Trading limits have come into the focus of senior management teams across the sell-side, according to the Q4 2024 Sell-Side Execution Management Insight report by Acuiti.

A major fine from UK regulators has changed approaches across the sell-side, the report noted.

“This new focus on trading limits has shone a light on issues such as the lack of a central limits system and lack of clarity on how execution limits should be calculated,” the report added.

Banks operate their own models for trading limits and determining them for a client is often a nuanced exercise that involves the desk’s accumulated knowledge about their clients’ needs and strategies, according to the report.

For futures desks, trading limit calibration was identified as a high or urgent priority by 61% of the network.

Network members report that improving pre-trade risk analysis is an important part of these reviews.

Acuiti said that give-up arrangements are also emerging as an item of particular attention within the trading limits discussion.

According to the findings, most of the network reported calculating client futures trading limits on a product-by-product basis.

“This approach requires extensive analysis of each product, considering factors such as the order book for that product, the algos used to trade it its IM and other aspects of market structure,” the report said.

The report stressed that “explaining the nuance and minutiae of trading limit calculations to senior management and regulators can be a time-consuming exercise”.

According to Acuiti, if senior management teams have the technical knowledge or experience of working an execution desk, the process is much easier, however, over a third of the network cited it as a major inconvenience.

The report also covered the rising demand for commodity futures, India’s Gift City, the re-bundling of execution and research and the outlook for the remainder of 2024.

The report is based on a survey of the Acuiti Sell-Side Execution Network, a group of over 300 senior executives at banks and brokers across the global market.

Each quarter members of the network input topics and questions into the survey with the responses aggregated into this report.

Interactive Brokers (Nasdaq: IBKR), an automated global electronic broker, announced the success of its ForecastEx prediction market. Since its launch on October 4, 2024, ForecastEx has a total volume of over USD 560 million in presidential election contracts traded as of midday on November 6, 2024, with no technical issues reported.

Key Highlights:

ForecastEx Performance: ForecastEx Election Contracts proved to be a good predictor of election outcomes offering publicly visible prices which clarify real-time sentiment and bring accountability and transparency to a topic.

Future of Prediction Markets: Interactive Brokers sees prediction markets like ForecastEx becoming valuable tools in the coming years, offering unique data and insights. Beyond elections, IBKR’s ForecastTrader provides contracts on economic indicators, environmental factors, and government-related issues.

Steve Sanders, EVP of Marketing and Product Development at Interactive Brokers, noted, “Since investors must commit capital to express their conviction, they are engaged and educated about a subject. ForecastEx delivered highly predictive, real-time data to both investors and the broader market.”

On election night, Interactive Brokers also achieved record overnight trading volumes, including:

US Stocks: 188,168 trades

US Derivatives: 161,742 trades

Total Overnight Trades: 349,910

This occurred from 8:00 pm to 4:00 am Eastern on US markets and represents a huge increase over normal overnight trading.

By Bob Cioffi, Global Head of Equities Product Management, ION

The equities trading landscape has taken a dynamic turn over the past few years. While the continued dominance of low-touch, algorithmic trading has accelerated the speed of activity, the rise of alternative trading venues worldwide has unlocked a wider range of options and opportunities.

Firms are feeling the pressure as a result. While buy-side businesses jostle for access to as many markets as possible to avoid missing out on liquidity, sell-side firms are competing to help deliver on those ambitions. However, both are struggling to keep up with the pace of change.

The market needs more agility and connectivity to manage greater volumes and demands. But the question of who takes ownership for this innovation – and bears the cost – is more complex. With more market players than ever before, firms, venues, and technology providers need to work out how to share this burden to reap the collective benefit.

New competitive dynamics

Across the equities market, choice and competition among trading venues is ramping up.

New, alternative trading venues have been challenging traditional exchanges for some time. Both are experimenting with new functionalities and order books – auction, dark, lit, and conditional – to differentiate themselves as the go-to platform for clients. In Europe, the London Stock Exchange (LSE) acquired Turquoise to draw liquidity back in response to post-MiFID liquidity fragmentation, while Euronext has grown by acquiring exchanges in Dublin, Oslo, and Milan.

Less typical market players have also entered the fray to challenge the primary exchanges. These range from banks creating their own trading venues, such as UBS’ MTF and Goldman Sachs’ MTF (SIGMA X), to brand new exchanges such as Artex, which offers tokenized art funds as a new investment opportunity and allows museums to trade digital asset securities like equities. The rapid growth of IntelligentCross, an alternative trading system (ATS) is another good example.

In a fragmented landscape where multiple venues offer free market data and connectivity with prominent liquidity providers, horizontal differentiation – exchanges offering different types of products or services to cater to different market segments – is increasingly common. We are at a point where no single venue can serve the interests of all investors.

Pressure on the system

It’s common for firms to want to “try before they buy” with access to new venues in the market. But building the technology to create fast access in this way is costly – both in time and resources.

For sell-side businesses to deliver best execution for their clients, the cost of connecting to every available venue currently outweighs the benefits. This leads most to opt for selective connections and rely on broker services. For buy-side firms and end-users deciding which markets they would like to access and how, these different approaches to connectivity will continue to shape their decisions, especially as different types of trading venues evolve. Naturally, technology providers are under pressure from all angles to build and monetize a new era of market infrastructure: solutions that can support connectivity to new venues, and therefore help all parties achieve their goals.

As a rule, greater competition is an economic good. It moves the market forward, breeds innovation, and results in lower costs. But key industry questions – such as who should take the lead in modernising market infrastructure to meet abundant modern connectivity needs – make reaching a verdict more difficult.

Addressing the challenge

As venues and order types grow in number, the degree of overhead in today’s market is significant – and the pace of change is fast. The question is how the market can innovate to keep up at a time of such rapid development.

Traditional processes for securing connectivity such as the manual configuration of connections and the lengthy onboarding of new clients are no longer quick or adequately responsive to meet needs. Technology firms need a way to work with new venues and exchanges to meet the needs of market participants.

At the same time, the growing trend of consolidation across exchanges in terms of ownership – for instance, the widespread adoption of Nasdaq’s technology – is also helping exchanges to take a big leap in terms of capabilities and offerings. Alongside the opportunity for new technology markets to provide much-needed common interfaces between different venues, a broader shift towards efficiency and scalability is already unfolding through consolidation.

Looking to the future

As we move ahead, it is through a collaborative effort that the market can address the challenge of funding new demands for innovation. With liquidity and best execution at stake, market connectivity is more important than ever. This bid for more options and flexibility is a prime opportunity to create a more resilient, agile market structure that can support the demands and direction of modern trading.

While the metaverse is being used and experimented with in a number of ways by financial institutions, it is an evolving technology with both potential benefits and risks that need to be better understood, according to Haimera Workie, Vice President and Head of OFI at FINRA.

The recent FINRA’s report, The Metaverse and the Implications for the Securities Industry, is intended to raise awareness among FINRA member firms and the broader securities industry by providing an overview of how developments related to the metaverse may impact business models and processes.

Haimera Workie

While the true implications of the metaverse may not be known for years, the report analyzes potential applications, use cases and challenges for member firms and notes certain regulatory considerations.

The report notes that the metaverse includes virtual worlds that are immersive, interactive and may be experienced in new ways through technological developments in hardware and software.

While the gaming industry has long been active in the metaverse, the report highlights that financial institutions have increasingly been exploring the metaverse to engage with the next generation of customers and to enhance their operations.

“A segment of financial institutions, including broker-dealers, are actively experimenting with incorporating the metaverse and its immersive technologies,” according to the report.

These developments prompted FINRA’s Office of Financial Innovation (OFI), which is part of the Office of Regulatory, Economics and Market Analysis, to launch the research initiative.

The report expands on the following potential metaverse-related use cases that FINRA members and related financial markets are considering or exploring: Data visualization; Virtual trading; Digital twins and industrial metaverse; Payments; Training and collaboration; Investor education; and Customer solicitation and service.

The report also delves into the challenges that firms may wish to consider as they explore applications on the metaverse or implement a metaverse strategy, including resource needs, data privacy and protection, and cybersecurity.

he report notes that member firms should also be mindful of the potential implications to their regulatory obligations as they consider whether to incorporate the metaverse into their internal systems and processes or use this technology within product offerings.

The specific rules applicable to member firms’ use of the metaverse will vary but will ultimately depend on how member firms deploy the technology, the report says. FINRA’s rules, which are intended to be technology neutral, continue to apply if member firms use the metaverse in the course of their businesses, just as they apply when member firms use any other technology or tool.

FINRA is seeking comments from firms, market participants and others currently exploring the metaverse. Comments are requested by March 14, 2025.

“We look forward to continuing to have an open dialogue with industry stakeholders to better understand the impact the metaverse could have on FINRA members and investors,” Workie said.

How are firms changing their data management strategies to improve investment operations and what is the increasingly relevant role of Artificial Intelligence (AI)?

In a recent Markets Mediawebinar, Duncan Cooper, Chief Data Officer at Northern Trust Asset Servicing, Miguel Castaneda, Partner at private markets advisory firm Alpha Alternatives (formerly Lionpoint Group), and Tom McHugh, CEO and Co-founder of FINBOURNE Technology, shared their perspectives.

Over the last 10 years, new technologies have allowed firms to capture greater volumes of data with increasing granularity. The types of data firms are dealing with is also largely unstructured and from a wide variety of sources, yet it still requires the same level of governance and control.

What are the key drivers instigating improvements in investment operations and the implementation of data strategies?

The amount of data has grown exponentially in all organizations and firms are now dealing with more diverse and more complex data. This is driving a change in the way firms think about and interact with data. Data silos have become more prominent and there is an ever-greater need for data across teams. Clients need a better way to communicate across functional silos to do their day-to-day work.

“One of the current challenges that we’ve seen is a lot of clients have legacy file exchange methods that are either SFDP or flat file uploads and they come in different formats and cadences, whether it be real time, daily, weekly, quarterly,” said Miguel Castaneda at Alpha Alternatives (formerly Lionpoint Group). “When an issue comes up there is a lot of emailing back and forth, resending and reloading. That causes delays across all the teams in the front middle and back office that need access to that data,” Castaneda said.

Where should a firm start with establishing a modern data strategy?

Duncan Cooper, Northern Trust

The first step is to conduct a thorough audit of where they are now and where they would like to go so that they can be strategic about what their data infrastructure should look like.

“Understanding how much data they are dealing with, where the data is going and the rate of decay or entropy of that data is a really good place to start.” – Duncan Cooper, Northern Trust.

According to Tom McHugh at FINBOURNE, firms often lack a clear understanding of the data terminology. Firms should first get a handle on what terms such as data lakes and lake houses really mean, and then look at their processing on top of it.

Tom McHugh, FINBOURNE Technology

“It boils down to three things: what are you going to use it for, who cares about it, and who is responsible? Who really owns it and who cares if it is not right? If they can solve that little panacea, everything else tends to be just technology that works around it.” – Tom McHugh, FINBOURNE.

The panelists were clear that firms should focus first on the process and the business need rather than just looking at the shiniest new tools. “What money will they save, what potential revenue could they open up, what risks could they mitigate? How will they get a better understanding of their data within the organization to be able to understand where potential risks may be or how they can optimize the business?” Cooper said.

“It is incumbent on good technology vendors to not necessarily sell what they have, but actually look at what solutions people need. That is easier said than done, but it breeds better outcomes.” – Tom McHugh, FINBOURNE.

What is the view on realistic uptake and the application of AI in data management within investment operations today?

Artificial Intelligence is seeing a lot of hype for its ability to process data at scale, but it is not yet widely used in financial services. “People want AI in their technologies, but do not always understand the costs involved,” said Castaneda. It is not just the AI models and compute power, but all the upfront energy that goes into creating a data strategy or a data environment to enable AI.

Miguel Castaneda, Alpha Alternatives

“Firms should approach AI incrementally, and not just in terms of technology, but also in terms of people, process and data.” – Miguel Castaneda, Alpha Alternatives (formerly Lionpoint Group).

Firms have been very cautious with using AI, according to McHugh. People are using AI to provide meeting summaries and as an email assistant. But in the rest of financial services, people are wondering if they have the right to train the model on data they are looking at. It is unclear who owns the product of that. There is no real standard on digital rights for market data, for reference data and for the customer’s data. And firms have not yet put in the necessary safety rails for people to be comfortable using AI, McHugh said.

If AI can help in the workflow and give a helpful suggestion or automate a task in an overall workflow, where a human is still in the loop, that is a good use case for now, said McHugh. The technology will evolve and become a more expected feature, but firms need to make sure they have the right governance and security in place to know what happens once they enable AI.

Traditionally, high-net-worth individuals and family offices have struggled to invest in private markets, in spite of their high collective AUM. In this article, Myles Milston, Co-Founder and CEO of Globacap gives insight into how technology is opening up access to private markets for private investors and analyses how increasing allocations from these investors will affect the market.

Private markets are experiencing a boom. Allocations are significantly increasing across the board from all types of investors. High-net-worth individuals (HNWIs) and family office investors are no exception to this rule. Diversification into private markets is now a strategic must-have for investors, particularly as the market faces higher levels of volatility.

This is a huge moment for individual investors, who aren’t letting this opportunity escape them – individual investors are set to invest an additional $1 trillion of retail assets into alternatives over the coming five years.

Private investors now oversee a sizable proportion of worldwide AUM, given the substantial growth in private wealth in recent years. The collective private markets assets under management (AUM) of family offices have more than doubled in the last 10 years, and the number of global private wealth owners is set to increase by 28.1% by 2028.

This positions HNWIs as key catalysts for future growth in private markets. But why are private market allocations growing at such an increased rate and how will this affect the real economy? economy?

Private markets pique investors’ attention

Private markets have made huge strides forward in recent years. Over the past decade, they have increased funding, boosted liquidity and embraced automation and technology, making them an attractive alternative to investing in public markets.

While EMEIA IPO activity continues to shrink, private markets are beginning to function more smoothly, quicker, more efficiently, and at a greater scale than before.

Private companies planning to list and those that have already gone public are increasingly finding private markets more attractive. This is because companies can now access the funding and liquidity they need while avoiding the complexity and expense of going public.

For investors, private markets offer a variety of benefits. Not least among them are the higher returns and stability they often provide, doubling as a strong hedge against inflation. Private markets also give investors a chance to invest in the real economy, diversifying away from more traditional stocks and bond investing routes.

Historically, HNWIs and family offices have faced challenges in accessing private assets, and it’s been cost-prohibitive for private markets-focused funds to offer access at scale. Slow transaction times, often taking weeks to process, combined with low liquidity and funding levels have kept investors reluctant to engage with the space.

Specifically, HNWIs and family offices’ small size often acts as a barrier to entry into the market. With typically lower AUM and high minimum investment requirements that are common for private market opportunities such as private equity or venture capital, HNWIs and family offices are often unable to invest.

In addition, regulation also prevents individual investors from entering private markets, as they need to be officially certified as having a high net worth or as sophisticated investors. To be certified, investors must have an income of at least £170,000 and net assets of at least £430,000 over the last financial year, preventing many from participating in the market.

However, strides forward in private markets’ technology have reduced transaction times and opened up accessibility to make private markets an attractive alternative to traditional public markets. Advances in workflow automation software, for instance, are bringing private markets’ efficiency in line with that of public markets.

Additionally, new technology and products, such as digital nominee solutions that offer alternatives to traditional structures such as SPVs and feeder vehicles, have made it feasible for asset managers to take HNWI investment at scale efficiently by pooling smaller ticket investors under a single LP.

As a result, interest from private investors in allocating greater portions of wealth into private markets is on the rise. In fact, new research shows that nearly half (46%) of family offices see an increased focus on private markets as a key area of difference for the next generation’s investments.

Driving the economy with increased participation

Investors of all types are eager for a slice of the lucrative private markets pie, with this becoming one of the more exciting areas of the market in recent years. Private investors’ flexibility means that they are particularly well-positioned to adapt quickly and take advantage of any new opportunities.

Historically, HNWIs and family offices have found it difficult to access the lucrative returns on offer in private markets. However, access is being widened for these investors through new technology such as digital nominee structures, empowering them to become more involved in this area of the investment market.

Growing incoming allocations from private wealth, along with bolstered private markets AUM and more seamless access to investments could provide a significant boost to the economy by unlocking trillions of dollars’ worth of new capital for investment in companies globally.

TECH TUESDAY is a weekly content series covering all aspects of capital markets technology. TECH TUESDAY is produced in collaboration with Nasdaq.

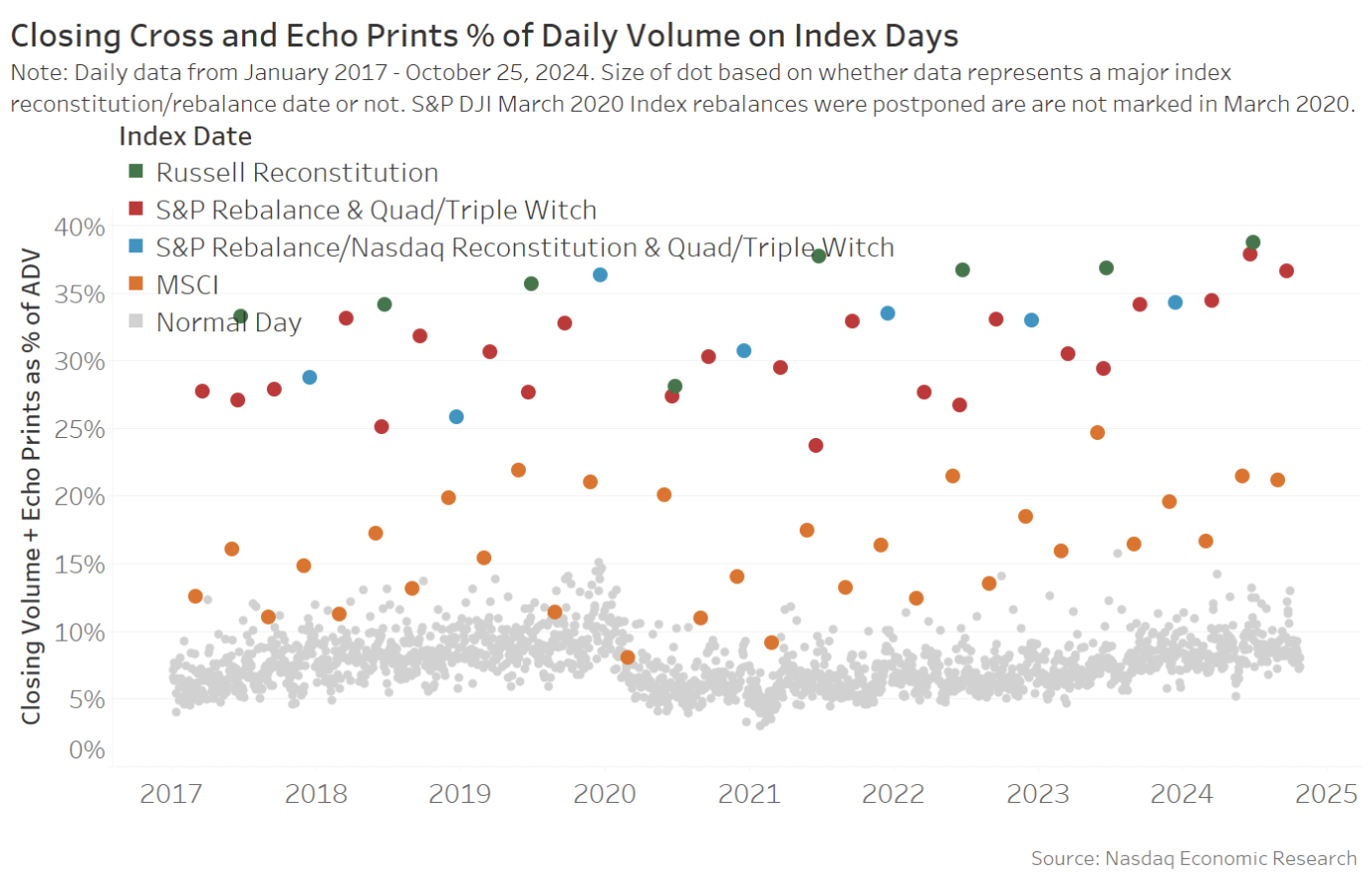

As we’ve noted before, index rebalance days tend to result in much larger closing auctions. That’s because most index funds try to exactly match what their index provider does – and index changes happen using the official closing price.

For example, a typical close accounts for less than 10% of volume traded during the day; meanwhile, some index rebalance dates see over 30% of volume traded in the close.

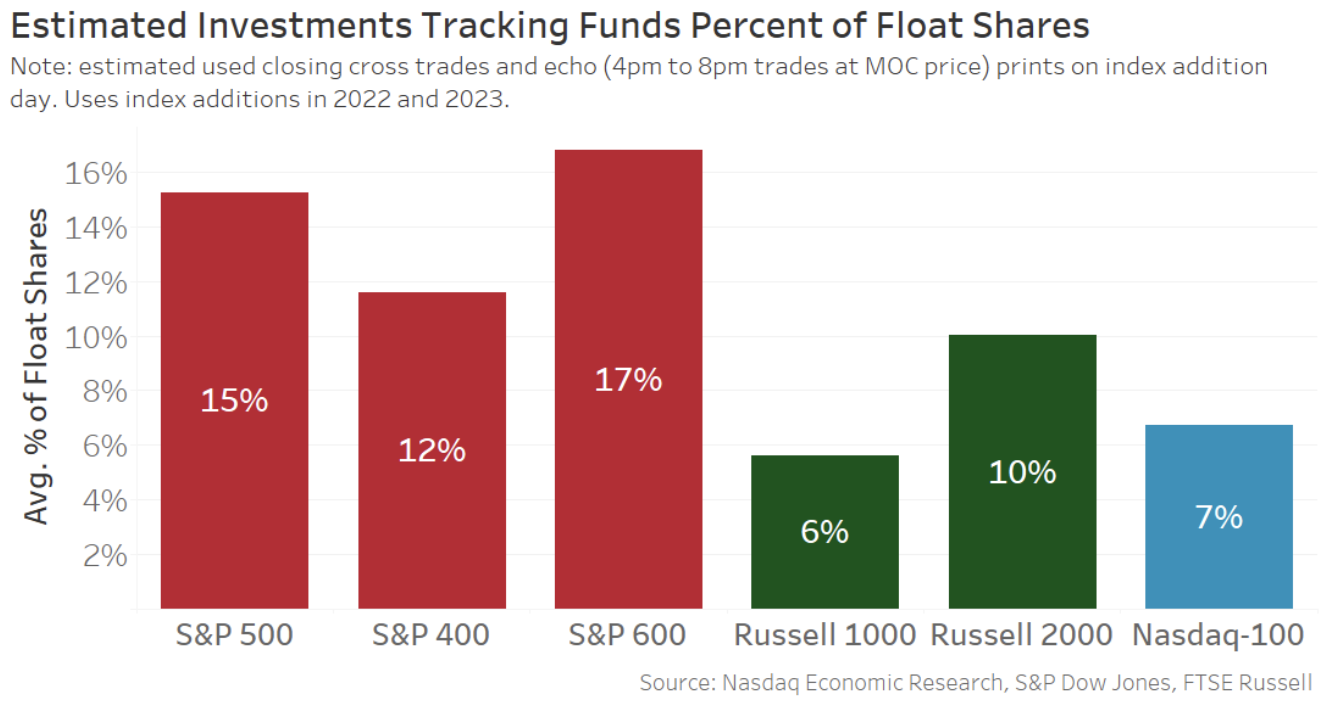

Based on this knowledge, we can use the size of the closing trades on index addition days to estimate total index fund tracking. The results show that many companies might have around a quarter of all float-shares bought by different index funds.

It’s important to note that companies benefit from being added to major indexes as they see significant new (and typically long-term) investors.

Index rebalance days have large close volumes

As the data in the chart below shows, there are just a few dates each year index trades typically happen:

MSCI is (typically) at the end of May and November. S&P, Nasdaq and FTSE indexes rebalance on the third Friday of the last month in the quarter. That’s also “quad witch” day, which makes the close volumes even higher.

Russell rebalances their indexes once a year, usually on the last Friday in June that is not quarter end.

Chart 1: Index rebalance days see exceptionally large closing volumes

A typical close currently adds to around $40 billion in trading, which is less than 10% of the volume traded during the day (grey dots).

In contrast, S&P and Russell index dates see an average $240 billion trading in the close, adding to over 30% of the day’s closing volume, and significantly elevating the total trading during the day (ADV), too. Even MSCI rebalances cause the close to increase to around 20% of ADV.

Using closing trading to estimate index tracking

There are two ways we can estimate how much index funds tracking each index adds:

Top down: Sometimes index providers disclose how much money tracks their indexes. Some academics have also added up all the index fund holdings from 13F filings. You could even try to reconcile that to ICI disclosures that nowadays say index funds are around 50% of all mutual funds.

Bottoms up: Another way is behavioral – to look at how many shares actually trade on the index rebalance dates. Knowing that index funds only really need to trade on the rebalance date, and that in order to accurately track the index before market open the next day, many funds prefer to trade at the same time as the benchmark is changed (which is the close!), representing another way to see how big index funds might be.

Today, we use the bottoms up approach to see how many float-shares actually trade on rebalance dates across the major U.S. indexes. The results (Chart 2) show that:

Small caps actually have significant proportion of index tracking, 27% total in the S&P 600 and Russell 2000.

Although, a large cap can qualify for all three major indexes, including the Nasdaq-100®, it could have up to 28% of its float shares held by index funds.

Even though far more dollars are indexed to the S&P 500, as much as $7.5 trillion, it’s the proportion of each company’s float shares that we are measuring here – and that should be consistent across all companies in each index.

Chart 2: Index day close trading indicates index tracking funds could own around 25% of float shares in many companies

Importantly, neither the top-down nor bottom-up approach is perfect. Some futures and options hedges might trade like index funds, while actual index funds might pre-position to try to limit market impact from the predictable index trade. Some also claim that some active funds trade like “closet indexers.”

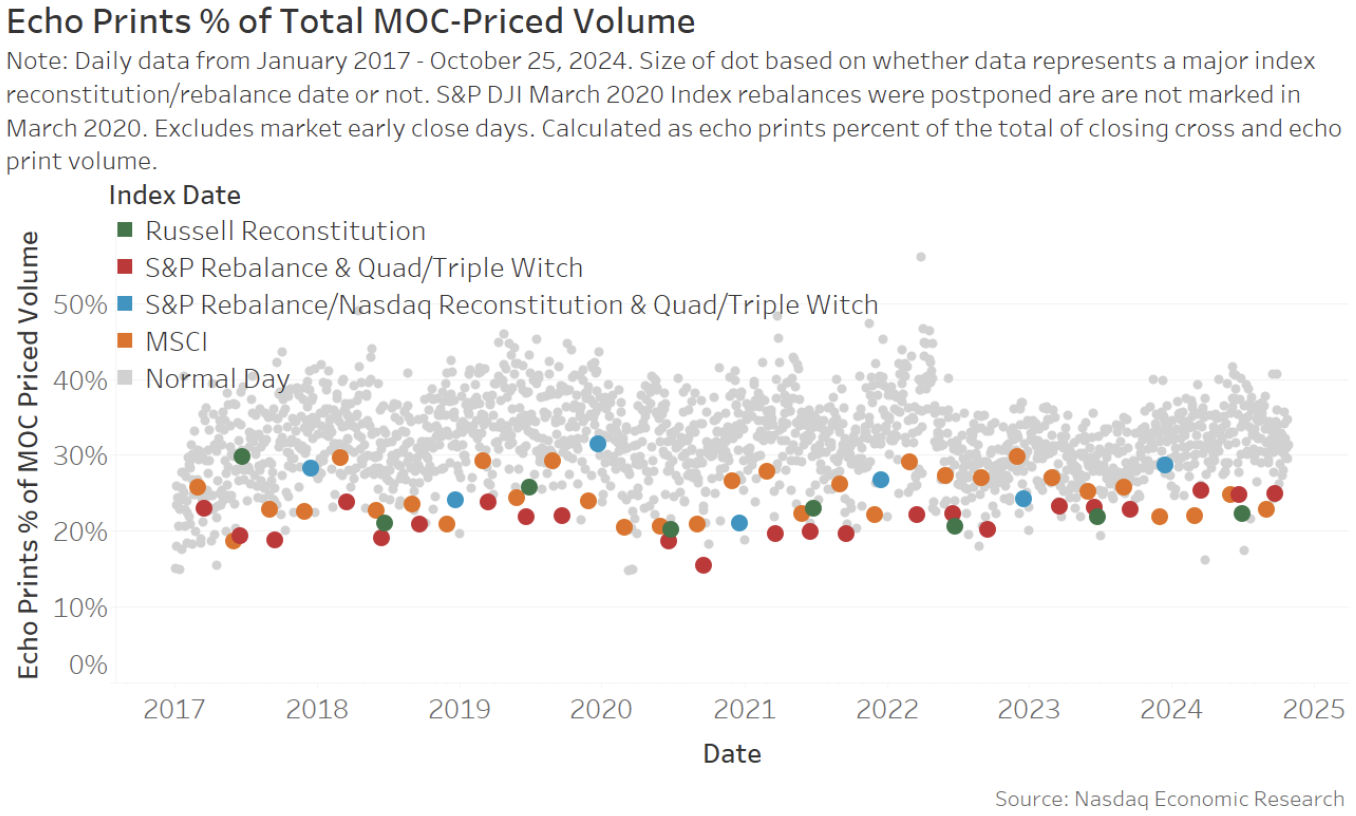

Closing volumes need to include some off exchange trades now too

Off-exchange trading is becoming larger and larger. That’s also true in the close.

Exchanges and brokers can both publish so-called “echo prints” that copy the official close price (MOC) but print to the “tape” after they find out what the official close price is.

In this study, we add the echo print trades that occur from 4 p.m. to 8 p.m. and are at the MOC price – to the “MOC volumes” we use above. Interestingly:

On a typical day, we see the echo prints average around 30% of the MOC volumes (grey dots in Chart 3).

On an index rebalance day, the official close seems more important, with echo prints adding to around 20% of all trades.

Chart 3: Echo prints contribute a consistent proportion of total MOC-priced trading

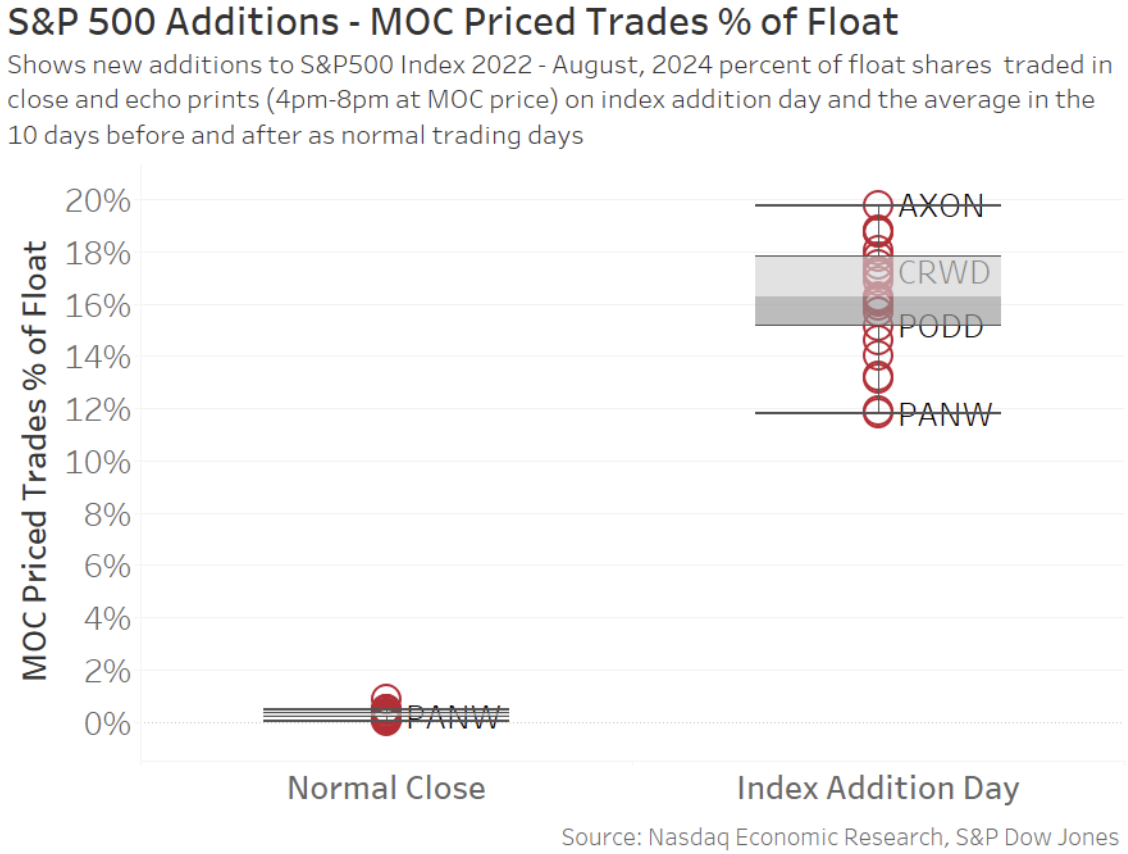

Normal close trading is likely a fraction of trading on index rebalance dates

Some might also wonder if we shouldn’t remove “normal”, or non-index, MOC volume from the totals above. Especially given we have previously said that the MOC is typically more active (and less index) than people think.

However, when we look at how much volume trades in a “normal” close – and compare it to how much trading that we see on index addition dates – we see that any adjustment would be a rounding error (as Chart 4 shows).

The reason index trades appear so much larger in this view is because the data in chart 1 is for the whole market – while index trades typically affect just the added stocks – so the effect is magnified (or focused) on the index add stock.

This also highlights how important index additions are for companies. They result in a material fraction of total float shares being bought by index funds – and index funds are typically long-term holders.

Chart 4: The “normal” MOC activity is a fraction of the index trading on a rebalance day

The data in Chart 4 also shows the typical dispersion of results that we average in Chart 2. Although the average S&P 500 addition adds to 16% of a company’s float shares the actual trade typically ranges from 14% to 18%, and sometimes much more.

It’s also worth noting that most S&P additions happen away from quad witch. That’s important, as quad witch trading might otherwise exaggerate the S&P results.

Typically, the S&P quarterly rebalance includes “other” index changes, like float, style and shares outstanding updates. Because the S&P 500 is a “500 company” index at all times, additions are typically made whenever another company leaves the index (often through M&A). Although, to be fair, the past few quarterly rebalances have included some promotions and demotions to reallocate stocks to more appropriate market cap groups.

Index addition is good for companies

We know that index addition creates a significant amount of liquidity in an added stock.

This research shows just what proportion of float shares change hands, and are likely bought by index funds, on those dates.

Importantly, index addition is mostly good for companies. Index funds are a large, long-term, new investor base. Index inclusion also increases interest from active mutual funds, which may increase access to U.S. capital for future investments.

Nicole Torskiy, Economic Research Senior Specialist, contributed to this article.

Creating tomorrow’s markets today. Find out more about Nasdaq’s offerings to drive your business forward here.

TS Imagine has acquired PrimeOne, a provider of operational risk management solutions for the prime brokerage industry, from S&P Global, according to CEO Rob Flatley.

“I am fortunate to be able to reunite with the PrimeOne team at a perfect time for TS Imagine,” he told Traders Magazine.

Rob Flatley

The combined team will operate under the TS Imagine brand, and global headquarters will remain in New York. EJ Liotta, leader of PrimeOne, will join TS Imagine’s executive team.

PrimeOne was founded by Flatley in 2011, as part of CoreOne Technologies. He then sold CoreOne and its four core products, RegOne, DeltaOne, VistaOne and PrimeOne, to IHS Markit in 2015. In 2022, S&P Global and IHS Markit completed their approximately $140bn merger, and PrimeOne’s products became part of S&P Global Market Intelligence.

Flatley formed TS Imagine following the merger of TradingScreen and Imagine Software in 2021.

TS Imagine innovates by drawing on nearly thirty years’ experience serving the world’s most sophisticated financial institutions through changing markets and shifting regulatory landscapes.

The Company delivers a SaaS platform for integrated electronic front-office trading, portfolio management, and financial risk management tools to the buy-side and sell-side.

“We are well-positioned with large institutional clients, on both the buy-side and the sell-side, for cross-asset class electronic trading, and cross-asset class financial risk management,” Flatley said.

“The financing business is adjacent to the markets currently served by TS Imagine. For firms that use leverage, trading and financing are inextricably linked. Their trading flows will follow where they finance,” he said.

Flatley said that the hardest part about setting up financing technology is the actual integration with risk management and the margin systems: “that’s where a lot of people might get into trouble”.

PrimeOne’s platform offers key services such as stock borrowing, lending, and margin management, which will complement TS Imagine’s existing technology.

The acquisition will allow TS Imagine clients to streamline workflows and improve operational efficiency.

When Flatley bought TradingScreen and Imagine Software, he realized that he’d “love to buy PrimeOne back.

“I felt like we had two amazing pieces of a puzzle, but there was a third piece where we could go in and really help firms deliver what they need faster, and also do that with zero operational and integration risk,” he commented.

The integration of PrimeOne’s tools with TS Imagine’s RiskSmart platform aims to enhance real-time risk monitoring by leveraging PrimeOne’s operational and financing data. Additionally, PrimeOne’s expertise in swaps will support the expansion of TS Imagine’s TradeSmart OEMS into swaps.

The acquisition creates several opportunities in product integration, product development and cross-selling.

According to Flatley, the market has expressed a desire for a single solution with RiskSmart quality real-time analytics paired with the robust prime brokerage infrastructure of PrimeOne.

“There are not that many systems where the buy-side and the sell-side can actually use the same risk management system,” Flatley said.

In addition, PrimeOne’s expertise in swaps will be integrated with TS Imagine’s TradeSmart OEMS, paving the way for electronification and automation of the swaps market.

The current state of electronification in the swaps market is “pretty weak”, according to Flatley. “When you want to go out and price a swap, it’s almost done exclusively on chat and email,” he said.

PrimeOne’s technology electronifies the equity terms for the swap and the financing terms, so the buy-side and the sell-side have the same rule book in terms of how they’re going to manage their exposure, Flatley said.

“We’ve electronified the fixed income market using electronic RFQs, we’ll take the same approach in the swaps market,” he said.

Commenting on the impact of the greater electronification in the swaps market, Flatley said: “The buy-side will save money, because today that work is analog and it’s not that efficient.”

In addition, Flatley thinks that firms will be able to get in and out of positions a lot easier with fewer error prone operations.

“It’s a good performance enhancer as well. You get the best inventory management relative to the exposure that you’re trying to achieve,” he added.

The AI Insights: Revolutionizing Financial Trading panel, opened with the simple, straightforward question of what has changed in the past year.

It was noted that conversations in October 2023 were more about pilot programs and proofs of concepts, whereas now with more development now there is more AI actually in use.

Still, some unrealistic expectations of a “magical trading robot” or the like remain out there, and remain far from being realized.

AI goes hand-in-hand with data, and the panel noted that AI is making strides in giving traders more useful knowledge while reducing the noise that comes from data overload. For example, an AI-powered cluster model can screen stocks for characteristics such as capitalization, liquidity, and spread, telling the trader whether a given stock is relatively easy or difficult to trade.

Even if that works well, one panelist said “there is always information on the trading desk that is not captured in data, and you need a trader to still make human decisions.” And in fact, areas of progress over the past year have been in better human decision-making and challenging of the data.

Risk management is fertile ground for applying AI, including the newer generative AI, the panel noted. AI won’t itself solve a risk problem, but “it will give a human expert a head start on where it’s best to apply efforts” to solve the problem.

The panel stressed the importance of guardrails and education in rolling out AI. The technology “isn’t really making decisions in these early days. But it is freeing up humans to do more interesting and important work.”

One rough benchmark to strive for is AI freeing up 90% of human trader and technologist time, so they can focus on the most important 10% of their work.

The future of AI is potentially boundless, as it was noted that today’s AI models “are the worst you’ll ever see” when compared with what’s to come.

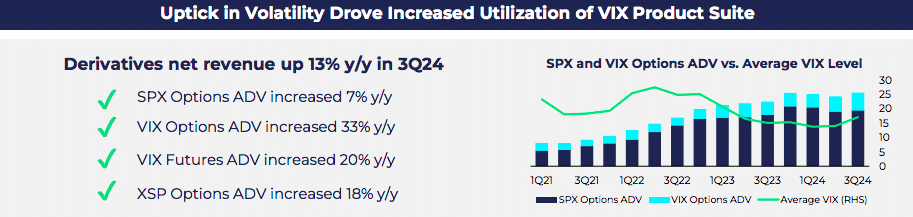

Cboe Global Markets had record derivatives volumes in the third quarter, which the derivatives and securities market operator said was driven by proprietary index options and futures products.

Source: Cboe

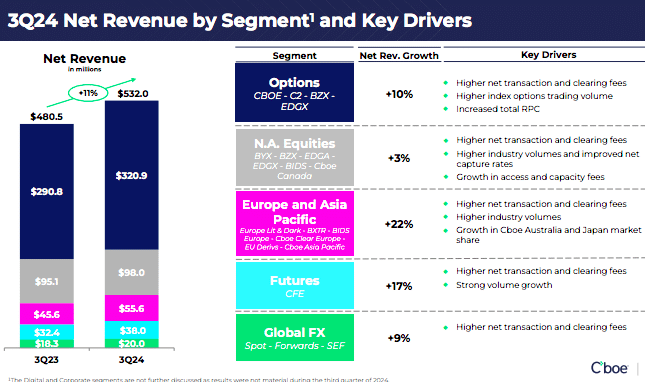

The group reported record net revenue for the quarter of $532m, up 11% year-over-year. Derivatives net revenue grew 13% year-over-year in the third quarter due to record volumes.

Fredric Tomczyk, chief executive of Cboe Global Markets, said on the third quarter results call on 1 November that the record results were driven by strong volumes in its derivatives franchise, specifically the proprietary index options and futures products. In addition, there were “solid” volumes across cash and spot markets, continued expansion of the data and access solutions business and steady expense management.

Fredric Tomczyk, Cboe

Tomczyk said: “Over the past year as CEO, I have concentrated on sharpening our strategic focus and making important and deliberate decisions on how to best allocate our capital and resources to support our growth strategy.”

As a result of the strategic review, the group has dialled back its M&A activities, lowered expense growth and stabilized margins. The capital allocation strategy has changed to increase investments in organic initiatives and reallocated resources to align with core strengths, which Tomczyk described as derivatives; data and access solutions and leading-edge technology.

Although Cboe will focus on an organic growth strategy, the group will continue to explore acquisitions that provide scale and broaden distribution inside key geographic markets. “I have always said we were going to slow down M&A, but I have never said we were never going to do M&A,” said Tomczyk

He highlighted that Cboe has just acquired a 14.8% ownership stake in proprietary trading system, Japannext.

“Japan is one of the largest and most important capital market places in the world, and is undergoing a lot of change as the regulatory landscape evolves and the market opens to more competition,” said Tomczyk. “We see tremendous opportunity for Cboe to compete.”

Options business

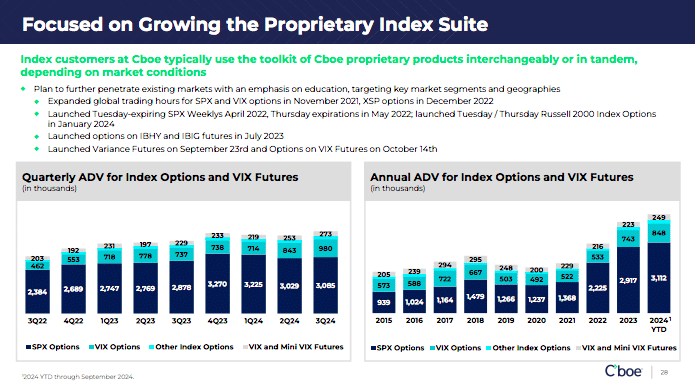

The strategic framework includes investing in the continued growth of the core global derivatives business as there is increasing demand for access to the US market, and for options.

“Given that options by their very nature expire, investors must repurchase new options to reposition themselves in the market, which in turn creates a quasi-recurring revenue stream that continues to increase,” Tomczyk added.

Options achieved record net revenue of $320.9m, up 10% from the third quarter of 2023. Dave Howson, global president of Cboe, said on the results call that the increase was led by strength in proprietary products.

Source: Cboe

Howson said the most notable event in the third quarter was the yen carry trade unwind on 5 August that produced one of the largest short-term volatility events since the Covid pandemic and the global financial crisis.

“Investors rushed for downside protection in the form of VIX options and ADV of 1.2 million contracts in August was the second highest on record, trailing only February 2018,” added Howson.

He also highlighted the launch of variance futures on 23 September, which Howson described as the latest tool in Cboe’s volatility toolkit to provide an exchange-listed alternative to over-the-counter variant swaps.Variance futures offer a streamlined approach to trading the spread between implied and realized volatility of the U.S. equity market as measured by the S&P 500 index, enabling market participants to take advantage of discrepancies between market expectations and actual outcomes.

In addition, Howson noted the launch of options on VIX futures on 14 October. Cboe offered securities-based VIX index options but the new contracts are physically settled. With futures as the underlying asset, the new options are CFTC-regulated, enabling access for market participants that are restricted from accessing U.S. securities-based options to use the product to express their views on equity market volatility.

David Howson, Cboe Global Markets

Options on VIX futures also allows Cboe to offer more tenors, in particular, those with a shorter duration that meet customer demand. Howson said: “These two additive products need time to seed, but the early signs are really good, though. We have got prices on the screen, customers engaging and testing the plumbing, and a good pipeline coming through.”

He continued there is also a meaningful opportunity to bring options to a greater portion of the US customer base, especially using exchange-traded products to access a variety of options strategies in a traditional ETF wrapper.

“US listed options-based ETFs have grown to an estimated $120bn in AUM, with assets increasing over 600% over the past three years,” added Howson.

Retail market

Cboe also remains optimistic on the growing retail participation in the options market. In October this year Cboe and Robinhood Markets announced they will launch Cboe’s index options on the retail broker’s platform, which is slated for this quarter.

“We believe retail adoption of index options is just beginning, and Cboe is well positioned to cater to this growing demand,” added Tomczyk.

The strategy for supporting continued retail growth includes education, broadening access by working with retail brokers and listing products that provide opportunities for customers to trade a contract that is the right size for them and on a time frame that suits their needs, particularly shorter-dated contracts. Cboe estimated that less than 10% of customers at large retail broker-dealers are currently enabled to trade options.

International growth

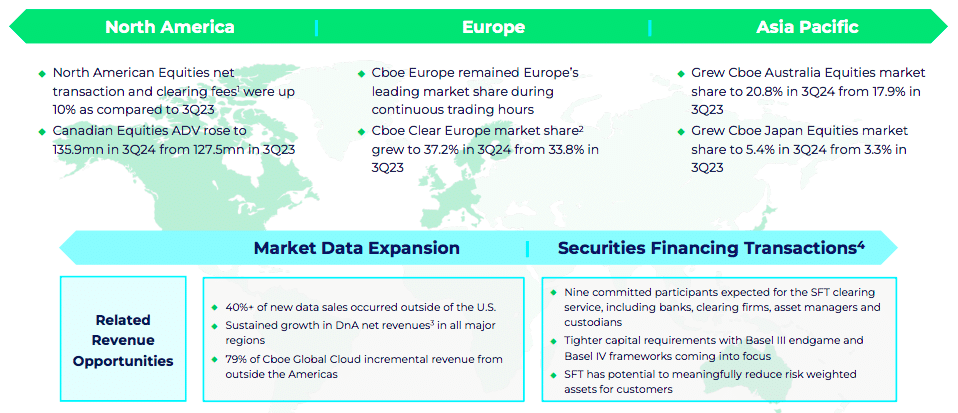

During the third quarter, approximately 40% of new sales in the data and access business were international.

“We remain particularly excited about the outlook for our Canadian business as we remain on track with the migration of our Canadian market to Cboe technology in early 2025, subject to regulatory approval,” said Howson.

Source: Cboe

In Australia Cboe grew market share to 20.8%, up 2.9% from the third quarter of 2023. In Japan market share hit 5.4% in the third quarter, a 2.1% improvement from the same period in 2023.

“The Asia Pacific region remains a key focus for Cboe as we move forward, providing a number of opportunities across our ecosystem to fuel growth,” said Howson.”We anticipate continued strategic investment in the region in increased brand awareness and improved sales efforts for the import of derivatives activity into the US.”

Technology

In February this year Cboe introduced dedicated cores for its EDGA equities exchange. Dedicated cores allows members and sponsored participants to host their specific logical order entry ports on their own CPU core(s), rather than sharing a core(s), which reduces latency, enhances throughput, and improves performance.

“The uptake from dedicated cores continues to exceed our expectations as we roll the functionality out across additional markets,” Howson.

Dedicated cores is due to launch in the UK and Europe in this quarter and the first quarter of next year, then Australia, and eventually Japan and Canada.

Chris Isaacson, Cboe

Chris Isaacson, chief operating officer, said on the call that the Canadian migration in March will be the last onto Cboe’s technology platform.

“We have spent a fair amount of time and a lot of resources this year making that happen,” he said. “We think that will free up a substantial amount of resources to focus on high growth areas like derivatives and data and access.”

Isaacson added that Cboe is investing heavily in its data analytics platform and on artificial intelligence to drive productivity within the organization, but also to explore and enhance revenue opportunities for customers.

Source: Cboe

Jill Griebenow, chief financial officer, said on the results call that Cboe is raising the organic total net revenue growth range for 2024 to between 7% and 9%, up from the prior guidance of 6% to 8%, given the year-to-date trends and expectations for the fourth quarter.

Who Pays for Innovation? Why Market Collaboration is the Key to More Connectivity

By Bob Cioffi, Global Head of Equities Product Management, ION

The equities trading landscape has taken a dynamic turn over the past few years. While the continued dominance of low-touch, algorithmic trading has accelerated the speed of activity, the rise of alternative trading venues worldwide has unlocked a wider range of options and opportunities.

Firms are feeling the pressure as a result. While buy-side businesses jostle for access to as many markets as possible to avoid missing out on liquidity, sell-side firms are competing to help deliver on those ambitions. However, both are struggling to keep up with the pace of change.

The market needs more agility and connectivity to manage greater volumes and demands. But the question of who takes ownership for this innovation – and bears the cost – is more complex. With more market players than ever before, firms, venues, and technology providers need to work out how to share this burden to reap the collective benefit.

New competitive dynamics

Across the equities market, choice and competition among trading venues is ramping up.

New, alternative trading venues have been challenging traditional exchanges for some time. Both are experimenting with new functionalities and order books – auction, dark, lit, and conditional – to differentiate themselves as the go-to platform for clients. In Europe, the London Stock Exchange (LSE) acquired Turquoise to draw liquidity back in response to post-MiFID liquidity fragmentation, while Euronext has grown by acquiring exchanges in Dublin, Oslo, and Milan.

Less typical market players have also entered the fray to challenge the primary exchanges. These range from banks creating their own trading venues, such as UBS’ MTF and Goldman Sachs’ MTF (SIGMA X), to brand new exchanges such as Artex, which offers tokenized art funds as a new investment opportunity and allows museums to trade digital asset securities like equities. The rapid growth of IntelligentCross, an alternative trading system (ATS) is another good example.

In a fragmented landscape where multiple venues offer free market data and connectivity with prominent liquidity providers, horizontal differentiation – exchanges offering different types of products or services to cater to different market segments – is increasingly common. We are at a point where no single venue can serve the interests of all investors.

Pressure on the system

It’s common for firms to want to “try before they buy” with access to new venues in the market. But building the technology to create fast access in this way is costly – both in time and resources.

For sell-side businesses to deliver best execution for their clients, the cost of connecting to every available venue currently outweighs the benefits. This leads most to opt for selective connections and rely on broker services. For buy-side firms and end-users deciding which markets they would like to access and how, these different approaches to connectivity will continue to shape their decisions, especially as different types of trading venues evolve. Naturally, technology providers are under pressure from all angles to build and monetize a new era of market infrastructure: solutions that can support connectivity to new venues, and therefore help all parties achieve their goals.

As a rule, greater competition is an economic good. It moves the market forward, breeds innovation, and results in lower costs. But key industry questions – such as who should take the lead in modernising market infrastructure to meet abundant modern connectivity needs – make reaching a verdict more difficult.

Addressing the challenge

As venues and order types grow in number, the degree of overhead in today’s market is significant – and the pace of change is fast. The question is how the market can innovate to keep up at a time of such rapid development.

Traditional processes for securing connectivity such as the manual configuration of connections and the lengthy onboarding of new clients are no longer quick or adequately responsive to meet needs. Technology firms need a way to work with new venues and exchanges to meet the needs of market participants.

At the same time, the growing trend of consolidation across exchanges in terms of ownership – for instance, the widespread adoption of Nasdaq’s technology – is also helping exchanges to take a big leap in terms of capabilities and offerings. Alongside the opportunity for new technology markets to provide much-needed common interfaces between different venues, a broader shift towards efficiency and scalability is already unfolding through consolidation.

Looking to the future

As we move ahead, it is through a collaborative effort that the market can address the challenge of funding new demands for innovation. With liquidity and best execution at stake, market connectivity is more important than ever. This bid for more options and flexibility is a prime opportunity to create a more resilient, agile market structure that can support the demands and direction of modern trading.