The AI Insights: Revolutionizing Financial Trading panel, opened with the simple, straightforward question of what has changed in the past year.

It was noted that conversations in October 2023 were more about pilot programs and proofs of concepts, whereas now with more development now there is more AI actually in use.

Still, some unrealistic expectations of a “magical trading robot” or the like remain out there, and remain far from being realized.

AI goes hand-in-hand with data, and the panel noted that AI is making strides in giving traders more useful knowledge while reducing the noise that comes from data overload. For example, an AI-powered cluster model can screen stocks for characteristics such as capitalization, liquidity, and spread, telling the trader whether a given stock is relatively easy or difficult to trade.

Even if that works well, one panelist said “there is always information on the trading desk that is not captured in data, and you need a trader to still make human decisions.” And in fact, areas of progress over the past year have been in better human decision-making and challenging of the data.

Risk management is fertile ground for applying AI, including the newer generative AI, the panel noted. AI won’t itself solve a risk problem, but “it will give a human expert a head start on where it’s best to apply efforts” to solve the problem.

The panel stressed the importance of guardrails and education in rolling out AI. The technology “isn’t really making decisions in these early days. But it is freeing up humans to do more interesting and important work.”

One rough benchmark to strive for is AI freeing up 90% of human trader and technologist time, so they can focus on the most important 10% of their work.

The future of AI is potentially boundless, as it was noted that today’s AI models “are the worst you’ll ever see” when compared with what’s to come.

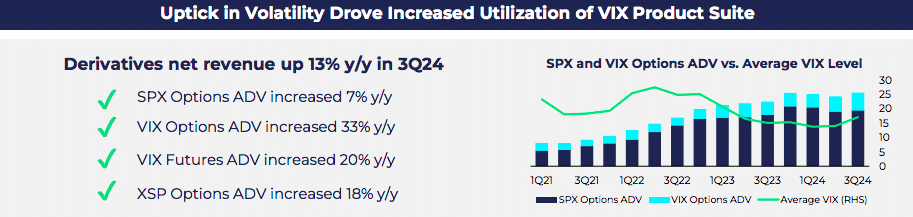

Cboe Global Markets had record derivatives volumes in the third quarter, which the derivatives and securities market operator said was driven by proprietary index options and futures products.

Source: Cboe

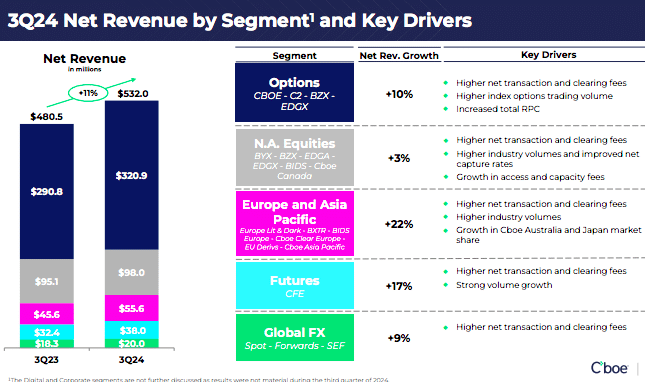

The group reported record net revenue for the quarter of $532m, up 11% year-over-year. Derivatives net revenue grew 13% year-over-year in the third quarter due to record volumes.

Fredric Tomczyk, chief executive of Cboe Global Markets, said on the third quarter results call on 1 November that the record results were driven by strong volumes in its derivatives franchise, specifically the proprietary index options and futures products. In addition, there were “solid” volumes across cash and spot markets, continued expansion of the data and access solutions business and steady expense management.

Fredric Tomczyk, Cboe

Tomczyk said: “Over the past year as CEO, I have concentrated on sharpening our strategic focus and making important and deliberate decisions on how to best allocate our capital and resources to support our growth strategy.”

As a result of the strategic review, the group has dialled back its M&A activities, lowered expense growth and stabilized margins. The capital allocation strategy has changed to increase investments in organic initiatives and reallocated resources to align with core strengths, which Tomczyk described as derivatives; data and access solutions and leading-edge technology.

Although Cboe will focus on an organic growth strategy, the group will continue to explore acquisitions that provide scale and broaden distribution inside key geographic markets. “I have always said we were going to slow down M&A, but I have never said we were never going to do M&A,” said Tomczyk

He highlighted that Cboe has just acquired a 14.8% ownership stake in proprietary trading system, Japannext.

“Japan is one of the largest and most important capital market places in the world, and is undergoing a lot of change as the regulatory landscape evolves and the market opens to more competition,” said Tomczyk. “We see tremendous opportunity for Cboe to compete.”

Options business

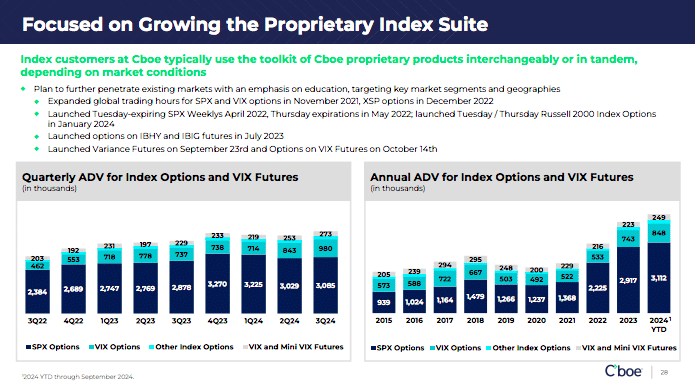

The strategic framework includes investing in the continued growth of the core global derivatives business as there is increasing demand for access to the US market, and for options.

“Given that options by their very nature expire, investors must repurchase new options to reposition themselves in the market, which in turn creates a quasi-recurring revenue stream that continues to increase,” Tomczyk added.

Options achieved record net revenue of $320.9m, up 10% from the third quarter of 2023. Dave Howson, global president of Cboe, said on the results call that the increase was led by strength in proprietary products.

Source: Cboe

Howson said the most notable event in the third quarter was the yen carry trade unwind on 5 August that produced one of the largest short-term volatility events since the Covid pandemic and the global financial crisis.

“Investors rushed for downside protection in the form of VIX options and ADV of 1.2 million contracts in August was the second highest on record, trailing only February 2018,” added Howson.

He also highlighted the launch of variance futures on 23 September, which Howson described as the latest tool in Cboe’s volatility toolkit to provide an exchange-listed alternative to over-the-counter variant swaps.Variance futures offer a streamlined approach to trading the spread between implied and realized volatility of the U.S. equity market as measured by the S&P 500 index, enabling market participants to take advantage of discrepancies between market expectations and actual outcomes.

In addition, Howson noted the launch of options on VIX futures on 14 October. Cboe offered securities-based VIX index options but the new contracts are physically settled. With futures as the underlying asset, the new options are CFTC-regulated, enabling access for market participants that are restricted from accessing U.S. securities-based options to use the product to express their views on equity market volatility.

David Howson, Cboe Global Markets

Options on VIX futures also allows Cboe to offer more tenors, in particular, those with a shorter duration that meet customer demand. Howson said: “These two additive products need time to seed, but the early signs are really good, though. We have got prices on the screen, customers engaging and testing the plumbing, and a good pipeline coming through.”

He continued there is also a meaningful opportunity to bring options to a greater portion of the US customer base, especially using exchange-traded products to access a variety of options strategies in a traditional ETF wrapper.

“US listed options-based ETFs have grown to an estimated $120bn in AUM, with assets increasing over 600% over the past three years,” added Howson.

Retail market

Cboe also remains optimistic on the growing retail participation in the options market. In October this year Cboe and Robinhood Markets announced they will launch Cboe’s index options on the retail broker’s platform, which is slated for this quarter.

“We believe retail adoption of index options is just beginning, and Cboe is well positioned to cater to this growing demand,” added Tomczyk.

The strategy for supporting continued retail growth includes education, broadening access by working with retail brokers and listing products that provide opportunities for customers to trade a contract that is the right size for them and on a time frame that suits their needs, particularly shorter-dated contracts. Cboe estimated that less than 10% of customers at large retail broker-dealers are currently enabled to trade options.

International growth

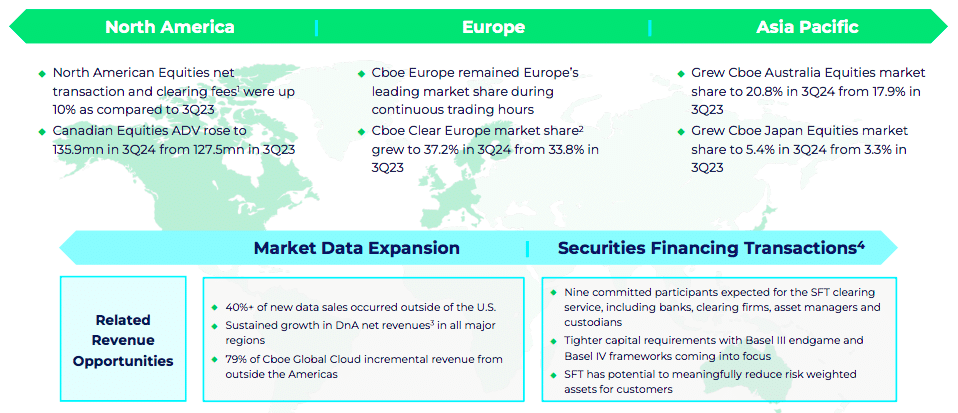

During the third quarter, approximately 40% of new sales in the data and access business were international.

“We remain particularly excited about the outlook for our Canadian business as we remain on track with the migration of our Canadian market to Cboe technology in early 2025, subject to regulatory approval,” said Howson.

Source: Cboe

In Australia Cboe grew market share to 20.8%, up 2.9% from the third quarter of 2023. In Japan market share hit 5.4% in the third quarter, a 2.1% improvement from the same period in 2023.

“The Asia Pacific region remains a key focus for Cboe as we move forward, providing a number of opportunities across our ecosystem to fuel growth,” said Howson.”We anticipate continued strategic investment in the region in increased brand awareness and improved sales efforts for the import of derivatives activity into the US.”

Technology

In February this year Cboe introduced dedicated cores for its EDGA equities exchange. Dedicated cores allows members and sponsored participants to host their specific logical order entry ports on their own CPU core(s), rather than sharing a core(s), which reduces latency, enhances throughput, and improves performance.

“The uptake from dedicated cores continues to exceed our expectations as we roll the functionality out across additional markets,” Howson.

Dedicated cores is due to launch in the UK and Europe in this quarter and the first quarter of next year, then Australia, and eventually Japan and Canada.

Chris Isaacson, Cboe

Chris Isaacson, chief operating officer, said on the call that the Canadian migration in March will be the last onto Cboe’s technology platform.

“We have spent a fair amount of time and a lot of resources this year making that happen,” he said. “We think that will free up a substantial amount of resources to focus on high growth areas like derivatives and data and access.”

Isaacson added that Cboe is investing heavily in its data analytics platform and on artificial intelligence to drive productivity within the organization, but also to explore and enhance revenue opportunities for customers.

Source: Cboe

Jill Griebenow, chief financial officer, said on the results call that Cboe is raising the organic total net revenue growth range for 2024 to between 7% and 9%, up from the prior guidance of 6% to 8%, given the year-to-date trends and expectations for the fourth quarter.

ETF Exchange traded fund Trading Investment Business finance concept on virtual screen

This issue of The Cerulli Edge—U.S. Monthly Product Trends analyzes mutual fund and exchange-traded fund (ETF) product trends as of September 2024 and assesses the responsible investing product landscape.

Highlights from this research:

-At the end of September, mutual fund assets stood at $20.6 trillion, up 1.4% from August. Mutual funds continued to leak flows throughout the year, with $40.8 billion in September.

-ETF assets crossed the $10.0 trillion mark in net assets in September. ETF flows missed out on surpassing the $100 billion mark in September, generating $95.9 billion in flows.

-Concerns over greenwashing, political backlash, and underperformance have hurt overall responsible investing assets. As the landscape matures, product development has slowed, alongside a record number of recent mutual fund and exchange-traded fund (ETF) product closures. Despite these challenges, a broader range of products, structures, and asset classes are becoming available to investors. While anticipated demand from retail investors through advisor-sold channels has not materialized in a significant way, capital allocations from U.S. institutional investors remain solid.

Graham Howell has joined Corlytics as Chief Finance Officer with 35 years of experience with PE-backed firms, helping lead the firm as it continues its rapid expansion into the United States through organic and inorganic growth. Reporting directly to founder and CEO John Byrne, Howell brings 35 years’ experience in finance functions within the software industry, of which the last 15 years have been spent as the CFO of various SaaS software companies, including Nextlane, TraceOne and Ullink.

George Stephan

Franklin Templeton has appointed George Stephan to the newly created position of Global Chief Operating Officer of Wealth Management Alternatives. Stephan previously spent five years at Kohlberg Kravis Roberts & Co. (KKR), as the Head of Strategy and Business Development for the firm’s Global Client Solutions business. Before that, he was Chief Operating Officer and Head of Investor Relations for KKR’s Global Wealth Solutions business in the Americas.

Ryan Terpstra

ITRS, a provider of real-time IT monitoring and observability solutions, has appointed Ryan Terpstra as CEO. Terpstra succeeds Guy Warren, who has decided to step down from executive roles to spend more time with his family, after successfully leading the company for over a decade. Terpstra brings more than two decades of C-level experience leading and growing technology companies, spanning venture-backed startups, middle-market private equity-backed firms, and global public corporations. Most recently, he was Chief Product Officer at ION Analytics.

Broadridge Financial Solutions has announced the appointment of David Fellah as Vice President of AI Trading Solutions at Broadridge, based in New York City, NY. He will report into Roger Burkhardt, Enterprise Head of AI and Data and CTO of Capital Markets at Broadridge. With nearly 30 years of expertise at the cutting edge of trading technology, quantitative research, and advanced analytics, Fellah brings significant leadership experience from roles at Instinet (Nomura), ITG, and J.P. Morgan.

CoinShares has appointed Lisa Avellini as Group General Counsel, effective November 4, 2024. Avellini brings a wealth of valuable experience to CoinShares, with an extensive background in legal and compliance roles within leading global financial institutions. She joins CoinShares after three years at Balyasny Asset Management, where she oversaw global legal and compliance requirements. She is also an alumnae of Citadel.

Robert Eaton has joined Northern Trust Asset Management as a Senior Relationship Manager within NTAM’s Wealth Client Group. Eaton brings more than 20 years’ experience in asset management, exchange traded funds and wealth-tech. His prior experience includes serving as Head of Strategic Relationships at BondBloxx Investment Management ETFs; a variety of business development roles at BlackRock including Head of Americas Business Development for Aladdin Wealth Tech and Head of National Accounts for BlackRock and iShares; and as Head of US Retail Marketing at Merrill Lynch Investment Managers.

The FCA and PSR boards have announced the appointment Alison Potter as chair of the FCA’s Regulatory Decisions Committee (RDC) and the PSR’s Enforcement Decisions Committee (EDC). Potter has previously been appointed as a senior decision maker for the Guernsey Financial Services Commission in 2018. She has over 30 years of experience as a barrister working in commercial law, specialising in financial services and financial regulatory law.

If you have a new job or promotion to report, let me know at alyudvig@marketsmedia.com

The traditional asset management industry is standing on a precipice, facing immense pressure from all sides. Small and medium-sized investment houses, juggling both equity and fixed-income portfolios, are especially feeling the heat. As retail investors continue to flock to passive investment giants, and institutional investors demand greater customisation at ever-lower fees, many traditional players find themselves struggling to keep up. It’s a battle for survival, and the truth is, this crisis has been looming for years. The cost squeeze that asset managers are now experiencing has reached breaking point.

At the heart of the problem lies a plethora of inefficient processes that have, until now, been tolerated. Research by Coalition Greenwich reveals that outdated systems for managing and sharing data — including manual processing — are costing asset managers millions of dollars each year. One example is the daily grind of trade reconciliation. Each trading day, custodians send data packages to asset managers, outlining the value of assets held on behalf of their clients. These figures need to be reconciled with the fund manager’s own internal records, which include any intra-day trades taking place through brokers. If discrepancies arise, such as trades that haven’t been processed or mismatched valuations, a small army of people is needed to track down the issues and resolve them. It’s a tedious, time-consuming, and frankly immensely costly affair that the industry can no longer afford to absorb.

This archaic approach is just one example of where traditional asset managers can haemorrhage resources. As with many of the operational challenges faced by asset managers, the solution lies in creating a reliable, accurate, and timely source of truth for data that can effectively underpin a fully automated process. Rather than wasting valuable time sifting through data to find exceptions and errors, asset managers can fully automate workflows. This provides real-time trade monitoring, comprehensive audit trails, and configurable alerts which maintain trade integrity. The copious time saved from this automation can then be redirected towards higher-value activities. From conducting deeper market analysis and making more informed decisions to optimise portfolio performance, to spending quality time with clients to understand their needs — think of all that could be done with the additional headspace.

Asset managers have no choice but to adapt. While automating processes is an essential step, it’s about more than just replacing manual tasks with technology. The future lies in fostering a culture of continuous improvement, built on an operating system that connects the past with the future. Such a system should allow firms to be data-driven, using automation, machine learning, and AI to enhance decision-making. Building this foundational infrastructure and mindset is not just a cost-saving measure — it’s the key to remaining competitive in today’s passive-dominant market. Without it, asset managers risk becoming relics of the past, unable to keep pace with an industry that demands adaptability and forward-thinking solutions.

Integration of AI is Reshaping the Business of Market Data Providers – New Burton Taylor Report

Clients are influencing the deployment of AI-driven solutions, demanding more automation, precision, and actionable insights from data providers.

AI will provide a path to greater production and variety of data, with Burton Taylor expecting AI to contribute 3.3% to the market data industry TAM by 2029, growing at a 56% CAGR to 2029.

Burton Taylor estimates that AI will add an incremental $1.9 billion to market data providers’ revenues.

November 1st, 2024 – Artificial intelligence is affecting data products for both human and machine consumption, changing the dynamics of data use and demand, and internal operational processes. A new report from Burton Taylor International Consulting, part of TP ICAP’s Parameta Solutions, evaluates AI’s present and future influence on data consumption, the emergence of new data types, and exponential data growth.

“AI is being leveraged across the market data and capital markets value chain. Today POCs are exploring the next generation of AI for use in human and machine consumption of data. “AI is substantially impacting the market data business. It allows new levels of operational effectiveness in the processing of data and sets the stage for new types of data products that market participants will demand,” says Brad Bailey, Research Director at Burton Taylor. “AI in the capital markets will look very different by 2029.”

The future progression, however, will not be without its challenges to data providers, according to the report. “While AI offers significant benefits,”notes Bailey, “Market data providers face hurdles in areas such as data readiness, regulatory compliance, explainability, and intellectual property. These challenges require continuous investment in data governance, model transparency, and legal frameworks to ensure that AI is deployed responsibly and effectively.”

This new Burton Taylor report explores how the integration of AI is fundamentally reshaping the landscape for market data providers, driving innovations in data processing, analytics, and product delivery. Further, it looks at the way AI sets new standards for how financial data is consumed and utilized by enhancing data quality, automating workflows, and enabling real-time insights.

The Bank of New York Mellon Corporation, a global financial services company, announced the expansion of its iFlow1 product offering, with more extensive fixed income and equity data analytics. iFlow provides a unique vantage point of insights into BNY’s more than $50 trillion in assets2 under custody and/or administration, revealing global asset allocation trends and market-moving reactions, to investment managers and asset owners.

With this expanded capability, BNY’s iFlow will now be able to generate on-demand charts for shorts, holdings, and positioning, complementing existing flow views. This allows for clearer definitions of rotation trade equity, credit, and duration in bonds and, ultimately supports improved benchmark definitions and portfolio construction.

iFlow will now provide the following fixed income and equity insights:

· iFlow Shorts: aggregates short interest metrics that capture borrowing and lending behavior, aiding portfolio managers in making portfolio construction decisions.

· iFlow Holdings: reflects investor exposure to stock and bond markets, showing an aggregated view into how investors have allocated capital across country, sector, credit rating and maturity.

· iFlow Positioning: measures investment preferences based on aggregated investor holdings, showing capital deployment across countries and sectors, compared to other asset classes and benchmarks.

The new indicators are designed to provide transparency into unexpected market moves and show how markets have acted historically, helping to determine the potential vulnerabilities around shock events.

“Finding ways to distill and understand market data continues to be one of the most important priorities for our clients. The challenge of today is no longer about getting access to vast market data sets but finding ways to unpack and generate insights,” said Jason Vitale, Head of Global Markets Trading at BNY. “Given our unique vantage point, touching about a fifth of the world’s investable assets, and through our expanded iFlow capabilities, we’re able to help clients better understand global markets.”

With economists having to react to news cycles getting even shorter and market events happening quicker than before, they can no longer count solely on the traditional widely disseminated macro-metrics and tools to provide actionable analysis, according to Michael McDonough, Chief Economist for Financial Products at Bloomberg.

Michael McDonough

On October 30, Bloomberg in partnership with Coalition Greenwich released a new study that assesses how U.S. economists and strategists are utilizing data, analytical tools and emerging technology in anticipation of the most impactful macro events, including the U.S. Presidential Election.

The study reveals that economists from leading asset managers, top banks and broker research firms, NGOs and government agencies are adopting new predictive tools, alternative data and generative AI.

McDonough said that for example, in the first presidential debate, people were caught off guard by what happened.

“Relying on traditional polling data means waiting days or even weeks to assess the impact,” he told Traders Magazine.

“Predictive markets, however, offer an immediate sense of how significant an event might be, allowing for a faster understanding of its implications,” he said.

“Broadly speaking, traditional data is very backward looking, and people are trying to get a read on where we are now, not where we were a month ago,” he added.

McDonough said that another key finding, which supports this, was that economists rank alternative data—particularly social media sentiment analysis and real-time consumer transaction data—and Generative AI-enhanced analytics as the #2 and #3 most important tools to analyze macro drivers over the next 12 months.

“We’ve offered prediction market data on the Terminal since 2020, so while we were aware of the demand, we underestimated just how significant that interest would become,” he commented.

According to the findings, early career economists highly value generative AI for use in forecasting models as the single area of their workflow that may be transformed in the coming 2-3 years.

Kevin McPartland

Kevin McPartland, Head of Market Structure and Technology Research at Coalition Greenwich, commented that experienced economists and strategists are also looking to complement traditional tools with innovative solutions, as shown through their adoption of alternative datasets in their daily workflows.

“In our research, 53% of economists with 15-years or more of experience reported utilizing social media sentiment data daily, 47% utilized real-time consumer transaction-level data, 47% utilized web traffic and app usage data, 35% event driven feeds, 29% geolocation data (including foot traffic data) and 24% satellite/imagery data,” he shared.

“Considering this, when analyzing the U.S. economy, 56% of economists with 15-years or more of experience still view point-in-time data as more important than alternative data,” he said.

McPartland told Traders Magazine that forecasting is only one of AI’s early applications, and economists are already adopting AI in complementary ways beyond prediction as they try to determine its value.

For example, he said, the study found that AI is widely used in summarization tools, with 33% of economists and strategists identifying it as the most transformative AI application in their workflow, and 18% viewing sentiment analysis as most transformative.

“Specifically when trying to figure out risk analytics and the sensitivity of a position to the election for a portfolio, macro investors can utilize these AI tools and alternative metrics to help gauge the potential risks, he said.

The findings also suggest that fast, robust, and easily accessible data is key.

“Economists today are faced with an overwhelming array of data, and the ability to quickly access and synthesize this information is essential,” McDonough said.

He stressed that with the sheer volume of data out there today, economists and strategists need to seamlessly integrate it into their workflow and connect all of it to find the signal in all this noise.

“That’s where AI plays a critical role to seamlessly connect the data, model it, present it in a way where they can then extract insights and signals,” he said.

“This is going to become very crucial for economists and strategists in the future, especially as they continue to have to analyze larger raw and calculated data sets than ever before,” he concluded.

United States Capitol Rotunda. Senate and Representatives government home in Washington D.C.

FLASH FRIDAY is a weekly content series looking at the past, present and future of capital markets trading and technology. FLASH FRIDAY is sponsored by Instinet, a Nomura company.

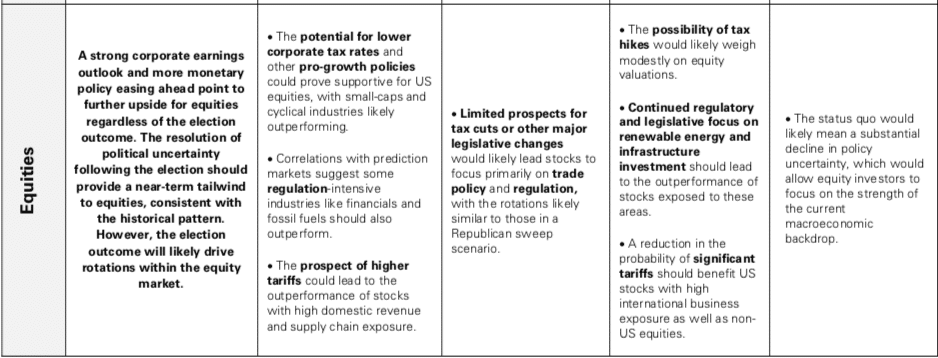

The US election on 5 November 5 is definitely top of mind. So it is unsurprising that Goldman Sachs’ latest Top of Mind report focuses on post-election economic policies. Alec Phillips, chief US political economist in Goldman Sachs Research, said in the report that financial regulation could change in a second Trump administration, with potentially faster shifts across consumer finance than in the case of capital and liquidity requirements.

Under a second Trump administration, Goldman Sachs also expects an easier regulatory climate for several sectors including energy, antitrust enforcement and healthcare.

“That said, while reduced regulation could in principle boost economic activity, our prior bottom-up work in this area suggests that deregulation during the first Trump Administration had a limited macroeconomic impact,” added Phillips.

The bank also looked at the possible impact on asset classes including equites:

At Northern Trust, Grant Johnsey, regional head of client solutions for capital markets found there are seven instances in which the S&P 500 returned over 20% in a calendar year before a presidential election year. In those seven instances, the S&P 500 closed higher in the subsequent election year. Therefore, unless there is a dramatic sell-off in the last two months of this year, 2024 should be the eighth instance where the S&P 500 closes higher in an election year following a 20%+ gain in the previous year.

Jim Toes, president and chief executive of STA, said in a newsletter that things to keep in mind as the election approaches include buy hope, sell fear; the need to educate yourself and vote and to be gracious.

He stressed that the STA is bipartisan: “No matter what the political landscape may look like on January 20, 2025, STA’s mission will remain the same. We are here to represent the securities industry and the interests of you, our members.”

His final piece of advice:

“Meteorologists worldwide are in agreement that the sun will rise on Wednesday, Nov. 6. We may not know who the next president will be on that day, but we will eventually. And life will go on.”

In a similar vein, writer Oliver Burkeman gave some advice on how not to freak about the US election.

Burkerman said: “For years now, since long before I started writing books, I’ve found solace and breathing-space in a question from Eckhart Tolle: “Do you have a problem now?” “Narrow your life down to this moment,” Tolle writes. “Your life situation may be full of problems – most life situations are – but find out if you have any problem at this moment. Not tomorrow or in ten minutes, but now.”

This was backed up by the Daily Stoic website which quoted Marcus Aurelius’ Meditations:

“You must build up your life action by action, and be content if each one achieves its goal as far as possible—and no one can keep you from this.”

The Daily Stoic added: “Being virtuous, like voting, is within our power. Whether it visibly changes the world is not. But we act because it is our duty, and that alone is reason enough. The same applies to voting—in this election, in the next election, in every election. Make your small contribution to the common good, because even if it doesn’t reshape society, it shapes you.”

The Investment Association, the trade body for UK fund managers, is aiming to widen the discussions following the release of the the final report from the Technology Working Group on the industry’s use of artificial intelligence.

On 10 October the UK government published the final report from the Technology Working Group, consisting of policymakers, regulators and market participants, which was set up to identify how the UK investment management industry could harness the potential of innovative new technologies.

Michelle Scrimgeour, chief executive of Legal & General Investment Management and chair of the Technology Working Group, said in a statement that the implementation of analytical AI has been foundational in algorithmic trading and anti-money laundering monitoring.

Michelle Scrimgeour, LGIM

“However, the use of AI is evolving at great pace and the advent of generative AI is a capability that marks a real paradigm shift for our industry,” she added. “When paired with the promise shown with tokenization, the new technological innovations outlined in this report have the potential to redefine how we think about asset management over the next decade.”

John Allan, head of innovation and operations at IA, told Markets Media that the tokenization blueprint was important because it put the UK on a firm footing to start the conversation and as a result, the FCA joined Project Guardian to help learn lessons from Singapore.

“We hope this report on AI will ensure that the UK is able to position itself as an innovative jurisdiction,” said Allan.

He continued that there is now an opportunity, as the trade body had with the previous report on tokenization, to widen the group of members who are involved in discussions beyond the taskforce.

“I think the report was a sober assessment of where we have got to,” Allan added. “It is a very practical and realistic vision of where AI could take us in the future as it is potentially transformational.”

AI can have a transformational role in asset management, for example, by providing quick access to almost any data point to provide actionable insights for portfolio managers. However, Allan highlighted there are still some downsides in terms of Gen AI’s propensity to hallucinate, and giving probabilistic answers when the asset management sector needs very accurate, deterministic outputs. In addition, the sector is highly regulated and regulators’ have objectives in terms of consumer protection and avoiding consumer harm.

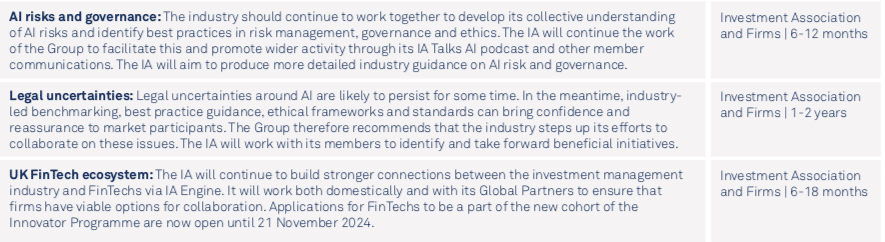

“Potential risks and the governance framework have a lot of interest from members because they are very practical in nature, and we have set some fairly ambitious targets in terms of timeframes,” added Allan.

The Investment Association is owner of recommendations from the report around AI risks and governance; legal uncertainties and the UK fintech ecosystem.

Source: Technology Working Group

Key recommendations from the report include stabilizing regulatory clarity and consistency to enable developers and users of AI to plan and invest with confidence; building a UK fintech ecosystem with strong international connections; joint public and private sector action on AI-enabled fraud; managing systemic risk through collective understanding and identifying best practice in risk management.

Combining blockchain and AI

Allan continued that the combination of blockchain and AI is one of the really interesting discussions.

“It’s certainly not something that is happening today or in the very near future but it is part of the really exciting piece that we could see over a longer timeframe,” he added.

The Investment Association believes that personalization and the power of AI will change the nature of the fund, and has called this new world Investment Fund 3.0 (IF3.0). It consists of a single digital record on a shared blockchain, rather than multiple agents along the value chain running separated record-keeping systems and processes.

Allan gave the example of AI being used to perform tasks that are otherwise performed by humans while DLT provides trust in a trustless environment and said that pairing the two together can be a significant and powerful tool for providing better, more efficient and effective services for consumers.

For example, smart contracts could rely on external data sources that have been assisted by AI.

John Allan, IA

“That feeds into our wider agenda about modernising the infrastructure for investment funds and to providing better services for consumers who are used to operating in a digital environment,” he said. “We would advocate looking at the two in tandem as they progress over the next few years, rather than seeing them as silos that never overlap.”

There are ongoing discussions about how to get explainability on AI, and how that would fit in with the FCA’s senior manager regime, which identifies individuals in firms who are accountable for certain functions, according to Allan. He said the IA has always advocated that firms should not need a designated officer for artificial intelligence, because it is just a technology.

“For example, if AI is being used in the investment process, then the investment officer is responsible,” he added.

The World Federation of Exchanges, has also published a paper on the opportunities and challenges surrounding AI and suggested three 3 foundational principles – principles-based regulation; a risk-based framework and alignment of regulatory standards.

Richard Metcalfe, head of regulatory affairs at the WFE, said in a statement that a failure to strike the right balance in the regulation puts more than growth at risk.

“More advanced machine learning models and generative AI has opened new avenues for enhancing operational efficiency, improving market surveillance, and managing risk,” added Metcalfe. “Policymakers must take care that regulatory changes don’t leave investors more exposed to risk, with overly broad regulation stifling the use of AI in safeguarding markets.”

A Lack of Automation is Draining Asset Managers’ Competitive Edge

By Thomas McHugh, CEO and Co-founder, FINBOURNE Technology

The traditional asset management industry is standing on a precipice, facing immense pressure from all sides. Small and medium-sized investment houses, juggling both equity and fixed-income portfolios, are especially feeling the heat. As retail investors continue to flock to passive investment giants, and institutional investors demand greater customisation at ever-lower fees, many traditional players find themselves struggling to keep up. It’s a battle for survival, and the truth is, this crisis has been looming for years. The cost squeeze that asset managers are now experiencing has reached breaking point.

At the heart of the problem lies a plethora of inefficient processes that have, until now, been tolerated. Research by Coalition Greenwich reveals that outdated systems for managing and sharing data — including manual processing — are costing asset managers millions of dollars each year. One example is the daily grind of trade reconciliation. Each trading day, custodians send data packages to asset managers, outlining the value of assets held on behalf of their clients. These figures need to be reconciled with the fund manager’s own internal records, which include any intra-day trades taking place through brokers. If discrepancies arise, such as trades that haven’t been processed or mismatched valuations, a small army of people is needed to track down the issues and resolve them. It’s a tedious, time-consuming, and frankly immensely costly affair that the industry can no longer afford to absorb.

This archaic approach is just one example of where traditional asset managers can haemorrhage resources. As with many of the operational challenges faced by asset managers, the solution lies in creating a reliable, accurate, and timely source of truth for data that can effectively underpin a fully automated process. Rather than wasting valuable time sifting through data to find exceptions and errors, asset managers can fully automate workflows. This provides real-time trade monitoring, comprehensive audit trails, and configurable alerts which maintain trade integrity. The copious time saved from this automation can then be redirected towards higher-value activities. From conducting deeper market analysis and making more informed decisions to optimise portfolio performance, to spending quality time with clients to understand their needs — think of all that could be done with the additional headspace.

Asset managers have no choice but to adapt. While automating processes is an essential step, it’s about more than just replacing manual tasks with technology. The future lies in fostering a culture of continuous improvement, built on an operating system that connects the past with the future. Such a system should allow firms to be data-driven, using automation, machine learning, and AI to enhance decision-making. Building this foundational infrastructure and mindset is not just a cost-saving measure — it’s the key to remaining competitive in today’s passive-dominant market. Without it, asset managers risk becoming relics of the past, unable to keep pace with an industry that demands adaptability and forward-thinking solutions.