ranged from smaller, community-focused efforts to larger, content-rich conferences, demonstrating our commitment to fostering engagement and dialogue within the industry. Another key achievement was our successful 91st Annual Market Structure Conference held in Orlando, which combined a productive program with a resort setting to provide both professional enrichment and networking opportunities. Finally, the launch of the STA Arizona Chapter marked an important milestone for the securities industry in the Southwest, underscoring our growing presence across the country and the increasing activity in emerging or non-traditional financial hubs.

What trends are getting underway that people may not know about but will be important?

There are a number of trends that will gain momentum in 2025, and our STA Advisory Committees on Retail Trading, Listed Options and ETFs are actively working to plot our next move on emerging regulatory priorities under the new administration. Come what may, we will ensure that our members remain well-informed and ready to adapt. In particular, the impact of new legislative committee appointments in the Senate and House of Representatives should not be underestimated. These appointments often play a crucial but underappreciated role in shaping market structure and regulatory priorities. One significant update is the appointment Arkansas Rep. French Hill, a former banker, as the next chair of the House Financial Services Committee. Beyond that, STA is also driving initiatives like the expansion of our Women in Finance committee, our Grassroots Giving program and emphasizing LinkedIn for communication and engagement.

What are your expectations for 2025?

As STA moves into 2025, expectations are high. We plan to leverage our core strengths—deep industry knowledge, a national footprint and a long history of bipartisan collaboration—to respond effectively to the changes brought by the new administration. Advocacy will remain a cornerstone of STA’s mission, with particular emphasis on addressing market challenges related to capital formation. We have expressed concerns about the SEC’s recent neglect of its responsibilities in this area and intend to bring this issue to the forefront. By focusing on these priorities, we aim to deliver continued value to our members and to the broader financial community.

London, 6 th January 2025 – The World Federation of Exchanges, the global industry association for exchanges and CCPs (The WFE), has published new research which analyses the link between stock market development and economic growth on a global scale.

The research analysed quarterly data from 36 countries over two decades (2003-2022).

Key findings

Short term analysis:

• There is a two-way influence between economic output growth and stock market capitalisation in the short term, but only for high-income countries.

• Low and middle-income countries experience a unidirectional relationship in the short term, where stock market capitalisation positively impacts economic growth, but not vice versa.

This means that low and middle-income country exchanges aren’t seeing a positive impact on their market capitalisation as a result of economic growth, though higher market capitalisation leads to higher economic growth. This reflects structural differences, such as lower savings rates and limited investment capacity, which inhibits the feedback loop from economic growth to stock market development.

• The low- and middle-income group experience a stronger response in output growth to changes in market capitalisation activity compared to high-income countries.

• A doubling of market capitalisation leads to an increase of over 0.4% in economic growth within two quarters for low- and middle-income countries.

This suggests there should be policy interventions aimed at stimulating market capitalisation as they will have a pronounced short-term impact on economic growth in low- and middle-income countries.

Long term analysis:

• Stock market capitalization generally promotes economic growth across all income groups, though the effect is much stronger in high-income countries than in low- and middle-income economies.

• In high-income countries, a 10% increase in stock market capitalization is associated with a 0.045% rise in long-term economic growth.

• The relationship in low- and middle-income countries is weaker, reflecting challenges such as underdeveloped financial systems and structural inefficiencies. However, growth in stock market capitalisation in low- and middle-income countries contributes a greater percentage to overall economic growth.

This shows that well-developed stock markets benefit high-income countries by enabling efficient savings and capital allocation, which fosters sustained economic growth.

Nandini Sukumar, CEO of the World Federation of Exchanges, said, “A growing stock exchange means a growing economy. The research shows that where high-income countries’ stock markets are struggling, regulators must take action to support them, so that they can ensure the continued contribution of this source of economic growth. On the other hand, low- and middle-income countries should focus on strengthening their stock markets to harness these growth benefits and support sustainable economic development. Policymakers must take heed of these findings and better tailor financial regulations and economic strategies to maximise the benefits stock markets bring.”

Commenting on the research findings Dr Pedro Gurrola-Perez, Head of Research at the WFE, said, “Weaker feedback loops from economic growth to stock market development are due to factors such as lower savings rates, limiting the capital available for investment in stock markets; limited investment capacity, reducing business’s ability and appetite to expand. In these environments, the lack of investor participation and limited business growth may inhibit the ability of economic growth to foster stock market development, and in turn, economic output. Policymakers, particularly in low- and middle-income countries, should therefore focus on strengthening their stock markets to harness these growth benefits and support sustainable economic development.”

Established in 1961, the WFE is the global industry association for exchanges and clearing houses. Headquartered in London, it represents over 250 market infrastructure providers, including standalone CCPs that are not part of exchange groups. Of our members, 37% are in Asia-Pacific, 44% in EMEA and 19% in the Americas. WFE’s 87 member CCPs and clearing services collectively ensure that risk takers post some $1.3 trillion (equivalent) of resources to back their positions, in the form of initial margin and default fund requirements. WFE exchanges, together with other exchanges feeding into our database, are home to over 51,000 listed companies, and the market capitalisation of these entities is over $110 trillion; around $140 trillion (EOB) in trading annually passes through WFE members (at end 2024).

The WFE is the definitive source for exchange-traded statistics and publishes over 350 market data indicators. Its free statistics database stretches back 49 years and provides information and insight into developments on global exchanges. The WFE works with standard-setters, policy makers, regulators and government organisations around the world to support and promote the development of fair, transparent, stable and efficient markets. The WFE shares regulatory authorities’ goals of ensuring the safety and soundness of the global financial system.

With extensive experience of developing and enforcing high standards of conduct, the WFE and its members support an orderly, secure, fair and transparent environment for investors; for companies that raise capital; and for all who deal with financial risk. We seek outcomes that maximise the common good, consumer confidence and economic growth. And we engage with policy makers and regulators in an open, collaborative way, reflecting the central, public role that exchanges and CCPs play in a globally integrated financial system.

By Bryan Dougherty, Head of Product and Technology, Arcesium

Regulators are not backing down on demands that firms modernize disclosure models and enhance data governance practices. A prime example of this is the $900 million wire transfer mistake made by Citibank in 2020, which resulted in the Office of the Comptroller of the Currency (OCC) slapping the financial institution with a $400 million civil money penalty. Old, defective software was identified as the culprit of this costly error and Citi assured regulators it would improve risk management, data governance, and internal controls. However, just four years later, the institution was once again handed a $135 million dollar fine for their inadequate remediation efforts in addressing data quality management issues.

As financial institutions race to keep up with the pace of digitalization and automation, regulators like the SEC, FINRA, and others are hot on their tails, ensuring their rulemaking remains relevant to today’s rapidly evolving market landscape.

For both buy-side and sell-side firms to stay ahead and remain on the right side of these regulations, they must answer the call to modernize their disclosure models, operate using clean and accurate data, and enact meticulous data governance standards that lead to airtight compliance and reporting. Institutions that move to transform data management processes will be able to manage regulatory risk, enhance operational efficiency, swiftly meet investor demands, and achieve better returns.

The dynamic backdrop of regulatory mandates

The monumental swing in attention by regulatory bodies towards reporting and disclosure methods has been a long time coming. As technology has raced ahead, financial institutions are pushed to capitalize on machine learning, automation, and AI, to build efficiencies and keep up with the competition. However, as markets continue to grow in complexity, spanning across multiple asset classes, venues, and regions, investors today conduct business under a cloud of potential risks. These range from liquidity, compliance hurdles, trade manipulation, and operational vulnerabilities. Regulators view these shifts in the market as a mandate for greater oversight of an industry in flux, seeking to protect investors and, ultimately, the entire financial system.

More oversight means more accountability; more accountability means extensive reporting and disclosure rules. Regulators have made forceful strides with new proposals and intensified enforcement of rules like Regulation Best Interest, the financial recordkeeping and communications law, the revised Form PF, and the recently implemented T+1 rule, which requires trades to be settled one day earlier on the next business day, instead of two days post-trade. Every rule demands heightened accuracy and promptness of financial reporting and disclosure, and both buy-side and sell-side firms need to prepare.

Outdated models unearth the risk of untrustworthy data

To avoid regulatory scrutiny, potential fines, and reputational damage, firms need to address modernizing their disclosure models and tech infrastructure, as was true in the Citibank case.

Firms’ legacy data management platforms and traditional manual spreadsheet processes are unable to properly ingest data from market data vendors, service providers, third-party applications, cloud marketplaces, and internal applications such as accounting, CRM, risk tools, and internal databases. This data fragmentation causes the connection between middle- and back-office operations and front-office aspirations to become disjointed. A firm that relies on bad, inaccurate, and untrustworthy data is flying blind with overly complex workflows, will be slow to incorporate new strategies or asset classes, and will be unable to make informed portfolio decisions. Firms who want to merge into popular private debt vehicles or deploy advanced blended private-public strategies find vexing operational obstacles. They cannot efficiently meet all investor and regulator reporting demands for performance, attribution, and risk. Moreover, disparate datasets lead to costly errors, leaving compliance departments’ reporting and disclosure practices hung out to dry.

Data governance: The backbone of risk control

Updated infrastructure and superior data quality are some of the key steps in meeting regulators and investors’ demands. However, for firms to keep up with evolving rule changes, be audit-ready, and sustain long-term success in meeting reporting and disclosure regulations, they must pursue rigorous data governance and risk management control standards. Citi’s $135 million dollar penalty is a not-so-subtle message from regulators to remediate data quality management and governance. Institutions that formalize clear processes around reporting and disclosure methods that ensure data integrity, accountability, and compliance will be more agile in flagging and rapidly correcting mistakes and in adapting to changing rules in the future.

Automation is the missing piece to efficient and accurate reporting

When faced with increasing regulations, firms can only keep up with expanding reporting requirements if they lean on automation tools for help. Automation can support teams in streamlining data collection and calculation processes, reducing manual errors, and ensuring it’s done efficiently. Teams prioritizing their automation and data processes will be miles ahead in meeting increased reporting demands with greater ease and precision, lessening the chance of costly fines.

Building a golden thread of data

Financial firms should join regulators in their quest for better, more robust reporting. And this is not merely to follow rules, but also to drive alpha. However, driving alpha is no easy task, especially when the investing community is experiencing a state of data explosion and the rise in popularity of opaque and multi-asset-class strategies. The upsurge of less data-transparent private markets continues with an AUM totaling $13.1 trillion, a 20% yearly growth since 2018. Multi-asset strategies have led to asset-class convergence, with its correlation of asset classes causing significant data complexity. The post-trade operations teams who continue to be tasked with manually pulling this raw data from spreadsheets to validate P&L calculation, monitor timestamps, verify trade allocations, and handle transaction reporting are at a disadvantage, burning time and making unavoidable errors.

It’s vital for firms to operate from a single golden thread of investment lifecycle data that is validated and organized. Data management technology should speak directly to the unique needs of modern trading, enabling firms to pull precise information from disparate datasets, as well as the aggregation of holdings, performance, cash flows, risk analytics, and reporting data. Firms must have modernized systems in place that possess the ability to comprehend and interpret data across different asset classes and jurisdictions. These tools provide a crystal-clear picture to their analysts, investors, and regulators alike.

A triple competitive edge: modernization, quality, and governance

In fiscal year 2025, the SEC says it will continue to encourage investor testing on both existing and proposed disclosures to retail investors; and it will advocate for innovative, and more investor focused approaches to disclosure. The procrastination runway in financial services for digital transformation has run out. The SEC stated in its 2025 exam priorities that it will review RIAs and RICs’ compliance programs, including reviewing their consistency of portfolio management practices and disclosures, and issues associated with market volatility.

To have any hope of building secure risk controls, fully compliant reporting, and innovative disclosures, both buy-side and sell-side firms will have no choice but to move away from outdated manual processes and upgrade outdated and inefficient tech infrastructure. Data governance approaches that ensure financial data is standardized, interoperable, and effectively managed to meet evolving regulatory expectations is a prerequisite to growing AUM and staying competitive, now and down the road. The integration of advanced data management systems that operate on clean, organized, and accurate investment lifecycle data is no longer a cost center; it’s a profit center, and a lucrative one. The benefits are extensive, from providing the ability to make informed decisions and facilitate operations to launching new lines of business, as well as meeting regulatory compliance requisites and strengthening investor confidence – ultimately, lining up the path for both short- and long-term growth.

Stephen Cavoli is Global Head of Execution Services at Virtu Financial.

Stephen Cavoli

What were the key theme(s) for your business in 2024?

Every successful firm begins and ends with a great product supported by great people. Our key themes remain consistent: We prioritize client needs as the foundation of product development, ensuring the solutions we build align with client workflows and expectations. Wherever possible, these solutions are global and multi-asset, covering the entire trade life cycle.

The key themes varied by region. In APAC, the focus was on India, where we developed collocated trading infrastructure to address client requirements and support the market’s rapid growth and evolving demands. In MENA, we refined algorithms to align with the region’s unique market structure and advanced the launch of a block trading venue to support institutions and large trade executions.

The key themes also varied by product. For our Triton EMS offering, there was a large focus on meeting clients’ needs for multi-asset capabilities within the EMS and deepening integration with third-party systems. The key themes for our data analytics platform were strengthening multi-asset functionality including the addition of TCA for Fixed Income Derivatives and enhancing API access to enable clients to bring trading analytics “in-house.” We also released a more granular pre- and post-trade transaction cost models (SCE and DyCE) in response to client requests. Our global FIX Network expanded by connecting with new banks, brokers, and dealers, as we focus on delivering FIX Network services that simplify client workflows and boost efficiency.

What trends are getting underway that people may not know about but will be important?

We’re seeing more and more desks adopt a single trading infrastructure. This trend is a long-time coming and it’s just begun to tip. As desks migrate to a unified trading infrastructure that supports the entire trade life cycle across all asset classes globally, it simplifies operations, reduces costs, and ensures consistency in execution and post-trade services.

We’re also seen a resurgence of demand for new sources of liquidity. Specifically, clients want algos that identify and interact with these incremental liquidity sources in sophisticated and transparent ways.

What are your clients’ pain points, and how have they changed from one year ago?

Clients are increasingly focused on getting the most out of their commission dollars through quality alpha generating research, navigating global regulations and workflows, optimizing commission spend, demanding better value and cost transparency. We’ve seen more clients embrace our global, multi-asset trading and analytics platform which allows clients to streamline external relationships and internal workflows, saving time, reducing operational risk, and increasing wallet purchasing power.

The demand for intelligent and transparent liquidity access has evolved. Previously, the focus was on static routing and spread positioning. Now, clients demand sophisticated routing decisions and access to unique liquidity pools. Achieving this requires a trading infrastructure capable of consuming vast amounts of market data and making real-time decisions based on specific trading conditions. Brokers must now explain algorithmic decisions with transparency and a clear decision-making rationale. Descriptive statistics are no longer sufficient; clients expect causal analysis to justify order routing choices.

Related to the evolving demand for intelligent and transparent execution and workflow tools, as trading across asset classes becomes increasingly electronic, clients’ requests for more tailored support engagement has increased. Tighter collaboration with clients is mandatory to properly understand their desired outcomes which is highly correlated to being able to solve real-time issues.

Jason Paltrowitz is Executive Vice President of Corporate Services at OTC Markets Group.

Jason Paltrowitz

What were the key theme(s) for your business in 2024?

In 2024, OTC Markets Group focused on three major themes to drive growth, enhance market transparency, and better serve global investors:

Continued Growth in International Business: OTC Markets Group operates the largest U.S. stock market for non-U.S. equities, facilitating trading for international companies seeking access to U.S. investors. This year, 92% of our total trading volume came from non-U.S. equities, with 79% of that volume attributed to companies with market caps exceeding $1 billion. Reflecting the strong demand for cross-border investment opportunities, we launched two significant initiatives to enhance accessibility and flexibility for global investors.

First, we launched OTC Overnight, an innovative “overnight trading” service, enabling investors in any time zone to access securities on our markets and react to international news in real-time. Second, we launched the MOON ATS, an alternative trading system designed to provide a seamless trading experience for NMS listed securities. Both OTC Overnight and MOON ATS underscore our commitment to building infrastructure that empowers global investors while streamlining access to U.S. markets. These advancements strengthen our role as a bridge between U.S. investors and international companies.

Regulatory Reform and Investor Protection: A key focus in 2024 was advancing regulatory initiatives to improve market transparency and investor protections. We introduced OTCID, a new identification framework designed to enhance accountability, improve compliance, and help investors make better-informed decisions. OTCID represents a significant milestone in creating a more transparent market for all participants.

Addressing Risks in Low-Priced Securities: OTC Markets Group prioritized education of the risks associated with low-priced securities, including exchange-listed “penny stocks,” which often pose challenges for retail investors due to their volatility and potential for fraud. We supported industry efforts to crack down on risky practices in the micro- and small-cap markets. By promoting investor education, enhanced standards, and oversight, we aim to protect investors and uphold market integrity.

What was the highlight of 2024?

Several key milestones defined OTC Markets Group’s success in 2024:

Launch of Overnight Trading: We introduced overnight trading, enabling investors to trade international securities outside traditional market hours. This initiative provides greater flexibility for global investors and enhances access to international markets.

Announcement of OTCID: The rollout of OTCID marked a major advancement in improving market structure. This new identifier will enhance transparency and accountability, strengthening trust and confidence among market participants.

Growth in QX and QB Markets, Including Expansion into Korea: Our OTCQX and OTCQB markets continued to experience robust growth, driven by strong demand from international and growth-stage companies. Notably, we expanded our global reach by facilitating new listings from South Korea, further broadening the opportunities available to U.S. investors.

Who were the most important/influential people at your firm in 2024?

While I am proud to have contributed to our success, the accomplishments of 2024 are a testament to the exceptional teams across OTC Markets Group. From our leadership team to those driving initiatives like the launch of OTCID, overnight trading, and the growth of our OTCQX and OTCQB markets, it has been a collective effort. Their expertise, dedication, and innovative thinking have been instrumental in executing our strategic priorities and delivering value to investors and companies globally.

What are your expectations for 2025?

Looking ahead to 2025, OTC Markets Group is focused on deepening global partnerships, expanding investor access, and enhancing market infrastructure:

“List Local, Trade Global” Growth We are seeing growing interest from non-U.S. exchanges and companies seeking to leverage OTC Markets Group’s platform to gain access to U.S. investors while remaining listed on their local exchanges. A notable trend is the continued discount in valuations of non-U.S. equity markets, particularly in regions like the UK, which presents compelling opportunities for U.S. investors to diversify their portfolios.

Increased Engagement Through OTCID As OTCID rolls out more broadly, we anticipate greater engagement from companies, brokers, and market participants. OTCID will help enhance transparency and governance while providing investors with clearer, more reliable information about the securities they are trading.

Solidifying Our Leadership in Non-U.S. Equities With growing interest from Asian retail investors seeking trading access to the world’s leading companies, OTC Markets Group is well-positioned to strengthen its leadership as the platform for trading international equities. This growing demand reflects the global investor appetite for diversified, cross-border investment opportunities.

Anthony Denier is Group President and US CEO of Webull.

Anthony Denier

What were the key theme(s) for your business in 2024?

In 2024, Webull saw an increased user base from retail investors across the globe. The group now serves over 20 million registered users in 15 regions, offering investment strategies that seamlessly integrate market data and information, a user community, and investor education resources. Additionally, we have seen retail investors putting their cash to work after previously stockpiling in high APY products. The high interest rate environment led to large amounts of uninvested cash. As interest rates come down, retail investors are moving cash back into equities and stimulating market activity.

What was the highlight of 2024?

The highlight of 2024 for me was retail’s embrace of 24 hour securities trading. This is signaling the continued evolution of retail investors. Just a few years ago, commission free trading for retail investors was unheard of, now it is common place. The same goes for fractional trading, and now 24/5. It is new and disruptive, but will become the standard. 24 hour trading is a natural progression of retail investor demands and expectations, which the industry is now embracing. We are thrilled that Webull users feel confident to trade in an overnight setting, outside of market hours. As the industry continues to move away from legacy, back office systems and transitions to more technology focused solutions, it will allow for more trading hours and continued rapid evolution.

What are your expectations for 2025?

Strong markets will fuel innovation and adoption of new products and technologies like AI and crypto for retail investors. A new administration comes with opportunities for change and growth and markets have been receptive to the election outcome. Retail investors will continue to ride this momentum and further diversify their portfolios based on the next iteration of products and tools available to them. I look forward to what 2025 will bring.

The Era of Data Modernization, Quality and Governance is Here

By Bryan Dougherty, Head of Product and Technology, Arcesium

Regulators are not backing down on demands that firms modernize disclosure models and enhance data governance practices. A prime example of this is the $900 million wire transfer mistake made by Citibank in 2020, which resulted in the Office of the Comptroller of the Currency (OCC) slapping the financial institution with a $400 million civil money penalty. Old, defective software was identified as the culprit of this costly error and Citi assured regulators it would improve risk management, data governance, and internal controls. However, just four years later, the institution was once again handed a $135 million dollar fine for their inadequate remediation efforts in addressing data quality management issues.

As financial institutions race to keep up with the pace of digitalization and automation, regulators like the SEC, FINRA, and others are hot on their tails, ensuring their rulemaking remains relevant to today’s rapidly evolving market landscape.

For both buy-side and sell-side firms to stay ahead and remain on the right side of these regulations, they must answer the call to modernize their disclosure models, operate using clean and accurate data, and enact meticulous data governance standards that lead to airtight compliance and reporting. Institutions that move to transform data management processes will be able to manage regulatory risk, enhance operational efficiency, swiftly meet investor demands, and achieve better returns.

The dynamic backdrop of regulatory mandates

The monumental swing in attention by regulatory bodies towards reporting and disclosure methods has been a long time coming. As technology has raced ahead, financial institutions are pushed to capitalize on machine learning, automation, and AI, to build efficiencies and keep up with the competition. However, as markets continue to grow in complexity, spanning across multiple asset classes, venues, and regions, investors today conduct business under a cloud of potential risks. These range from liquidity, compliance hurdles, trade manipulation, and operational vulnerabilities. Regulators view these shifts in the market as a mandate for greater oversight of an industry in flux, seeking to protect investors and, ultimately, the entire financial system.

More oversight means more accountability; more accountability means extensive reporting and disclosure rules. Regulators have made forceful strides with new proposals and intensified enforcement of rules like Regulation Best Interest, the financial recordkeeping and communications law, the revised Form PF, and the recently implemented T+1 rule, which requires trades to be settled one day earlier on the next business day, instead of two days post-trade. Every rule demands heightened accuracy and promptness of financial reporting and disclosure, and both buy-side and sell-side firms need to prepare.

Outdated models unearth the risk of untrustworthy data

To avoid regulatory scrutiny, potential fines, and reputational damage, firms need to address modernizing their disclosure models and tech infrastructure, as was true in the Citibank case.

Firms’ legacy data management platforms and traditional manual spreadsheet processes are unable to properly ingest data from market data vendors, service providers, third-party applications, cloud marketplaces, and internal applications such as accounting, CRM, risk tools, and internal databases. This data fragmentation causes the connection between middle- and back-office operations and front-office aspirations to become disjointed. A firm that relies on bad, inaccurate, and untrustworthy data is flying blind with overly complex workflows, will be slow to incorporate new strategies or asset classes, and will be unable to make informed portfolio decisions. Firms who want to merge into popular private debt vehicles or deploy advanced blended private-public strategies find vexing operational obstacles. They cannot efficiently meet all investor and regulator reporting demands for performance, attribution, and risk. Moreover, disparate datasets lead to costly errors, leaving compliance departments’ reporting and disclosure practices hung out to dry.

Data governance: The backbone of risk control

Updated infrastructure and superior data quality are some of the key steps in meeting regulators and investors’ demands. However, for firms to keep up with evolving rule changes, be audit-ready, and sustain long-term success in meeting reporting and disclosure regulations, they must pursue rigorous data governance and risk management control standards. Citi’s $135 million dollar penalty is a not-so-subtle message from regulators to remediate data quality management and governance. Institutions that formalize clear processes around reporting and disclosure methods that ensure data integrity, accountability, and compliance will be more agile in flagging and rapidly correcting mistakes and in adapting to changing rules in the future.

Automation is the missing piece to efficient and accurate reporting

When faced with increasing regulations, firms can only keep up with expanding reporting requirements if they lean on automation tools for help. Automation can support teams in streamlining data collection and calculation processes, reducing manual errors, and ensuring it’s done efficiently. Teams prioritizing their automation and data processes will be miles ahead in meeting increased reporting demands with greater ease and precision, lessening the chance of costly fines.

Building a golden thread of data

Financial firms should join regulators in their quest for better, more robust reporting. And this is not merely to follow rules, but also to drive alpha. However, driving alpha is no easy task, especially when the investing community is experiencing a state of data explosion and the rise in popularity of opaque and multi-asset-class strategies. The upsurge of less data-transparent private markets continues with an AUM totaling $13.1 trillion, a 20% yearly growth since 2018. Multi-asset strategies have led to asset-class convergence, with its correlation of asset classes causing significant data complexity. The post-trade operations teams who continue to be tasked with manually pulling this raw data from spreadsheets to validate P&L calculation, monitor timestamps, verify trade allocations, and handle transaction reporting are at a disadvantage, burning time and making unavoidable errors.

It’s vital for firms to operate from a single golden thread of investment lifecycle data that is validated and organized. Data management technology should speak directly to the unique needs of modern trading, enabling firms to pull precise information from disparate datasets, as well as the aggregation of holdings, performance, cash flows, risk analytics, and reporting data. Firms must have modernized systems in place that possess the ability to comprehend and interpret data across different asset classes and jurisdictions. These tools provide a crystal-clear picture to their analysts, investors, and regulators alike.

A triple competitive edge: modernization, quality, and governance

In fiscal year 2025, the SEC says it will continue to encourage investor testing on both existing and proposed disclosures to retail investors; and it will advocate for innovative, and more investor focused approaches to disclosure. The procrastination runway in financial services for digital transformation has run out. The SEC stated in its 2025 exam priorities that it will review RIAs and RICs’ compliance programs, including reviewing their consistency of portfolio management practices and disclosures, and issues associated with market volatility.

To have any hope of building secure risk controls, fully compliant reporting, and innovative disclosures, both buy-side and sell-side firms will have no choice but to move away from outdated manual processes and upgrade outdated and inefficient tech infrastructure. Data governance approaches that ensure financial data is standardized, interoperable, and effectively managed to meet evolving regulatory expectations is a prerequisite to growing AUM and staying competitive, now and down the road. The integration of advanced data management systems that operate on clean, organized, and accurate investment lifecycle data is no longer a cost center; it’s a profit center, and a lucrative one. The benefits are extensive, from providing the ability to make informed decisions and facilitate operations to launching new lines of business, as well as meeting regulatory compliance requisites and strengthening investor confidence – ultimately, lining up the path for both short- and long-term growth.