Paul Atkins will soon testify before the Senate Banking Committee for his potential SEC Chairman nomination, with no set date. If approved, a full Senate vote could confirm him within three weeks.

Paul Atkins

In addition to facing questions on his regulatory philosophy, enforcement priorities, and the SEC’s mandate: protecting investors, ensuring fair markets, and supporting capital formation, Atkins will face more specific inquiries. In this second of a multi-part series about the topics he will most likely face, we highlight the limitations that the SEC has in policing stock trading by government officials.

Congressional stock trading continues to captivate and confound the American public, raising persistent questions about fairness and accountability in government. Every day, we learn about these occurrences through a steady drip of financial disclosures mandated by the Stop Trading on Congressional Knowledge Act (STOCK Act) of 2012 shared via platforms like X, news outlets, and watchdog organizations that scrutinize trading reports for suspicious patterns. Yet, despite this transparency, many wonder why such behavior is seemingly allowed to persist, especially when the same actions would land private citizens in legal jeopardy.

For those of us in the financial industry, frustration and anger run very high. In our jobs, we face strict regulations on trading stocks in our personal accounts. We’re subject to pre-clearance requirements, before executing trades, and holding period rules, which prevent quick buy-and-sell transactions to avoid short-term speculation. Additionally, we are restricted from trading stocks of companies where we have material non-public information, which for anyone on a trading desk includes every company under the sun. These policies are monitored with great proficiency and when violated individuals face severe consequences in the form of fines and lifetime bans from our industry. These regulations and industry standards prevent the occurrence and perception of widespread insider trading.

The STOCK Act mandates federal government officials to disclose their financial transactions within 45 days and prohibits them from using material non-public information for personal profit. While the STOCK Act applies to all federal officials, it is not equally administered. Many three-letter agencies like the FDA, FCC, IRS and others have discretion on what is demanded among their staff, which leads to inconsistent levels of transparency. Reporting standards by congressional members is stricter with information on trades more easily found in the public domain. This is why almost all the attention is on them.

Today, there is widespread skepticism about the efficacy of the STOCK Act in restoring public trust. Enforcement has been virtually nonexistent due to significant challenges within the legal framework. Investigating and proving intent, as well as a breached duty of trust, is nearly impossible and often leads to a political minefield. One major legal obstacle is the Speech and Debate Clause—a constitutional provision that grants members of Congress immunity from prosecution for actions or statements made in the course of their legislative duties—which hinders regulatory agencies’ investigations. Another barrier is the lack of direct authority over Congress; while the SEC can investigate individual members, it lacks explicit power to regulate or discipline them, leaving enforcement to the Department of Justice or congressional ethics committees. That said, the STOCK Act has successfully increased transparency in an area where none previously existed.

SEC Chairs face significant limitations in policing insider trading by members of Congress, making it difficult to find meaningful courses of action within those constraints without additional authority from Congress. Until such reforms are enacted, public frustration is likely to persist, underscoring the urgent need for legislative action to close these loopholes and restore faith in governmental integrity.

Montréal Exchange (MX), Canada’s derivatives exchange, has announced the launch of options on 10 CIBC Canadian Depositary Receipts (CDRs), marking a significant expansion of investment opportunities for Canadian investors.

The new CDR options, listed on MX and available at the opening of trading today, provide investors with access to options on fractional shares of U.S. companies while trading in Canadian dollars on a Canadian exchange.

CDR options allow investors to gain exposure via options to high demand U.S. underlyings in Canadian dollars, providing new opportunities for retail investors to diversify their portfolios within the Canadian market.

Elliot Scherer

“We’re proud of the continued evolution of our growing platform, now adding CDR options to our rapidly expanding product suite,” said Elliot Scherer, Managing Director and Global Head, Wealth Solutions Group at CIBC Capital Markets.

“As investors look for more ways to invest in global companies, we look forward to furthering our CDR offering and developing industry-leading solutions to meet investor demand.”

“MX is committed to providing innovative and tailored investment solutions to its clients,” said Robert Tasca, Managing Director, Derivatives Products and Services, Montréal Exchange. “With the launch of these options on CDRs, retail investors gain valuable portfolio management flexibility in Canadian dollars.”

The following CDRs are available for options trading:

Advanced Micro Devices CDR – AMD

Alphabet CDR – GOOG

Amazon.com CDR – AMZN

Apple CDR – AAPL

Berkshire Hathaway CDR – BRK

Costco CDR – COST

Meta CDR – META

Microsoft CDR – MSFT

Nvidia CDR – NVDA

Tesla CDR – TSLA

For more information, please visit MX CDR Options here.

TECH TUESDAY is a weekly content series covering all aspects of capital markets technology. TECH TUESDAY is produced in collaboration with Nasdaq.

I have an inquisitive 10-year-old son, and I want to foster his curious nature. As such, we embrace the mantra: “there are no bad questions.” That said, he doesn’t like my answers to “why can’t we get a Cybertruck?”

Kevin Davitt, Nasdaq

I try to cultivate a similar mentality when I’m part of educational events. Last week, I participated in Nasdaq’s regular cadence of webinars with Interactive Brokers.

As we wrapped a presentation that addressed the qualities that made and make the Nasdaq-100® Index (NDX) unique, there was a fabulous question that continues to grind in my mind. I’ll paraphrase the inquiry:

“Given the maturation of the mega-cap technology and consumer discretionary sectors, could you explain a scenario where NDX volatility (realized or implied) traded at a discount to S&P 500 Index (SPX) volatility?”

My response in the moment was sufficient, but this medium affords me greater flexibility to flush out the thinking.

Background

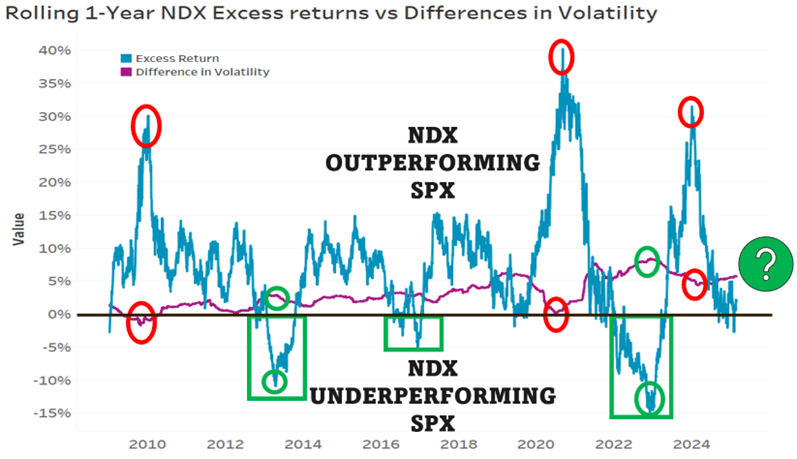

Historically, periods where NDX realized volatility is below that of the SPX are few and far between. The visual below is busy, but useful. The data starts January 1, 2008, and runs through mid-February 2025. Let’s understand what it shows.

Source: Nasdaq Economic Research

Blue line: Plots “Rolling 1-Year Price Returns” for the NDX minus the “Rolling 1-Year Price Returns” for the SPX.

Takeaway: Since the financial crisis, the NDX has consistently outperformed relative to the SPX. There have been ~3 periods of underperformance. Notably: 2013, mid-2016 and much of 2022 – highlighted in green.

Purple line: Plots the “Rolling 1-Year Realized Volatility” measure for the NDX minus the “Rolling 1-Year Realized Volatility” for the SPX.

Takeaway: Generally, the NDX realizes +3.1 higher volatility when compared to the SPX. The volatility spread narrowed considerably following the most acute crises of the past two decades, specifically after the GFC and during the COVID recovery – highlighted in red. Those vol convergences coincided with two of the most significant periods of NDX outperformance.

The bigger question becomes, why might that realized volatility spread narrow or expand?

Data:

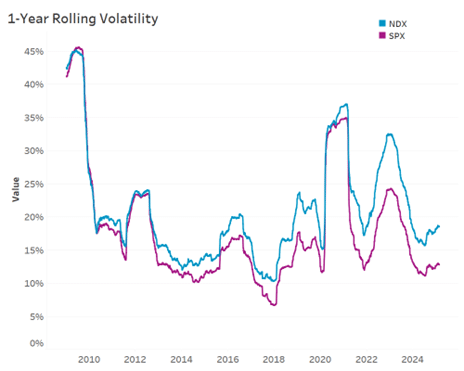

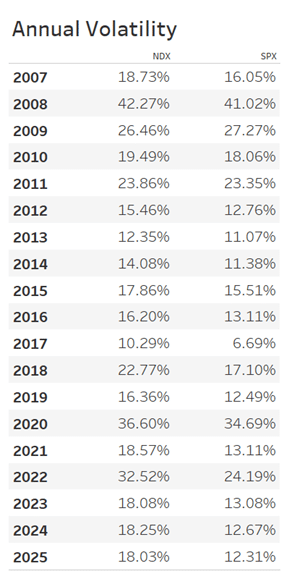

2008 – Present average NDX annualized volatility: 21.4%

2008 – Present average SPX annualized volatility: 18.3%

On average NDX moves with a 3.15 vol premium to SPX realized volatility.

2024 – NDV average annualized volatility: 17.0%

2024 – SPX average annualized volatility: 12.1%

Last year, the spread widened to an average width of NDX +4.9 vols.

The widest the rolling volatility spread date was December 2, 2022, and the period between late 2022 and early 2023 dominates the list widest spreads. That coincided with a meaningful bottom for the NDX and catalyzed a period of very significant outperformance. Mega-cap technology names suffered some of the largest drawdowns during the inflationary environment of 2022.

The list of dates where the vol spread inverted (NDX trailing vol < SPX trailing vol) is clustered around October and November 2009. Keep in mind that one year prior was the period of the most acute volatility during the financial crisis. While every sector was impacted during the 2007 – early 2009 selloff, the losses centered on and around the financial services area.

In fact, the list of largest bankruptcies in United States history are dominated by financials. Seven of the top 12 insolvencies were financial firms. Market history students likely know the two largest – Lehman Brothers (9/15/2008) and Washington Mutual (9/26/2008). Perhaps it’s no surprise that a year later, the trailing volatility for the NDX would be below the SPX.

In fact, the only full year (in window analyzed) where the NDX moved with a lower volatility than the SPX was 2009 (NDX vol = 26.46%; SPX vol = 27.27%).

Takeaway: As macro volatility (systematic risk) declines, the spread between NDX and SPX realized volatility tends to widen. When systematic risk increases (crises), the spread typically narrows. Over the past two decades, systemic risks have centered around financial firms. Periods of wider vol spread typically accompany NDX underperformance.

More Recently

Looking at NDX rolling excess returns (blue line above), the very meaningful outperformance during calendar year 2023 shifted on 12/29/2023.

NDX Total Return (2023): +53.8%

SPX Total Return (2023): +26.8%

That relationship has narrowed for the past 13 months. In late January 2025, it moved slightly negative, meaning 1-year trailing NDX returns were less than those of the SPX. The brief narrative there is one of mega-cap tech underperformance (short-term) and outperformance on the part of financials. We’ve been in a (historically) low correlation (high dispersion) market with some significant sector rotation.

Are we approaching an inflection point whereby the NDX begins outpacing again? Time will tell, but the continued growth in Nasdaq-100 (NDX) (and Nasdaq-100 Micro (XND)) Index Options may be indicative of sophisticated clients expressing their longer-term views on the relationship. Average daily volumes in the NDX hit a multi decade high in January 2025.

Large-Cap Equity Indexes are Not the Same

In many ways, volatility is the nuclear driver across capital markets. It’s at the core of every institutional and individual portfolio whether their beneficial owners know it or not. Change IS the constant. We invest because we expect things to change and over long horizons, that change tends to be for the better. It’s beneficial to asset owners.

The linchpin behind index option prices/values is volatility. Specifically, how volatile is the reference asset likely to be for the life of the option? It’s an estimate that changes dynamically. Index options can be used to define risk over a discrete time frame. They can be used express a forward-looking view. Index options can be incorporated to potentially enhance portfolio yield or manage cash flows. They are profoundly flexible tools.

At the index level, volatility is driven by the constituents (and their pairwise correlation). There are very real differences between the NDX and SPX. The NDX includes the 100 largest Nasdaq-listed companies, excluding financials. The median SPX sector exposure to financials since 2000 is 13%. The NDX includes no financials. For a full breakdown of NDX methodology: https://indexes.nasdaq.com/docs/Methodology_NDX.pdf

Keep asking questions and stay current on your Davitt Data for more analysis.

Bonus Visuals:

Source: Nasdaq Economic Research

Source: Nasdaq Economic Research

Creating tomorrow’s markets today. Find out more about Nasdaq’s offerings to drive your business forward here.

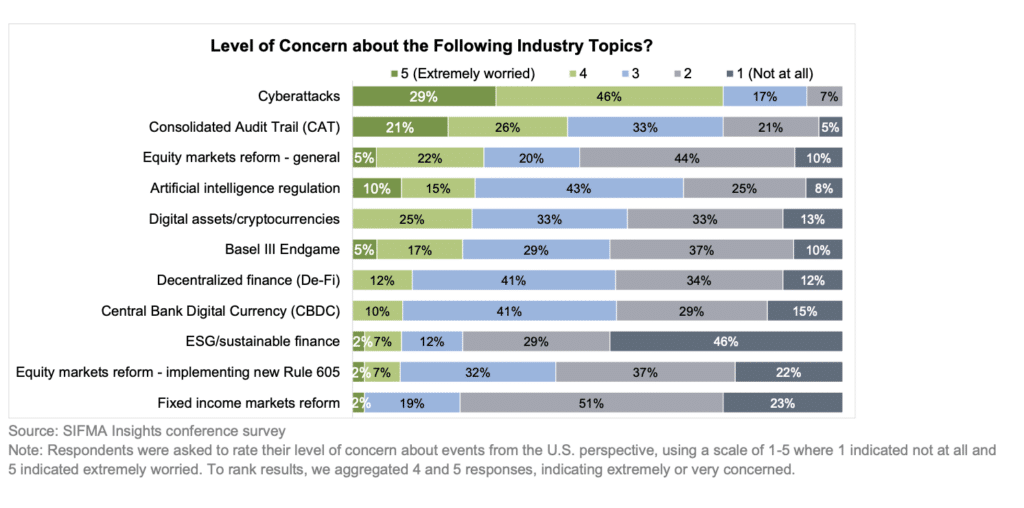

The financial services industry is facing an evolving landscape of risks and regulatory challenges, with cybersecurity emerging as the most pressing concern.

This underscores the persistent and growing threat of cyber intrusions on financial markets, which could disrupt trading, compromise sensitive data, and undermine investor confidence.

John Yensen

“Cyberattacks pose a very serious risk to financial stability with markets becoming increasingly digital,” John Yensen, President at Revotech Networks, told Traders Magazine.

Many firms are significantly strengthening their cybersecurity through zero-trust architectures, AI driven threat protection, as well as regular penetration and stronger encryption, he said.

According to Yensen, it is becoming more populate to collaborate with government agencies and cyber firms to help share intelligence with the goal if mitigating risks.

“I personally believe that more oversight is needed, especially with third party service providers that play a key role in market infrastructure even though regulations provide a “foundation”. Cyber threats evolve faster than regulations, requiring an adaptive, risk-based approach,” he stressed.

Yensen further said that advancements in AI and automated trading systems introduce new risks.

“While AI enhances fraud detection, it also expands attack surfaces. Threat actors can exploit algorithmic vulnerabilities or use AI-driven attacks to manipulate markets,” he said.

“Firms must implement real-time AI auditing, identity verification, and stronger threat modeling to mitigate risks,” he added.

Following cybersecurity, the Consolidated Audit Trail (CAT) was another major concern, with 46.2% of respondents expressing a high level of worry.

CAT, a regulatory initiative designed to enhance market surveillance by collecting trade and order data from across U.S. equity and options markets, has been a point of contention.

While intended to improve transparency and help regulators detect market abuse, some market participants worry about the security risks of maintaining such a vast data repository, as well as the operational and compliance burdens it imposes.

Beyond cybersecurity and CAT, a notable portion of respondents (26.8%) expressed significant concern over ongoing equity market reforms.

These regulatory changes aim to enhance market fairness, efficiency, and transparency, but they also introduce uncertainty for firms that must adapt to new rules.

Potential changes to order execution, market data access, and competition among trading venues remain key areas of debate.

The financial industry must navigate a delicate balance between regulatory compliance, market innovation, and security.

While cybersecurity remains the top priority, concerns over regulatory initiatives like CAT and broader equity market reforms highlight the industry’s broader challenges.

As firms continue to invest in technology and compliance measures, policymakers and market participants must collaborate to ensure that new regulations do not introduce unintended risks.

In an era of rapid technological advancement and evolving regulatory frameworks, financial institutions must remain agile, proactive, and resilient to safeguard the integrity of the markets.

FTSE Russell, the global index provider, today confirms the schedule for the 37th annual Reconstitution of the Russell US Indexes, set to occur at the end of June 2025.

This rebalancing process is designed to capture market shifts from the previous year to ensure the Russell US Indexes continue to accurately reflect the US equity market.

The 2025 Russell Reconstitution schedule is as follows:

Wednesday 30th April – “Rank Day” – Index membership eligibility for 2025 Russell Reconstitution determined from constituent market capitalization at market close.

Friday 23rd May – Preliminary index additions & deletions membership lists posted to the website after 6 PM US eastern time.

Friday 30th May, 6th June, 13th June and 20th June – Preliminary membership lists (reflecting any updates) posted to the website after 6 PM US eastern time.

Monday 9th June – “Lock-down” period begins with the updates to reconstitution membership considered to be final.

Friday 27th June – Russell Reconstitution is final after the close of the US equity markets.

Monday 30th June – Equity markets open with the newly reconstituted Russell US Indexes.

Catherine Yoshimoto, Director, Product Management at FTSE Russell, said:

“Due to the ever-evolving nature of the US equity market, it’s crucial to fully recalibrate the suite of Russell US Indexes, ensuring the indexes maintain an accurate representation of the market, including changes in company size and style shifts since the last rebalancing. This process culminates in one of the highest trading volume days of the year, with investors benefiting from a seamless and reliable experience that’s facilitated by our transparent, rules-based methodology and timely communication of preliminary index membership changes.”

On 21st February 2025, FTSE Russell announced the 1Q2025 preliminary list of IPO additions, which will take effect at the market open of 24th March. As of 1Q2025, there is one preliminary addition to the Russell 1000 Index and seven additions to the small cap Russell 2000 Index. There will also be six IPOs added to the Russell Microcap Index.

The reconstitution and quarterly IPO additions provide an important foundation for FTSE Russell’s widely used Russell US Indexes. These governance processes are designed to ensure the indexes remain a current and relevant measure of US equity market performance.

Although currently rebalanced on an annual basis, FTSE Russell announced in January that the reconstitution of the Russell US Indexes will be held semi-annually in June and November beginning in 2026. This decision is based on data analysis and follows a market consultation undertaken in response to the recent evolution of market dynamics. More on the Russell US Indexes moving to a semi-annual reconstitution next year can be found on the FTSE Russell website here.

In addition, in response to market concentration and in consideration of US RIC diversification limits, beginning with the March 2025 quarterly index review, Russell US Style Indexes will apply a capping methodology on a quarterly basis. FTSE Russell will also continue to calculate the Russell US Style Benchmark indexes, which will continue to reflect uncapped weights.

FTSE Russell is a global index leader that provides innovative benchmarking, analytics and data solutions for investors worldwide. FTSE Russell calculates thousands of indexes that measure and benchmark markets and asset classes in more than 70 countries, covering 98% of the investable market globally.

FTSE Russell index expertise and products are used extensively by institutional and retail investors globally. Approximately $15.9 trillion is benchmarked to FTSE Russell indexes. Leading asset owners, asset managers, ETF providers and investment banks choose FTSE Russell indexes to benchmark their investment performance and create ETFs, structured products and index-based derivatives.

A core set of universal principles guides FTSE Russell index design and management: a transparent rules-based methodology is informed by independent committees of leading market participants. FTSE Russell is focused on applying the highest industry standards in index design and governance and embraces the IOSCO Principles. FTSE Russell is also focused on index innovation and customer partnerships as it seeks to enhance the breadth, depth and reach of its offering.

FTSE Russell is wholly owned by London Stock Exchange Group.

FTSE Russell® is a trading name of FTSE, Russell, FTSE Canada, FTSE FI, FTSE FI Europe, WOFE, RBSL, RL, and BR. “FTSE®”, “Russell®”, “FTSE Russell®”, “FTSE4Good®”, “ICB®”, “Refinitiv” , “Beyond Ratings®”, “WMR™” , “FR™” and all other trademarks and service marks used herein (whether registered or unregistered) are trademarks and/or service marks owned or licensed by the applicable member of LSEG or their respective licensors and are owned, or used under licence, by FTSE, Russell, FTSE Canada, FTSE FI, FTSE FI Europe, WOFE, RBSL, RL or BR. FTSE International Limited is authorised and regulated by the Financial Conduct Authority as a benchmark administrator. Refinitiv Benchmark Services (UK) Limited is authorised and regulated by the Financial Conduct Authority as a benchmark administrator.

All information is provided for information purposes only. All information and data contained in this publication is obtained by LSEG, from sources believed by it to be accurate and reliable. Because of the possibility of human and mechanical inaccuracy as well as other factors, however, such information and data is provided “as is” without warranty of any kind. No member of LSEG nor their respective directors, officers, employees, partners or licensors make any claim, prediction, warranty or representation whatsoever, expressly or impliedly, either as to the accuracy, timeliness, completeness, merchantability of any information or LSEG Products, or of results to be obtained from the use of LSEG products, including but not limited to indices, rates, data and analytics, or the fitness or suitability of the LSEG products for any particular purpose to which they might be put. The user of the information assumes the entire risk of any use it may make or permit to be made of the information.

No responsibility or liability can be accepted by any member of LSEG nor their respective directors, officers, employees, partners or licensors for (a) any loss or damage in whole or in part caused by, resulting from, or relating to any inaccuracy (negligent or otherwise) or other circumstance involved in procuring, collecting, compiling, interpreting, analysing, editing, transcribing, transmitting, communicating or delivering any such information or data or from use of this document or links to this document or (b) any direct, indirect, special, consequential or incidental damages whatsoever, even if any member of LSEG is advised in advance of the possibility of such damages, resulting from the use of, or inability to use, such information.

No member of LSEG nor their respective directors, officers, employees, partners or licensors provide investment advice and nothing in this document should be taken as constituting financial or investment advice. No member of LSEG nor their respective directors, officers, employees, partners or licensors make any representation regarding the advisability of investing in any asset or whether such investment creates any legal or compliance risks for the investor. A decision to invest in any such asset should not be made in reliance on any information herein. Indices and rates cannot be invested in directly. Inclusion of an asset in an index or rate is not a recommendation to buy, sell or hold that asset nor confirmation that any particular investor may lawfully buy, sell or hold the asset or an index or rate containing the asset. The general information contained in this publication should not be acted upon without obtaining specific legal, tax, and investment advice from a licensed professional.

The Securities and Exchange Commission today announced it will hold a roundtable discussion on Artificial Intelligence in the financial industry. The event takes place on March 27 from 9 a.m. to 4 p.m. at the SEC’s headquarters in Washington, D.C. and is open to the public for either in-person or virtual attendance.

The AI roundtable will discuss the risks, benefits, and governance of AI in the financial industry.

SEC Acting Chairman Mark Uyeda and SEC Commissioners Hester Peirce and Caroline Crenshaw are expected to deliver remarks.

Advance registration is strongly encouraged for those planning to attend in person.

Information on the agenda, participants, and the process for the public to submit comments will be published on the SEC AI Roundtable’s event page.

As the securities industry continues to break out of silos and vertical business models, lines are blurring between asset classes, front-, middle- and back-office functions, and geographic markets.

To more closely align its offerings with an evolving marketplace, Trading Technologies is advancing its “multi-X” factor, with X representing asset class, function and region.

Traders Magazine caught up with TT Chief Operating Officer Justin Llewellyn-Jones (“JLJ”) to learn more.

What compelled you to join Trading Technologies in early 2024?

There were three main trigger points for why I joined TT.

The first was TT’s vision and strategy.

TT has been a leader in the futures and options markets, particularly in execution, for 30 years. While this remains a core focus, our vision has expanded to what I call “multi-X.” This means we are evolving our platform and network to be multi-asset, multi-geography, multi-workflow, and multi-function.

Justin Llewellyn-Jones

Financial services software developed in the 80s, 90s, and 2000s was typically designed for a specific business purpose, such as trading equities in the US, providing compliance in Europe, or clearing futures in Japan. While this approach met specific business requirements with targeted technology solutions, it led to inefficiency and duplication, because many of these solutions fundamentally perform the same functions, resulting in a fragmented ecosystem.

Keith Todd, TT’s CEO, has always envisioned consolidating trading solutions into a single platform and streamlining front-to-back trade processing. By using multi-X solutions to reduce fragmentation, risk, and cost, his goal has been to drive both efficiency and productivity. Keith’s vision has been a broader industry theme for many years, and I share it. I believe TT is best positioned to execute on this vision, acting as a catalyst for electronification and automation by enabling all asset classes to utilize the most optimized tools and workflows.

The second trigger point was the underlying technology.

I’ve been building solutions for the financial services industry for three decades, and I know that legacy technology is deeply entrenched in capital markets. Some solutions still in use were built as far back as the 70s and remain on mainframe technology. While the old adage “if it ain’t broke, don’t fix it” has its place, legacy technology makes it harder to leverage advancements like AI and cloud computing and to embrace the open, componentized ecosystems that are now standard.

As many people know, TT underwent a massive technology modernization program between 2011 and 2021, becoming one of the first vendors to embrace the Cloud. While there were certainly challenges and setbacks along the way, and we continue to enhance and optimize the platform with ongoing initiatives, we now have a cloud-native, componentized, and service-oriented architecture that allows us to take full advantage of current technological advances. This architecture also enables us to provide the open ecosystem that our customers want and readily integrate third-party solutions.

At some point everyone sitting on legacy technology solutions is going to have to go through the same modernization process, so joining an organization that had put the time and effort into modernizing their technology stack was incredibly attractive to me.

The third trigger point was the people.

The TT team is truly exceptional, composed of dedicated and hard-working individuals who are laser-focused on our customers and share a common goal: to build products that not only meet but exceed customer expectations, fostering growth and success. Furthermore, they are committed to providing outstanding customer service, and continually improving service excellence.

How could I not join TT when I saw that it had the right vision, the right technology and the right people?

Our goal is to provide comprehensive support for the core trade lifecycle across all asset classes and jurisdictions. This encompasses areas such as execution, order management, risk management, middle office, and clearing. Additionally, we recognize the critical importance of adjacent activities such as margin management, trade surveillance, trade and transaction reporting, real-time quantitative analysis for algorithm optimization, and so on. These interdependent elements must all operate seamlessly to deliver the highest levels of straight-through processing for our customers. When properly implemented, they also generate holistic data insights and feedback loops, enabling customers to continuously enhance their trading activities.

The lack of interoperability between different solutions is a real obstacle. For instance, in trade surveillance, many firms currently use multiple solutions to monitor their trading activity across various asset classes and regions. These solutions are usually linked to separate execution solutions. If you have a multi-asset execution solution that is integrated with a multi-asset surveillance solution, you can use surveillance models that are not only single-asset and multi-asset, but also single-market and cross-market, and single-product and cross-product.

That’s the essence of what we’re trying to do with multi-X. It’s not just about multi-asset execution, it’s also about these adjacent activities, where if you bring it all together, you get a much better oversight of your activity while reducing risk and cost, and an ability to really optimize.

What is the importance of interconnectivity in this context?

Many firms employ trading strategies that cover multiple asset classes, even if only for hedging purposes. So asset class interconnectivity exists and has always existed. What TT is doing is eliminating the “swivel effect” of having to interact with multiple solutions, and making it that much easier for people to execute their trading strategies efficiently. I think of this as horizontal interconnectivity.

The other vector of interconnectivity is vertical, occurring across the trade lifecycle and value chain. Modern, componentized solutions with higher levels of interoperability allow firms to build their own ecosystems, even building new or modernizing existing solutions. As the trade lifecycle evolves and shortens, as seen with Equities and T+1 settlement or Treasuries and centralized clearing, firms require this agility.

With our multi-X strategy, TT is well-positioned to assist firms with these needs and evolutions. Additionally, we can enable modernization programs by allowing firms to leverage our platform, network, and distribution.

TT will be represented at next week’s FIA Boca, which turns 50 this year. What’s the importance of this event?

The FIA does a fantastic job of bringing the industry — banks, brokers, buy-sides, vendors – together for constructive discussions and to make progress on optimizing the market structure, and they deserve kudos for what they’ve achieved since their founding in 1955. Over the last 50 years the FIA Boca event has brought together all of the players in the industry for a few days every year to discuss the most compelling issues.

With TT’s 30 years of working in futures and options, FIA Boca has a special place in our hearts when it comes to everything we have achieved so far, and will continue to be where we engage with our customers and the broader industry to discuss our collective vision for the future.

Optiver has appointed Lance Braunstein as Global Chief Technology Officer, effective May 1, 2025. Braunstein will join as a member of the Executive Committee and Partner, based in the New York office. In this newly-created role, reporting to CEO Jan Boomaars, he will drive a unified global technology strategy across business lines and regions, working closely with regional CTOs. Most recently, Braunstein served as Head of Aladdin Engineering at BlackRock, overseeing the design, product management, development and operation of the firm’s investment management technology platform. He has also held senior technology leadership roles at Goldman Sachs and Morgan Stanley.

Ryan Mitchell has been promoted to Senior Managing Director Coda Markets at Global Liquidity Partners. In his new role, Mitchell will oversee all daily operations for Coda, reporting directly to Tim Lang, CEO. Also joining Coda Markets in key sales and operations roles are Zack Wilezol and Chris Barrus.

Billy Obregon

Billy Obregon has been appointed Head Private Clients Americas and CEO of Vontobel Swiss Financial Advisers (SFA), effective March 1, 2025. Based in New York, he brings over 20 years of experience in the financial industry, most recently from his position at Deutsche Bank, where he was responsible for covering U.S. and Latin American clients.

Clearwater Analytics has added Yuriy Shterk as Global Head of Alternatives. Shterk brings a wealth of expertise and client experience from his 25-year career in the capital markets. He has held leadership roles driving product and solution innovation for the private markets, derivatives, and the broader alternative assets market. Prior to joining Clearwater, Shterk served as Chief Product Officer at Allvue Systems, where he was responsible for growing product lines and revenue streams for private markets.

Quantexa has appointed Stuart Riley to its board of directors. Riley, who currently serves as Group Chief Information Officer at HSBC and as a member of its Group Operating Committee, will replace current board member Colin Bell. As Group CIO at HSBC, Riley leads the bank’s global technology strategy, driving innovative, resilient, and customer-focused digital solutions.

Chatham Financial has appointed Lorelei Lenzen as Chief Marketing Officer. Lenzen is an accomplished marketing executive with more than 25 years of experience. She brings a proven track record of leading brand evolution and client engagement at global organizations in the financial services sector, including BNY, Enfusion, EY, and the New York Stock Exchange.

If you have a new job or promotion to report, let me know at alyudvig@marketsmedia.com

Rapid ideological, geopolitical and technological changes are creating a noisy and uncertain world, challenging traditional approaches and conventional wisdom across all sectors of the global economy. In such times, it becomes more important than ever to start from first principles when running a compliance program.

For compliance teams, a fundamental function is to build systems and processes that can find the right signals in the noise, unique to facts and circumstances.

Yet growing complexity across marketplaces threatens to overwhelm firms with interference. By exploring emerging trends – namely the potential for lighter-touch regulation, increasing demand for clarity across digital asset markets, and the growing power of artificial intelligence (AI) – it is clear that finding the signal demands a fresh capacity for flexibility and innovation across the surveillance function.

Responding to shifting enforcement environments

As governments across the world look to promote growth and competitiveness, the regulation of various industries is coming under scrutiny – especially financial services. The new Trump Administration is widely predicted to prioritize a broad agenda of deregulation amid leadership changes across federal agencies. The United Kingdom (UK) is eyeing the relaxation of financial crisis-era demands. Even the European Union (EU) is embarking on a process of “simplification.”

While this would suggest that existing efforts can ease, experience shows that deregulation often manifests as compliance “whack-a-mole” – where decreased enforcement in one area diverts attention and energy to other (often unanticipated) avenues.

Similarly, enforcement priorities can change very quickly amid the shifting sands of political expediency and public opinion. Issues at individual firms or market-wide black swan events can also trigger swift course corrections if there are perceived regulatory gaps. Longer-term, history has consistently demonstrated that periods of deregulation are often followed by renewed, more intensive scrutiny.

Put simply, the need for compliance teams to prioritize robust and proactive surveillance programs to guard against regulatory and reputational risk both now and in the future remains as important as ever. However, firms must also now navigate the prospect of doing more with less to cover an array of potential scenarios.

Increasing regulatory clarity for digital assets

It is also important to recognize that deregulation is in no way a universal trend. This is perhaps most evident across digital asset markets, where increasing consumer and institutional adoption has created strong momentum and support for clearer regulatory approaches and guidelines.

The introduction of the EU’s Markets in Crypto-Assets (MiCA) regulation – which came into force in December – is widely viewed as providing a regulatory framework that stands to be replicated across other jurisdictions. In the United States, new policy ambitions for digital assets seem to be ultimately aimed at bringing increased clarity after several years of flip-flopping and uneven enforcement. Ongoing consultations in the UK and Asia-Pacific also point towards more robust oversight.

It is unclear at this stage exactly how evolving regulatory approaches across the globe will impact competitiveness and enforcement at the jurisdictional level. What we do know is that firms will need flexibility to address the complexity and risks of meeting emerging rules and obligations across their multi-jurisdictional operations.

Harnessing the potential of AI

Faced with growing complexity and ongoing resource constraints, many firms are now actively exploring the use of AI to improve performance, unlock efficiencies and reduce costs.

When deployed effectively, the upside is transformative. AI tools allow firms to cast a wider net and capture more data, enabling them to accurately detect problematic behavior and patterns across markets and products – without overloading teams with alerts. AI also promises to automate labor-intensive manual and repetitive processes, freeing up resources to focus on higher-value activities.

Yet uncertainty around the potential downsides lingers. Despite the potential, hype and investment have far outpaced adoption and utility to date – with an estimated 80% of all AI projects failing. The reasons are varied, but inadequate risk controls and accountability are common challenges. Deployments are also being hamstrung by poor underlying data quality, which raises the risks of hidden biases and false and misleading information resulting in outright bad decision-making.

Given the recent shift in regulatory focus toward internal processes and controls, it is imperative that appropriate safeguards are in place to ensure that decisions are fully explainable and auditable. For example, if an alert is closed, firms must be able to demonstrate to regulators the considerations informing the calibration, the data used and the reason for closure.

Firms must also continue to ensure they are on top of their data. Over the past year, the threat of massive fines for lapses in data governance has served as strong motivation for firms to ensure complete, accurate data from all their trading systems finds its way into surveillance programs. While good progress has been made, the opportunity to realize maximum value from AI is a compelling reason to redouble efforts.

Finding signal in the noise

As we look ahead to 2025 and beyond, the only thing that seems certain is that uncertainty will remain.

Amid such instability and volatility, it is easy for the noise to drown out what is important. Challenges are compounded by the limitations of legacy surveillance solutions, which are increasingly overwhelmed by the highly complex and rapidly evolving nature of marketplaces around the world.

The good news is that modern surveillance platforms are helping firms find the signals in the noise and tune in to what really matters to them. The flexibility to deploy solutions quickly and cost-effectively to address specific, evolving needs – combined with complete coverage, comprehensive data ingestion and intelligent automation – is empowering firms with the clarity and focus to meet the moment.

Congressional Stock Trading: What Can an SEC Chair Do?

By Jim Toes, STA President and CEO

Paul Atkins will soon testify before the Senate Banking Committee for his potential SEC Chairman nomination, with no set date. If approved, a full Senate vote could confirm him within three weeks.

In addition to facing questions on his regulatory philosophy, enforcement priorities, and the SEC’s mandate: protecting investors, ensuring fair markets, and supporting capital formation, Atkins will face more specific inquiries. In this second of a multi-part series about the topics he will most likely face, we highlight the limitations that the SEC has in policing stock trading by government officials.

Congressional stock trading continues to captivate and confound the American public, raising persistent questions about fairness and accountability in government. Every day, we learn about these occurrences through a steady drip of financial disclosures mandated by the Stop Trading on Congressional Knowledge Act (STOCK Act) of 2012 shared via platforms like X, news outlets, and watchdog organizations that scrutinize trading reports for suspicious patterns. Yet, despite this transparency, many wonder why such behavior is seemingly allowed to persist, especially when the same actions would land private citizens in legal jeopardy.

For those of us in the financial industry, frustration and anger run very high. In our jobs, we face strict regulations on trading stocks in our personal accounts. We’re subject to pre-clearance requirements, before executing trades, and holding period rules, which prevent quick buy-and-sell transactions to avoid short-term speculation. Additionally, we are restricted from trading stocks of companies where we have material non-public information, which for anyone on a trading desk includes every company under the sun. These policies are monitored with great proficiency and when violated individuals face severe consequences in the form of fines and lifetime bans from our industry. These regulations and industry standards prevent the occurrence and perception of widespread insider trading.

The STOCK Act mandates federal government officials to disclose their financial transactions within 45 days and prohibits them from using material non-public information for personal profit. While the STOCK Act applies to all federal officials, it is not equally administered. Many three-letter agencies like the FDA, FCC, IRS and others have discretion on what is demanded among their staff, which leads to inconsistent levels of transparency. Reporting standards by congressional members is stricter with information on trades more easily found in the public domain. This is why almost all the attention is on them.

Today, there is widespread skepticism about the efficacy of the STOCK Act in restoring public trust. Enforcement has been virtually nonexistent due to significant challenges within the legal framework. Investigating and proving intent, as well as a breached duty of trust, is nearly impossible and often leads to a political minefield. One major legal obstacle is the Speech and Debate Clause—a constitutional provision that grants members of Congress immunity from prosecution for actions or statements made in the course of their legislative duties—which hinders regulatory agencies’ investigations. Another barrier is the lack of direct authority over Congress; while the SEC can investigate individual members, it lacks explicit power to regulate or discipline them, leaving enforcement to the Department of Justice or congressional ethics committees. That said, the STOCK Act has successfully increased transparency in an area where none previously existed.

SEC Chairs face significant limitations in policing insider trading by members of Congress, making it difficult to find meaningful courses of action within those constraints without additional authority from Congress. Until such reforms are enacted, public frustration is likely to persist, underscoring the urgent need for legislative action to close these loopholes and restore faith in governmental integrity.