FLASH FRIDAY is a weekly content series looking at the past, present and future of capital markets trading and technology. FLASH FRIDAY is sponsored by Instinet.

The evolution to electronic trading has been a long-term, secular trend in securities markets, dating all the way back to 1969 when Jerome Pustilnik and Herbert Behrens founded Institutional Networks Corp, now Instinet, to enable computerized trading between financial institutions.

Fast forward to 2020; the emergence, establishment and ascendance of electronic trading are old hat, but the COVID-19 backdrop of most traders working remotely has given fresh momentum for electronic trading to capture even more share, especially in non-equity markets that are historically less electronic.

In an August report, J.P. Morgan Chase noted in a report that the global pandemic has resulted in a “dramatic” shift in trading in US Treasuries. According to a Financial Times article: “Figures from the Wall Street bank, one of the biggest Treasury dealers, suggest that a gradual drift towards electronification of the market for US government bonds was accelerated by the impact of the pandemic as many of the bank’s clients — who found themselves suddenly working from home in a volatile market meltdown — preferred to transact based on prices quoted on a screen rather than picking up the phone to negotiate with a human trader.”

Electronic trading in Treasuries increased from about 50% one and two years ago to 70% in April 2020 and 77% in June, according to JP Morgan.

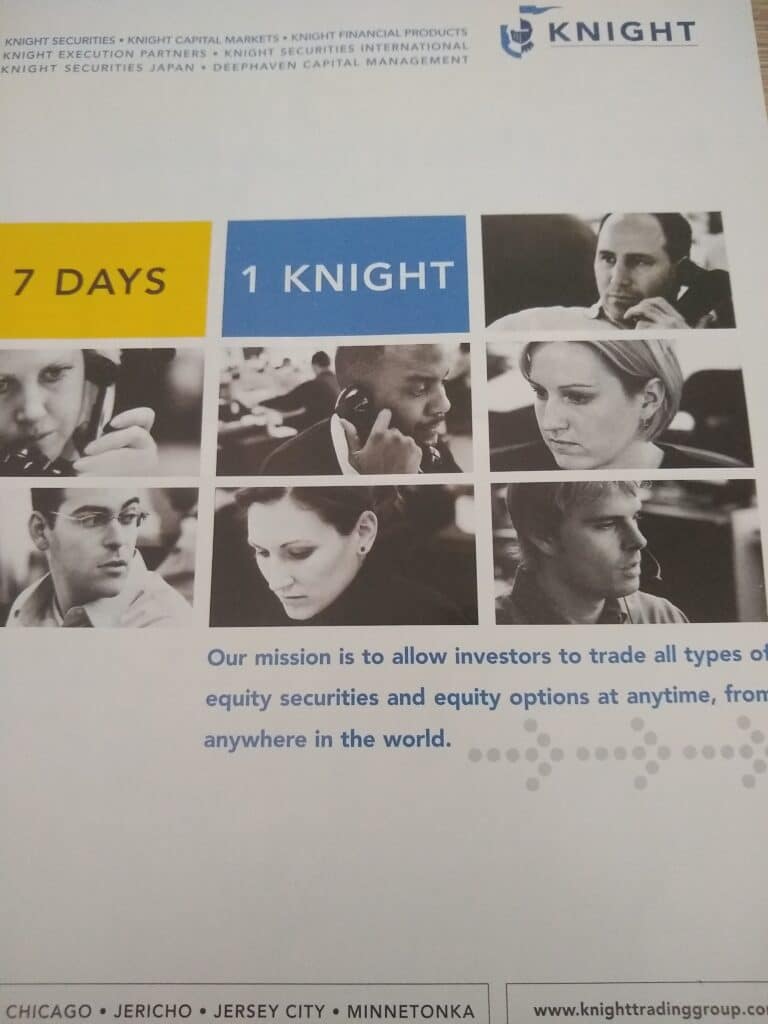

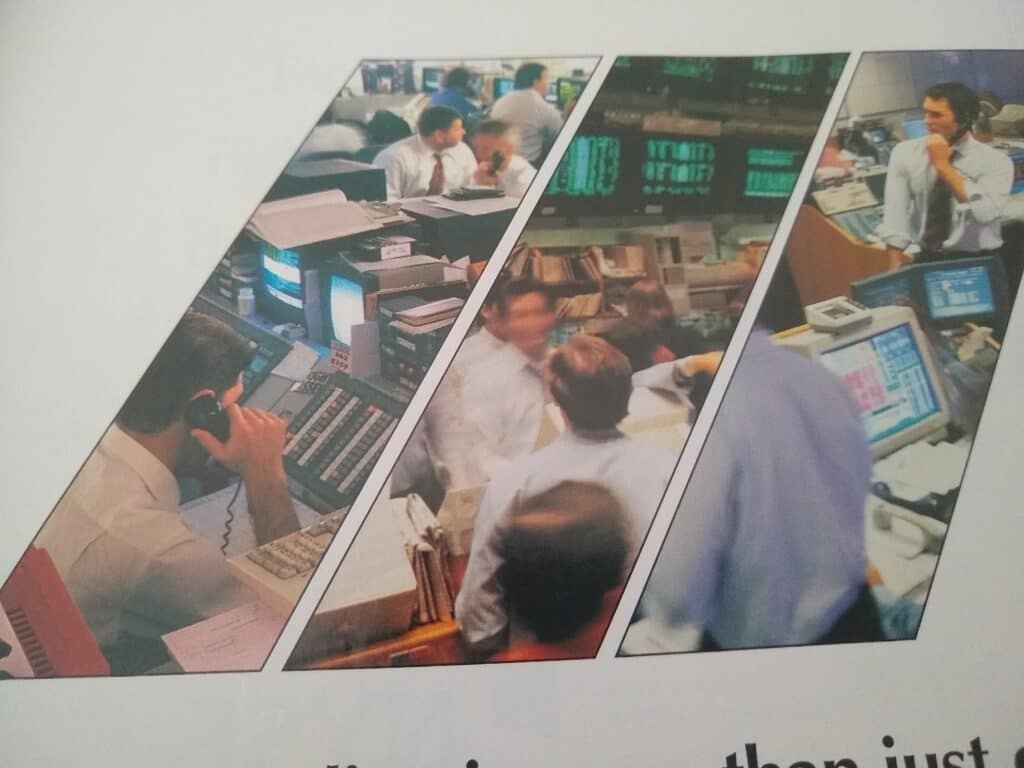

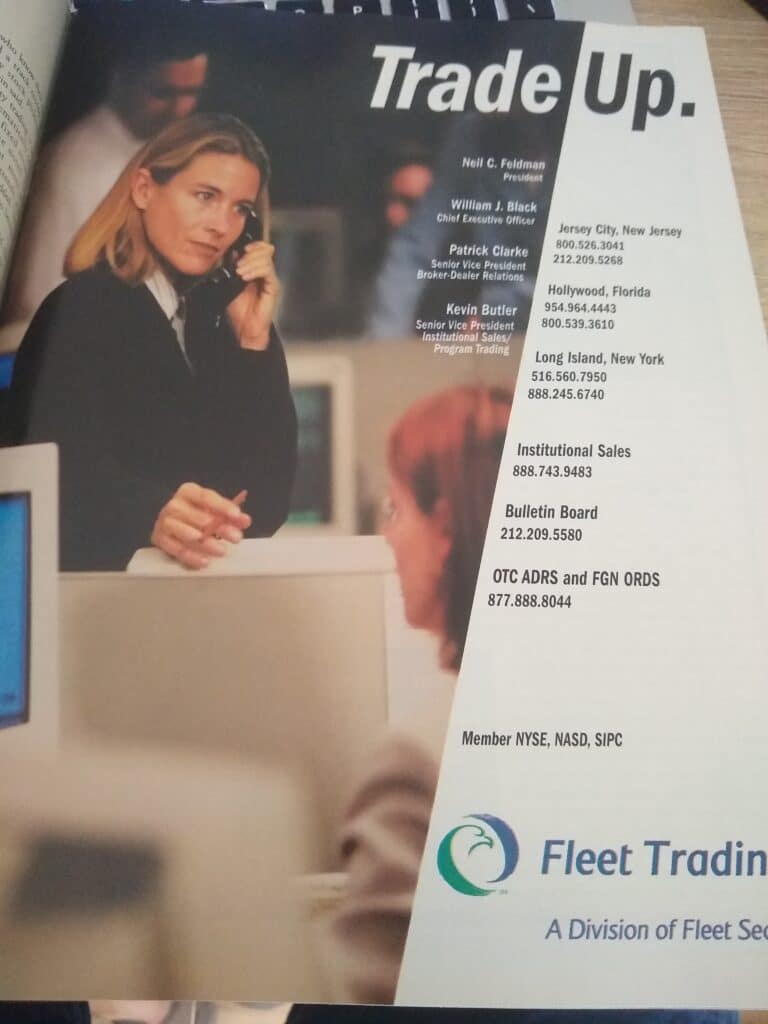

Traders Magazine is fully digital, but if there was still a print edition, it’s safe to say that the advertisements would reflect the times. In 2001, a scan of trading firms’ advertisements showed that the old-fashioned telephone was ubiquitous — possibly the signature piece of trading-floor hardware.

Phones aren’t on the trading-floor scrap heap with ticker-tape machines and quotrons — yet. But they’re used much less frequently, and apparently their utility has taken another leg down in 2020.