Sally Bartunek, trader at Ninety One, discusses the main takeaways from the market’s reaction to the US election results, in addition to the US Federal Reserve’s and Bank of England’s decision to cut interest rates by 25 basis points. She looks at how fixed-income markets performed and where she saw surprises in emerging markets.

In this episode, Bartunek unpacks how she trades and strategizes “a game plan” during highly volatile events. Looking ahead, Bartunek discusses how trading desks could approach the final few weeks of 2024, as they wrap up the year.

(EXECUTION MATTERS is a Traders Magazine content series focused on the topics most important to traders and technologists in US equities and options markets. EXECUTION MATTERS is produced in collaboration with Lime Trading Corp.)

Innovation, both in technology and in product offerings, is increasingly empowering retail traders, boosting a segment that has more than doubled its presence in the market since the early 2010s.

Whether it’s a more intuitive trading app with greater functionality, more targeted hedging and risk management vehicles, or expanded trading hours, the financial services industry is enabling novices to participate in markets for the first time, and also helping more experienced retail traders level up to be more active and self-directed, with a toolkit that can rival institutional capabilities.

Retail traders’ share of stock market trading volume increased from just above 10% in 2011 to more than 22% in 2021, according to Bloomberg Intelligence data cited by Forbes. Retail trading share in the options market is well above 40%. The ‘meme stock’ craze peaked in 2021 and retail trading has leveled off since then, but the absence of a significant market decline and a much-improved user experience have kept many retail players involved.

Market participants and observers say the industry’s focus on expanding and improving education has helped retail investors, as have technological advancements. For trading platform operators, the rise of the retail trader is an opportunity to gather more order flow, but it’s also a challenge to meet the demands of this much-more sophisticated market participant.

“Retail has become smarter, trading various types of strategies which could include ETFs and options, in combination with single stocks,” said Johan Sandblom, President and Head of Business Development at Lime Trading Corp, an agency-only broker-dealer providing low latency market access to the U.S. equities and options markets.

Johan Sandblom, Lime Trading

“Individual investors also have a better understanding of the US market structure,” Sandblom continued. “They are asking questions around the quality of the execution rather than just accepting a ‘free’ trade, and they are requiring more from their broker in order to execute their strategies efficiently.”

In a September 2024 blog post, Cboe Global Markets CEO Fred Tomczyk noted that retail traders have been a major growth engine in the options market over the past several years, and that can continue as long as the financial services industry continues to be good stewards.

“The options trading ecosystem is supported by a diverse range of participants who each play an important role in the market’s functionality and stability,” Tomczyk wrote. “As members of the financial services industry, it is our job — first and foremost — to provide trusted systems that enable people to confidently participate in the markets and economy. With that foundation set, our responsibility is to empower and educate people to participate in those systems to the best of their ability.”

Product innovation and the transformative impact of technology and education for retail were discussed at the Security Traders Association’s 91st Annual Market Structure Conference, which was held in Orlando, Florida in September.

In the panel Continued Democratization of Retail Investing, it was stated that competition between retail trading platforms generates constant improvements to the retail experience, with innovation in areas such as options products, fractional shares and ‘24/5’ trading.

Importantly, the panel noted an increase in active traders who are comfortable trading and actively managing their portfolios around major news events – these market participants are being provided sophisticated tools and more products to better construct their portfolios. The industry must continue to meet the needs of the retail trading segment as these participants continue to gain knowledge and sophistication.

“We now hear questions from retail about what type of application programming interfaces (APIs) are offered for their automated strategies, what order capacities are, questions around various order types, how orders are processed, what latencies are, and how all of it impacts their overall execution,” Lime Trading’s Sandblom said.

Added Sandblom: “For Lime, the transition to a more sophisticated retail trader has been very smooth. Our system was initially built for professional sophisticated traders – we have made this same technology available to the retail market, with several ways to direct their order flow to various markets.”

Prudential Financial has appointed Jacques Chappuis as president and CEO of PGIM, its $1.4 trillion global investment management business, effective May 1, 2025. Chappuis will report to Andrew Sullivan, head of International Businesses and Global Investment Management for Prudential Financial. He succeeds David Hunt, who will retire as president and CEO and stay on as chairman of PGIM until July 31, 2025, remaining actively involved throughout the transition period. With nearly 30 years of investment management experience, Chappuis joins PGIM from Morgan Stanley, where he was most recently co-head of Morgan Stanley Investment Management. At MSIM, he played a key role in the transformative and successful integration of Eaton Vance. From 2006 to 2013, he held senior leadership roles in Morgan Stanley’s Investment Management and Wealth Management businesses.

Terry Duffy

CME Group has extended Chairman and Chief Executive Officer Terry Duffy‘s contract through December 31, 2026. The company also announced Lynne Fitzpatrick will take on the expanded role of President and Chief Financial Officer. Additionally, its Chief Operating Officer Julie Holzrichter has decided to step down from her role to begin serving as an advisor to the company. Suzanne Sprague will succeed Holzrichter as Chief Operating Officer and Global Head of Clearing. Sprague, who has served as Senior Managing Director and Global Head of Clearing and Post-Trade Services since 2022, joined CME Group in 2002. She has served in a range of leadership positions in financial and risk management since that time, including Managing Director, Credit & Liquidity Risk, Risk Policy & Banking.

Tom Darnowski

Tom Darnowski has been promoted to Schroders CEO Americas, effective January 1, 2025. Darnowski has been with Schroders for over ten years and most recently served as the firm’s Global Head of Product Strategy, where he oversaw Schroders’ global product range and explored innovative ways to meet client needs. Prior to this role, he served as Head of Product Development, North America, and eventually of the Americas. He joined Schroders in 2013 from The Hartford, a U.S.-based investment and insurance company.

Blackstone has announced that Chris James – currently Chief Operating Officer (COO) and a founding member of Blackstone Tactical Opportunities (Tac Opps), with nearly two decades of experience at Blackstone – will become Global Head of Tac Opps. He will succeed David Blitzer, who will transition to chairman of the business at year end. Blackstone has also announced the elevation of two long-time senior Tac Opps partners to expanded leadership roles for the business. Jas Khaira will be Head of Tactical Opportunities Americas and Qasim Abbas will be Head of Tactical Opportunities International.

MarketAxess Holdings has announced that Founder and Executive Chairman Rick McVey will retire at the end of the year. McVey stepped down as CEO of MarketAxess in April 2023 after 23 years in that role, and has since been serving as Executive Chairman of the Board. Carlos Hernandez will succeed McVey as Chairman of the Board of Directors, effective January 1, 2025. McVey has agreed to remain as the Chairman of the Board of Directors of MarketAxess, the Company’s international holding company.

If you have a new job or promotion to report, let me know at alyudvig@marketsmedia.com

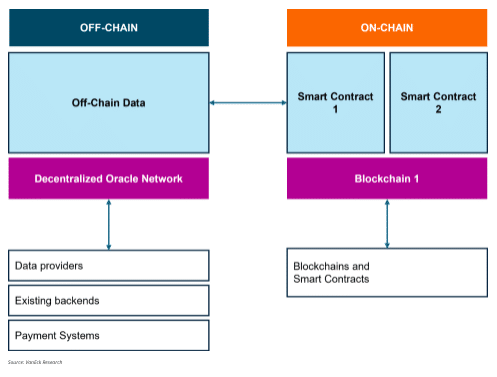

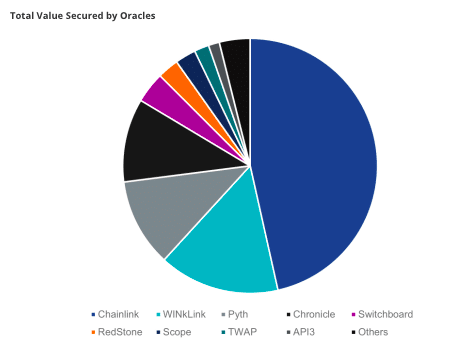

The Pyth network has introduced a staking system to reward contributors for the quality of their data as the decentralized blockchain-based distribution platform aims to make financial market data across asset classes cheaper, and more accessible.

Timely and accurate market data has historically only been available to institutions who can afford to pay for direct connectivity to exchanges, vendors or other providers.

Pyth was launched to find a better ways to make financial market data available on blockchain to projects and protocols using smart contracts, as well as to the general public. Mike Cahill, chief executive of digital asset infrastructure provider Douro Labs and a core contributor to Pyth, told Markets Media tha the network was designed to solve the oracle problem in blockchains.

On a blockchain, trust or verification from the user is not needed because data is stored on a decentralised ledger with global consensus. However blockchains need a way to securely access some off-chain data, such as asset prices which are constantly changing. Oracles were designed to provide secure access from blockchains to off-chain data using smart contracts to connect to external data providers.

Menno Martens, crypto specialist and product manager at fund manager VanEcK , described the Pyth network in a report on 5 November 2024 as a high-frequency oracle using Solana blockchain technology. This offers a robust solution for off-chain data sharing for primarily decentralized finance applications (DeFi), and provides services such as real-time price feeds and benchmarks. VanEck has a Pyth exchange-traded note.

Source: VanEck

“Pyth’s data pull model provides data directly from the source, such as exchanges, market makers or DeFi protocols,” added Martens. “Because data is pulled only on demand and not pushed at a given interval, it scales efficiently, and costs are offloaded to users where updates are demand-based.”

Cahill said Pyth was designed to allow DeFi to compete with the traditional financial world by having the lowest possible latency and cost, and run as efficiently as possible. The initial pitch for the network was to approach high-frequency traders and highlight that they had valuable data which could be contributed to this blockchain project to solve the oracle problem.

“We are able to generate a very high quality but zero-cost data stream,“ Cahill added. “This revolutionizes how people think about data and is completely orthogonal to the existing data economy, because we are relying on this found resource from so many different trading firms.”

Doug Cifu, Virtu Financial

Pyth began by approaching the biggest trading firms and some of the largest exchanges, but now has a comprehensive set of about 110 contributors across 550 symbols, according to Cahill. For example, in 2021 market maker Virtu Financial began to contribute financial market data across equities, foreign exchange, futures, and cryptocurrencies to Pyth. Douglas Cifu, chief executive of Virtu Financial, said at the time that with growing support from the trading community, the Pyth Network would become an integral piece of infrastructure in the evolving DeFi ecosystem,

In 2022 Cboe Global Markets became the first major global exchange operator to join the Pyth Network and contribute real-time, derived market data, starting with 10 symbols from one of its four US equities markets. This year Laser Digital, the digital asset subsidiary of Japanese bank Nomura, became an institutional data provider across crypto, equities, commodities, and FX.

“From the very beginning, the idea around who should publish on this network was the only trust it had,” added Cahill. “So they are institutions who have got too much reputation to lose than they have to gain by manipulating data.”

In order ensure the quality of the data there are mechanisms in place such as never having just one publisher in a symbol and needing a minimum of 10 publishers in order to generate an aggregate. Cahill said: “We have made some refinements, and think we will be able to scale those numbers up tremendously over the next several months.”

Pyth has just rolled out oracle integrity staking which Cahill described as adding economic trust to the network. Providers are incentivized to help maintain data quality by receiving rewards from an open-ended pool. However, they also face the risk of having their stake slashed as a penalty for failing to maintain data accuracy.

“Imagine this sci-fi world where you have everything that is traded reports its price to Pyth because we have incentivized all the traders to earn rewards,” said Cahill.

Users can see on-chain how much each publisher has been rewarded for providing the highest quality data, and validators can also receive a portion of the rewards.

Mike Cahill, Douro Labs

“Using these game theory mechanisms can reinforce the outcome for higher quality,” Cahill. “Pyth is designed to optimise trust at speed, which is vitally important for financial services.”

Pyth price feeds currently update every 400 milliseconds according to Cahill, which is very fast for blockchains but relatively slow for institutional finance who operate in microseconds, or sometimes nanoseconds.

“The end goal is to get all symbols on Pyth as close to T0 as possible,” he added. “The roadmap is to make things faster, make more data available and keep it very cheap.”

Cahill has ambitions that as Pyth starts to scale up into the many thousands, hundreds of thousands or millions of symbols, it will become an alternative to visual data for traders, which has historically been prohibitively expensive.

“Projects like OpenBB are already plugged into Pyth data and they are making it available to retail traders who have relied on 15-minute delayed data,” he added. “This is a global project and we think that giving equal access to everyone is a huge endeavor, which will be a game changer.”

Pyth data has also been integrated with TradingView, which allows users to view Pyth prices on their own website. Cahill said: “We are very aligned to being able to make data available everywhere.”

Data is currently available on 80 different blockchains in 425 applications, and has been used by 65% on-chain derivatives markets, according to Cahill. He said close to $1 trillion of volume in derivatives have been executed at the Pyth price over the network’s lifetime.

Source: VanEck

Market data pricing

In traditional finance, market participants have raised concerns about the cost of market data. Trade bodies including The Association for Financial Markets in Europe (AFME) and EFAMA, the European Fund and Asset Management Association, issued a joint statement on significant issues with the supervision of market data costs in October this year.

They told regulators that proposed new regulation does not ensure that the pricing of market data must be based on the actual cost of production and dissemination with a reasonable margin, bearing in mind that market data is a by-product of the trading activity.

“The present proposal will, if not changed significantly in line with the associations proposals, imply that the trend of considerably increasing costs of market data and complexity of terms & conditions will continue to exist to the detriment of the key-stakeholders in the capital markets meaning investors and pension savers will face less investment choices, less transparency, higher costs, lower savings, and companies may face reduced access to capital and higher cost of capital,” they said.

SEC Charges Invesco Advisers for Making Misleading Statements About Supposed Investment Considerations

Washington D.C., Nov. 8, 2024 —

The Securities and Exchange Commission today charged Invesco Advisers, Inc. for making misleading statements about the percentage of company-wide assets under management that integrated environmental, social, and governance (ESG) factors in investment decisions. The Atlanta-based registered investment adviser agreed to pay a $17.5 million civil penalty to settle the SEC’s charges.

According to the SEC’s order, from 2020 to 2022, Invesco told clients and stated in marketing materials that between 70 and 94 percent of its parent company’s assets under management were “ESG integrated.” However, in reality, these percentages included a substantial amount of assets that were held in passive ETFs that did not consider ESG factors in investment decisions. Furthermore, the SEC’s order found that Invesco lacked any written policy defining ESG integration.

“As stated in the order, Invesco saw commercial value in claiming that a high percentage of company-wide assets were ESG integrated. But saying it doesn’t make it so,” said Sanjay Wadhwa, Acting Director of the SEC’s Division of Enforcement. “Companies should be straightforward with their clients and investors rather than seeking to capitalize on investing trends and buzzwords.”

The order charges Invesco with willfully violating the Investment Advisers Act of 1940. Without admitting or denying the order’s findings, Invesco agreed to cease and desist from violations of the charged provisions, be censured, and pay the aforementioned $17.5 million civil penalty.

The SEC’s investigation was conducted by Jonathan T. Menitove of the Asset Management Unit and Richard Rodriguez of the Atlanta Regional Office with assistance from Robert K. Gordon. It was supervised by Ruth Hawley of the San Francisco Regional Office, Stephen E. Donahue of the Atlanta Regional Office, and Andrew Dean and Corey Schuster of the Asset Management Unit.

FLASH FRIDAY is a weekly content series looking at the past, present and future of capital markets trading and technology. FLASH FRIDAY is sponsored by Instinet, a Nomura company.

With ESMA recently reiterating the importance of harmonisation of shortening settlement cycles across Europe, it in effect signalled an appetite to move in sequence with the UK (provisionally end of December 2027 per task force recommendations) and Switzerland.

James Maxfield, Duco

While nothing has been set in stone, these signals will trigger strategic and tactical planning across the post trade ecosystem in Europe, looking at readiness for just over two years’ time. While that may seem like a long time, the reality is most will need to be thinking about budgets and timelines immediately.

The impact of the recent T+1 shift in North America and the lessons learned from it were a key theme at the recent AFME OPTIC conference in London. What Europe and the UK should look to do differently in terms of preparation was a key focus. There was a lot of good discussion across the different participants but here are the top 5 things the industry needs to be thinking about.

1. Cash continues to be king

Much has been made of the margin benefit that both sell-side and custodians took from the shift to T+1, with a 30% reduction in clearing margin. However, this has come at the expense of funding inefficiency for the rest of the market, with much of the buy-side noting an increase in funding costs as a result of the reduced settlement window.

SWIFT was one of the panellists at AFME OPTIC, and noted that while buy-side FX payment volumes have gone up as a result of the move to T+1, the average size has decreased. This indicates a loss of efficiency in cash management overall as a result of more frequent trading in smaller sizes.

The cost and operating model considerations of expanding the scope of T+1 to a wider universe of currencies and assets shouldn’t be underestimated. This creates both a challenge for the industry and also an opportunity for service providers to play a more global role in insulating participants from this effect.

Custodians and service providers bringing together settlement processing, cash management and funding into a 24/7 model will become increasingly attractive. But they will need to show value – operationally, commercially and from a client service perspective – which hasn’t always been the case and has led to the current fragmented processes.

2. Affirmation, affirmation, affirmation

The role of the affirmation process has undoubtedly contributed significantly to the lack of market disruption from the move in the US. This was a relatively new concept for many outside of the US, but its value in driving settlement discipline has been clear to see.

Driving adoption as part of the march to T+1 however will be much harder within the UK and the rest of Europe, as it will require regulators and the industry to agree on the right framework that incentivises take up (and dis-incentivises non-compliance). This is easy to say, but much harder to do in practice, and locking effective affirmation processes into the migration timeline will require intensive collaboration.

3. Securities lending is a game of moving parts

The relative lack of automation, allied to the global nature of liquidity pools within securities lending, created a major cause for concern with the move to T+1 in the US. While the key metrics – fail rates as an example – would imply there hasn’t been much market impact, the reality is that liquidity has reduced as a result of the need to maintain higher inventory buffers and a general risk reduction across trading desks. 50% of the industry are now citing securities lending as the single biggest impact of the move to T+1, which has increased from 33% 12 months ago. (Citi Securities Services Evolution 2024)

The marketplace across the UK and Europe is much more complex than the US – different taxation regimes, business models like synthetic prime brokerage, ETF complexity, investor behaviour – and securities lending is a critical component of efficient market practice.

The role of collateral mobility, both to support trading activity as well as margin and funding, is critical to enabling these businesses. But though the growth of tri-party providers and automation solutions has increased over the last decade, the market is still heavily reliant on people and legacy processes to make it function.

It is hard to imagine that an equivalent reaction in terms of liquidity and risk appetite won’t fundamentally alter the economics of doing business. So being able to efficiently mobilise collateral across a wide spectrum of uses, locations, clients and business units will become a critical piece of the puzzle.

4. Automation everywhere (or not actually)

While the role of the affirmation process in driving smooth implementation in the US has been well publicised, what is less obvious is how participants have actually achieved dealing with compressed timelines.

The perception that the industry was in part ‘throwing people at the problem’ vs re-engineering systems and processes has been borne out by some of the recent industry feedback. 31% of the industry confirmed they had achieved compliance by simply adding people to their operations teams, which compared to only 18% 12 months ago. And anecdotally, this number increases to > 50% in some of the larger brokers and custodians, many of whom have been reported to have added significant headcount. (Citi Securities Services Evolution 2024)

This would potentially imply two things:

The industry underestimated the challenge and impact to their operating models and had to invest more in people as the deadline neared.

Organisations left it too late to get mobilised, leaving insufficient time for automation and ultimately compensating with people to plug the gaps.

This latter point would also imply there is an element of catch up within investment cycles going into 2025 and beyond – which is going to create capacity challenges as organisations balance investment in remediation vs planning for 2027 and beyond. Organisations in the UK and EU would do well to apply the lessons their US counterparts learned, particularly into investment thinking. But, as we’ve seen in the past, the industry frequently talks a good game and then reverts to tactical compliance to hit the dates.

One panellist at AFME shared an excellent analogy from a recent post trade conference, stating that “the industry is currently very focused on the shiny T+1 penthouse but is ignoring the fact that the foundations are cracking”. This underlines the challenges that many organisations face: they are unable to mobilise effectively to unpick what are extremely complex legacy architecture and process challenges so paper over the cracks instead.

Focused on the ‘penthouse’

These are not simple challenges to solve (otherwise they would have been solved already) but warrant serious attention as the industry considers its next steps. Adding headcount to deal with a relatively simple set of market infrastructure practices (in the US) vs trying to replicate that approach across a region with almost 40 financial market infrastructures (FMIs) is clearly not realistic.

The positive adoption of AI and other trade process automation tools has shown in part what can be achieved through leveraging the types of innovation that were not present 10 years ago. But technology in itself is not going to deliver automation, it is merely an enabler and the industry will need to mobilise quickly if it is to learn from the global experience of T+1 to figure out operating model optimisation.

5. Governance is not sexy, but it’s necessary

What the North American regulators did well was communicate clearly and often, creating momentum and also certainty (the slipped milestones that characterised Dodd Frank and other regimes in the past weren’t going to happen here). This energy pushed the whole industry towards the end goal, with working groups mobilised and being visibly active around decision making on key points of contention.

Replicating this across multiple jurisdictions is going to be much, much harder and regulators, FMI’s and the industry working groups that guide them need to be highly focused on mandating the right structures and behaviours to lead the industry forward.

The US experience has shown a blueprint, but it doesn’t have to be adopted – there is a much greater degree of complexity across the UK and Europe, which can’t be ignored in attempting to globalise T+1. The industry shouldn’t be blind to this and has to balance pragmatism with market impact – for no other reason than the sheer scale and complexity of cross-border flows across the region.

Looking ahead to 2027

The experience of the T+1 shift globally has shown some positive signs, but that doesn’t mean one-size fits all in terms of implementation. The costs of compliance will be significant and the economic benefit of the change has not been equally distributed across all market participants. Individual firms should not be reliant on moving with the herd, as the nuances of systems and process, business mix, investor and client mix and geographical reach, will all ensure that no one firm’s challenges (and opportunities) are the same.

The US experience has signposted what the future could look like in terms of market efficiency and standardisation, but this should not be viewed as a ‘cut and paste’ around what will work elsewhere. Bringing similar value will require collaboration and consensus across a fragmented post trade landscape across the European region, which is not in itself a trivial exercise.

The disconnect between betting markets, and actual asset moves, versus the polling messaging magnified the level of shock at the strength of the victory, according to Jeff O’Connor Head of Equity Market Structure, Americas, Liquidnet.

“Really, the equities market has been responding with near certitude to the “Trump Trade” for several months,” he told Traders Magazine.

“There was some waffling late, and may have been driven by profit taking, but what the election did was qualify the accuracy of what the markets were telling us which hearkens back to the old adage, “the price is the news”,” he said.

“But certainly, going forward, the methods used to ascertain U.S. polling will be very much in question,” he said.

Jeff O’Connor

And early on, the Trump Trade winners have erupted, O’Connor said.

“While the conviction, outsized volume supporting a high standard deviation move, will have to temper, it is those types of trading days that can signal what the path of least resistance is going to be in the equities market,” he said.

According to O’Connor, it was remarkable to see many of the major indexes hitting all time highs supported by volumes some 60% beyond the averages of the year.

But it is that type of conviction that triggers the quant/systematic crowd to get involved, he said, adding that it can be described as a technical feedback loop, but almost the guaranteed business of momentum funds grabbing onto the move and then pushing to fresh highs.

“Couple that with some of the best traditional asset manager flows of the past four years, as reported by sell side trading desks, and the post-election day market action was extremely powerful,” he commented.

The contrast between the two candidates ideologies has made this election more clear from a market perspective, O’Connor said.

Whether it be corporate tax plans, tariff expectations, or sector specific winners/losers, the candidate dichotomy on visions for the economy, consumers, and suppliers, made the Trump Trade fairly easy to track, he added.

On the first day of trading, the clear cut winners were small caps, banks, construction materials, energy equipment, machinery, etc, he said, while the underperformers included solar, copper, Chinese technology, hospitals, defensives, etc.

But aside from sector/sub-sector performance, the more macro level trades maybe stand out the most – i.e. the dollar and rates, O’Connor said.

“What the moves are telling us is that the expectation is that Trump’s second term will follow the first, and that is tax cuts, deregulation, tariffs that will simultaneously spark economic growth, corporate profits, but with it inflation,” he said.

“And the possibility, seeming more likely, of total executive and legislative GOP control, is exacerbating the strength of moves,” he added.

According to O’Connor, clearly the potential for total GOP control has the institutions getting into trades quicker than they may have anticipated as they position for the future.

“Continuous institutional volumes in ’24 have been some of the best of the past 7-8 years, however, with equity performance so strong, and the presidential overhang, there was signals of institutional trepidation going into the election,” he said.

Valuations are obviously extended, and this year already marks a major outlier in terms of market performance versus historical averages on election years (+24% vs ~+7%), according to O’Connor.

One area that has gotten a significant boost is the small cap space where the prospects of better business backdrop (along with deregulation) are letting stocks move in the face of a total rate reprice, he said.

This arena is the most sensitive to higher interest rates, and should rates go higher from here, in general, not just for small caps, equity performance will see a cap, he said.

“In the end, the noise of the election will die down and volumes will revert quickly,” O’Connor said.

“There are signals that, globally, fund managers are over-exposed to U.S. markets and available cash has moved towards historical nadir levels. Performance is being driven by the macro backdrop,” he said.

“The market obviously likes the prospects from a fiscal perspective, and the FOMC’s job gets tougher as campaign promises point to a possible res-snap on inflation, but equity performance is going to continue to be driven by macro data points – the ability to meet steeper earnings growth expectations into 2025 and the ability to navigate the economy into a soft/no landing,” he added.

Trading limits have come into the focus of senior management teams across the sell-side, according to the Q4 2024 Sell-Side Execution Management Insight report by Acuiti.

A major fine from UK regulators has changed approaches across the sell-side, the report noted.

“This new focus on trading limits has shone a light on issues such as the lack of a central limits system and lack of clarity on how execution limits should be calculated,” the report added.

Banks operate their own models for trading limits and determining them for a client is often a nuanced exercise that involves the desk’s accumulated knowledge about their clients’ needs and strategies, according to the report.

For futures desks, trading limit calibration was identified as a high or urgent priority by 61% of the network.

Network members report that improving pre-trade risk analysis is an important part of these reviews.

Acuiti said that give-up arrangements are also emerging as an item of particular attention within the trading limits discussion.

According to the findings, most of the network reported calculating client futures trading limits on a product-by-product basis.

“This approach requires extensive analysis of each product, considering factors such as the order book for that product, the algos used to trade it its IM and other aspects of market structure,” the report said.

The report stressed that “explaining the nuance and minutiae of trading limit calculations to senior management and regulators can be a time-consuming exercise”.

According to Acuiti, if senior management teams have the technical knowledge or experience of working an execution desk, the process is much easier, however, over a third of the network cited it as a major inconvenience.

The report also covered the rising demand for commodity futures, India’s Gift City, the re-bundling of execution and research and the outlook for the remainder of 2024.

The report is based on a survey of the Acuiti Sell-Side Execution Network, a group of over 300 senior executives at banks and brokers across the global market.

Each quarter members of the network input topics and questions into the survey with the responses aggregated into this report.

Interactive Brokers (Nasdaq: IBKR), an automated global electronic broker, announced the success of its ForecastEx prediction market. Since its launch on October 4, 2024, ForecastEx has a total volume of over USD 560 million in presidential election contracts traded as of midday on November 6, 2024, with no technical issues reported.

Key Highlights:

ForecastEx Performance: ForecastEx Election Contracts proved to be a good predictor of election outcomes offering publicly visible prices which clarify real-time sentiment and bring accountability and transparency to a topic.

Future of Prediction Markets: Interactive Brokers sees prediction markets like ForecastEx becoming valuable tools in the coming years, offering unique data and insights. Beyond elections, IBKR’s ForecastTrader provides contracts on economic indicators, environmental factors, and government-related issues.

Steve Sanders, EVP of Marketing and Product Development at Interactive Brokers, noted, “Since investors must commit capital to express their conviction, they are engaged and educated about a subject. ForecastEx delivered highly predictive, real-time data to both investors and the broader market.”

On election night, Interactive Brokers also achieved record overnight trading volumes, including:

US Stocks: 188,168 trades

US Derivatives: 161,742 trades

Total Overnight Trades: 349,910

This occurred from 8:00 pm to 4:00 am Eastern on US markets and represents a huge increase over normal overnight trading.

By Bob Cioffi, Global Head of Equities Product Management, ION

The equities trading landscape has taken a dynamic turn over the past few years. While the continued dominance of low-touch, algorithmic trading has accelerated the speed of activity, the rise of alternative trading venues worldwide has unlocked a wider range of options and opportunities.

Firms are feeling the pressure as a result. While buy-side businesses jostle for access to as many markets as possible to avoid missing out on liquidity, sell-side firms are competing to help deliver on those ambitions. However, both are struggling to keep up with the pace of change.

The market needs more agility and connectivity to manage greater volumes and demands. But the question of who takes ownership for this innovation – and bears the cost – is more complex. With more market players than ever before, firms, venues, and technology providers need to work out how to share this burden to reap the collective benefit.

New competitive dynamics

Across the equities market, choice and competition among trading venues is ramping up.

New, alternative trading venues have been challenging traditional exchanges for some time. Both are experimenting with new functionalities and order books – auction, dark, lit, and conditional – to differentiate themselves as the go-to platform for clients. In Europe, the London Stock Exchange (LSE) acquired Turquoise to draw liquidity back in response to post-MiFID liquidity fragmentation, while Euronext has grown by acquiring exchanges in Dublin, Oslo, and Milan.

Less typical market players have also entered the fray to challenge the primary exchanges. These range from banks creating their own trading venues, such as UBS’ MTF and Goldman Sachs’ MTF (SIGMA X), to brand new exchanges such as Artex, which offers tokenized art funds as a new investment opportunity and allows museums to trade digital asset securities like equities. The rapid growth of IntelligentCross, an alternative trading system (ATS) is another good example.

In a fragmented landscape where multiple venues offer free market data and connectivity with prominent liquidity providers, horizontal differentiation – exchanges offering different types of products or services to cater to different market segments – is increasingly common. We are at a point where no single venue can serve the interests of all investors.

Pressure on the system

It’s common for firms to want to “try before they buy” with access to new venues in the market. But building the technology to create fast access in this way is costly – both in time and resources.

For sell-side businesses to deliver best execution for their clients, the cost of connecting to every available venue currently outweighs the benefits. This leads most to opt for selective connections and rely on broker services. For buy-side firms and end-users deciding which markets they would like to access and how, these different approaches to connectivity will continue to shape their decisions, especially as different types of trading venues evolve. Naturally, technology providers are under pressure from all angles to build and monetize a new era of market infrastructure: solutions that can support connectivity to new venues, and therefore help all parties achieve their goals.

As a rule, greater competition is an economic good. It moves the market forward, breeds innovation, and results in lower costs. But key industry questions – such as who should take the lead in modernising market infrastructure to meet abundant modern connectivity needs – make reaching a verdict more difficult.

Addressing the challenge

As venues and order types grow in number, the degree of overhead in today’s market is significant – and the pace of change is fast. The question is how the market can innovate to keep up at a time of such rapid development.

Traditional processes for securing connectivity such as the manual configuration of connections and the lengthy onboarding of new clients are no longer quick or adequately responsive to meet needs. Technology firms need a way to work with new venues and exchanges to meet the needs of market participants.

At the same time, the growing trend of consolidation across exchanges in terms of ownership – for instance, the widespread adoption of Nasdaq’s technology – is also helping exchanges to take a big leap in terms of capabilities and offerings. Alongside the opportunity for new technology markets to provide much-needed common interfaces between different venues, a broader shift towards efficiency and scalability is already unfolding through consolidation.

Looking to the future

As we move ahead, it is through a collaborative effort that the market can address the challenge of funding new demands for innovation. With liquidity and best execution at stake, market connectivity is more important than ever. This bid for more options and flexibility is a prime opportunity to create a more resilient, agile market structure that can support the demands and direction of modern trading.

Who Pays for Innovation? Why Market Collaboration is the Key to More Connectivity

By Bob Cioffi, Global Head of Equities Product Management, ION

The equities trading landscape has taken a dynamic turn over the past few years. While the continued dominance of low-touch, algorithmic trading has accelerated the speed of activity, the rise of alternative trading venues worldwide has unlocked a wider range of options and opportunities.

Firms are feeling the pressure as a result. While buy-side businesses jostle for access to as many markets as possible to avoid missing out on liquidity, sell-side firms are competing to help deliver on those ambitions. However, both are struggling to keep up with the pace of change.

The market needs more agility and connectivity to manage greater volumes and demands. But the question of who takes ownership for this innovation – and bears the cost – is more complex. With more market players than ever before, firms, venues, and technology providers need to work out how to share this burden to reap the collective benefit.

New competitive dynamics

Across the equities market, choice and competition among trading venues is ramping up.

New, alternative trading venues have been challenging traditional exchanges for some time. Both are experimenting with new functionalities and order books – auction, dark, lit, and conditional – to differentiate themselves as the go-to platform for clients. In Europe, the London Stock Exchange (LSE) acquired Turquoise to draw liquidity back in response to post-MiFID liquidity fragmentation, while Euronext has grown by acquiring exchanges in Dublin, Oslo, and Milan.

Less typical market players have also entered the fray to challenge the primary exchanges. These range from banks creating their own trading venues, such as UBS’ MTF and Goldman Sachs’ MTF (SIGMA X), to brand new exchanges such as Artex, which offers tokenized art funds as a new investment opportunity and allows museums to trade digital asset securities like equities. The rapid growth of IntelligentCross, an alternative trading system (ATS) is another good example.

In a fragmented landscape where multiple venues offer free market data and connectivity with prominent liquidity providers, horizontal differentiation – exchanges offering different types of products or services to cater to different market segments – is increasingly common. We are at a point where no single venue can serve the interests of all investors.

Pressure on the system

It’s common for firms to want to “try before they buy” with access to new venues in the market. But building the technology to create fast access in this way is costly – both in time and resources.

For sell-side businesses to deliver best execution for their clients, the cost of connecting to every available venue currently outweighs the benefits. This leads most to opt for selective connections and rely on broker services. For buy-side firms and end-users deciding which markets they would like to access and how, these different approaches to connectivity will continue to shape their decisions, especially as different types of trading venues evolve. Naturally, technology providers are under pressure from all angles to build and monetize a new era of market infrastructure: solutions that can support connectivity to new venues, and therefore help all parties achieve their goals.

As a rule, greater competition is an economic good. It moves the market forward, breeds innovation, and results in lower costs. But key industry questions – such as who should take the lead in modernising market infrastructure to meet abundant modern connectivity needs – make reaching a verdict more difficult.

Addressing the challenge

As venues and order types grow in number, the degree of overhead in today’s market is significant – and the pace of change is fast. The question is how the market can innovate to keep up at a time of such rapid development.

Traditional processes for securing connectivity such as the manual configuration of connections and the lengthy onboarding of new clients are no longer quick or adequately responsive to meet needs. Technology firms need a way to work with new venues and exchanges to meet the needs of market participants.

At the same time, the growing trend of consolidation across exchanges in terms of ownership – for instance, the widespread adoption of Nasdaq’s technology – is also helping exchanges to take a big leap in terms of capabilities and offerings. Alongside the opportunity for new technology markets to provide much-needed common interfaces between different venues, a broader shift towards efficiency and scalability is already unfolding through consolidation.

Looking to the future

As we move ahead, it is through a collaborative effort that the market can address the challenge of funding new demands for innovation. With liquidity and best execution at stake, market connectivity is more important than ever. This bid for more options and flexibility is a prime opportunity to create a more resilient, agile market structure that can support the demands and direction of modern trading.